Ullah Mirzat, Sohag Kazi, Haddad Hossam

Graduate School of Economics and Management, Ural Federal University, Yekaterinburg, 620002, Russia.

School of Management Sciences, Ghulam Ishaq Khan (GIK) Institute of Engineering Sciences and Technology, Topi, Swabi, Pakistan.

Heliyon. 2024 May 1;10(9):e30558. doi: 10.1016/j.heliyon.2024.e30558. eCollection 2024 May 15.

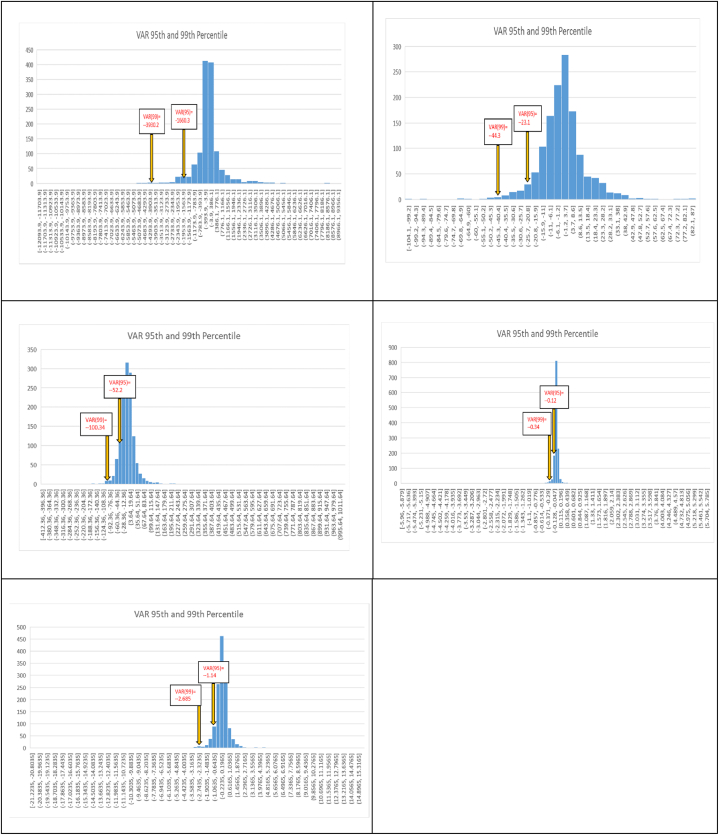

This empirical research study aims to investigate the asymmetric spillovers among crypto and key financial assets such as gold, equity, bonds, and the dollar-to-ruble exchange rate volatility, focusing on new developments during the Russia-Ukraine conflict in 2022. Utilizing time- and frequency-domain methodologies, this study conducts an in-depth analysis employing daily frequency data from January 01, 2018, to May 30, 2023. The study employs value at risk and conditional value at risk estimations to assess potential losses in the portfolio during the crisis. The findings reveal that Bitcoin exhibits hedging ability, enabling investors to diversify risk among the underlying financial assets. The study observes a significant increase in Bitcoin investments during the crisis, leading to heightened volatility and uncertainty. Negative news has a stronger impact compared to positive news, underscoring the importance of prudent asset allocation for risk mitigation. The implications of our findings are particularly significant for financial policymakers and trade partners of Russia. The study urges them to differentiate their short- and long-term strategies and procurement contracts. In the long run, policymakers should be cognizant of the influence of the riskiness of crypto assets during economic crises, guiding the formulation of prudent policies and investment decision-making initiatives.

这项实证研究旨在调查加密货币与黄金、股票、债券等关键金融资产以及美元兑卢布汇率波动之间的不对称溢出效应,重点关注2022年俄乌冲突期间的新情况。本研究利用时域和频域方法,采用2018年1月1日至2023年5月30日的日频率数据进行深入分析。该研究采用风险价值和条件风险价值估计来评估危机期间投资组合中的潜在损失。研究结果表明,比特币具有套期保值能力,使投资者能够在基础金融资产之间分散风险。该研究观察到危机期间比特币投资显著增加,导致波动性和不确定性加剧。负面消息比正面消息的影响更大,这凸显了谨慎资产配置以降低风险的重要性。我们研究结果的影响对俄罗斯的金融政策制定者和贸易伙伴尤为重要。该研究敦促他们区分短期和长期战略以及采购合同。从长远来看,政策制定者应认识到加密资产风险在经济危机期间的影响,并指导制定谨慎的政策和投资决策举措。