Chen Peng, Vivian Andrew, Ye Cheng

Department of Finance and Institute of Finance, School of Economics, Jinan University, Guangzhou, 510632 China.

School of Business and Economics, Loughborough University, Leicestershire, LE11 3TU UK.

Ann Oper Res. 2022;313(1):559-601. doi: 10.1007/s10479-021-04406-4. Epub 2021 Dec 30.

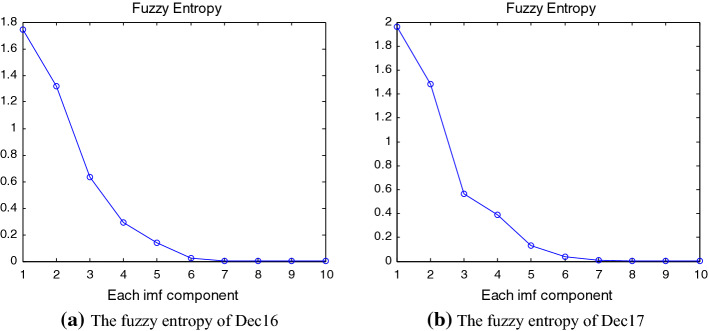

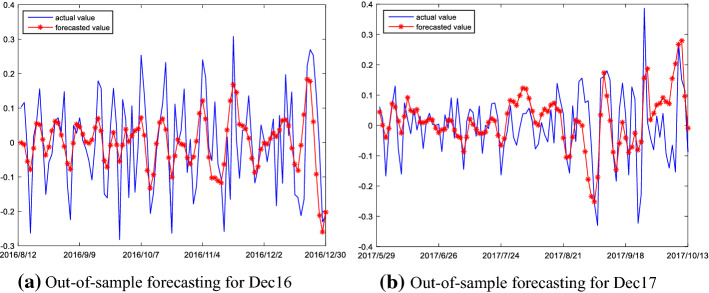

In this paper, we propose a novel hybrid model that extends prior work involving ensemble empirical mode decomposition (EEMD) by using fuzzy entropy and extreme learning machine (ELM) methods. We demonstrate this 3-stage model by applying it to forecast carbon futures prices which are characterized by chaos and complexity. First, we employ the EEMD method to decompose carbon futures prices into a couple of intrinsic mode functions (IMFs) and one residue. Second, the fuzzy entropy and K-means clustering methods are used to reconstruct the IMFs and the residue to obtain three reconstructed components, specifically a high frequency series, a low frequency series, and a trend series. Third, the ARMA model is implemented for the stationary high and low frequency series, while the extreme learning machine (ELM) model is utilized for the non-stationary trend series. Finally, all the component forecasts are aggregated to form final forecasts of the carbon price for each model. The empirical results show that the proposed reconstruction algorithm can bring more than 40% improvement in prediction accuracy compared to the traditional fine-to-coarse reconstruction algorithm under the same forecasting framework. The hybrid forecasting model proposed in this paper also well captures the direction of the price changes, with strong and robust forecasting ability, which is significantly better than the single forecasting models and the other hybrid forecasting models.

在本文中,我们提出了一种新颖的混合模型,该模型通过使用模糊熵和极限学习机(ELM)方法扩展了先前涉及总体经验模态分解(EEMD)的工作。我们通过将此三阶段模型应用于预测具有混沌和复杂性特征的碳期货价格来进行演示。首先,我们采用EEMD方法将碳期货价格分解为若干个本征模态函数(IMF)和一个余项。其次,使用模糊熵和K均值聚类方法对IMF和余项进行重构,以获得三个重构分量,具体为高频序列、低频序列和趋势序列。第三,对平稳的高频和低频序列实施自回归滑动平均(ARMA)模型,而对非平稳的趋势序列使用极限学习机(ELM)模型。最后,将所有分量预测进行汇总,以形成每个模型的碳价格最终预测。实证结果表明,与相同预测框架下的传统由细到粗重构算法相比,所提出的重构算法在预测精度上可带来超过40%的提升。本文提出的混合预测模型也很好地捕捉了价格变化方向,具有强大且稳健的预测能力,显著优于单一预测模型和其他混合预测模型。