Kakani Pragya, Navangul Swayami, Lee Luo Christie, Tormohlen Kayla N, Kanter Genevieve P, Landrum Mary Beth, Keating Nancy L, Bond Amelia M

Department of Population Health Sciences, Weill Cornell Medical College, New York, New York.

Department of Health Policy and Management, Sol Price School of Public Policy, University of Southern California, Los Angeles.

JAMA Health Forum. 2025 Jan 3;6(1):e244874. doi: 10.1001/jamahealthforum.2024.4874.

The prevalence of pharmacies owned by integrated insurers and pharmacy benefit managers (PBMs), or insurer-PBMs, is of growing regulatory concern. However, little is known about the role of these pharmacies in Medicare, in which pharmacy network protections may influence market dynamics.

To evaluate the prevalence of insurer-PBM-owned pharmacies and the extent to which insurer-PBMs steer patients to pharmacies they own in Medicare.

DESIGN, SETTING, AND PARTICIPANTS: This cross-sectional study used Medicare Part D claims data on prescription fills for a 20% random sample of US beneficiaries enrolled from January 1 through December 31, 2021. Data were analyzed from March to November 2024.

Prescription fills.

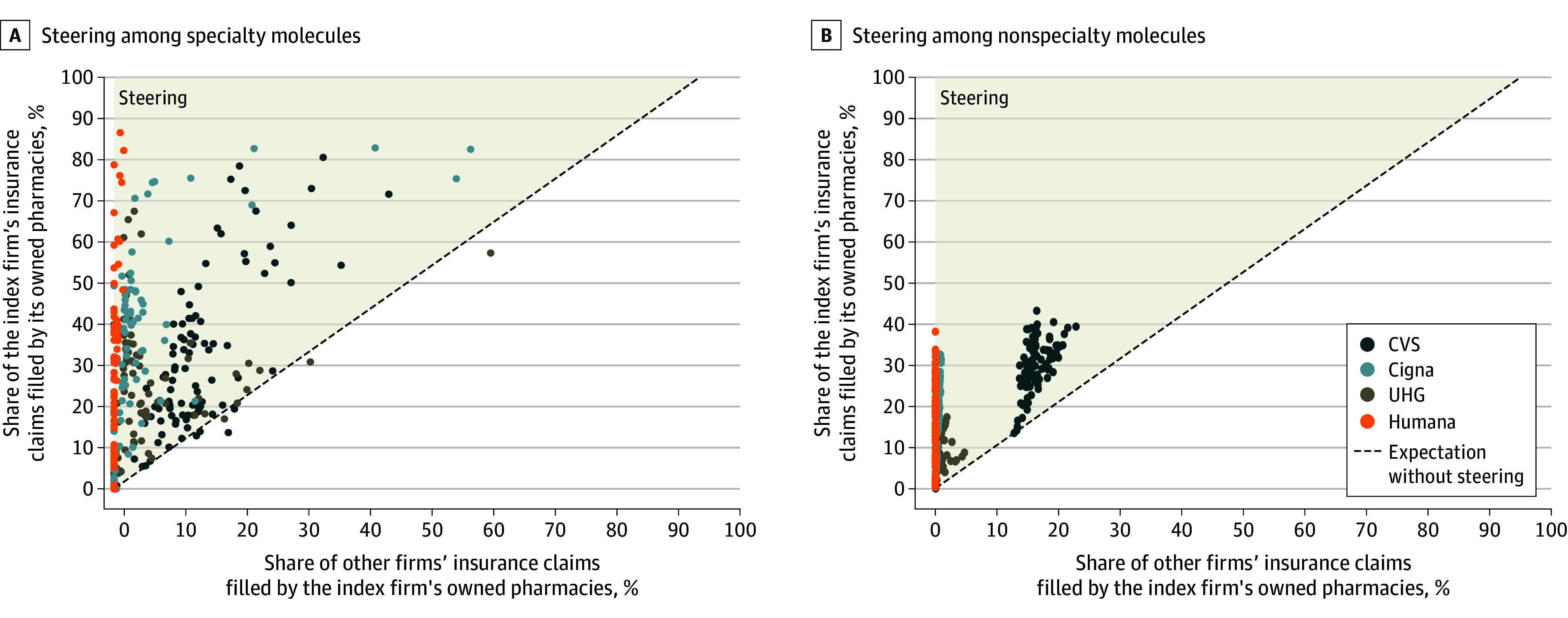

The main outcome was the share of spending filled by insurer-PBM-owned pharmacies overall, by pharmacy type (specialty and nonspecialty), and by drug class. For the top 100 specialty and nonspecialty molecules by claim volume, 2 quantities were identified for 4 major insurer-PBMs (Cigna, CVS, Humana, and UnitedHealth Group): share of the index firm's insurer claims filled by its owned pharmacies and share of other firms' insurer claims filled by the index firm's owned pharmacies. Differences between these quantities were assessed to evaluate the degree to which insurer-PBMs steered patients to their own pharmacies.

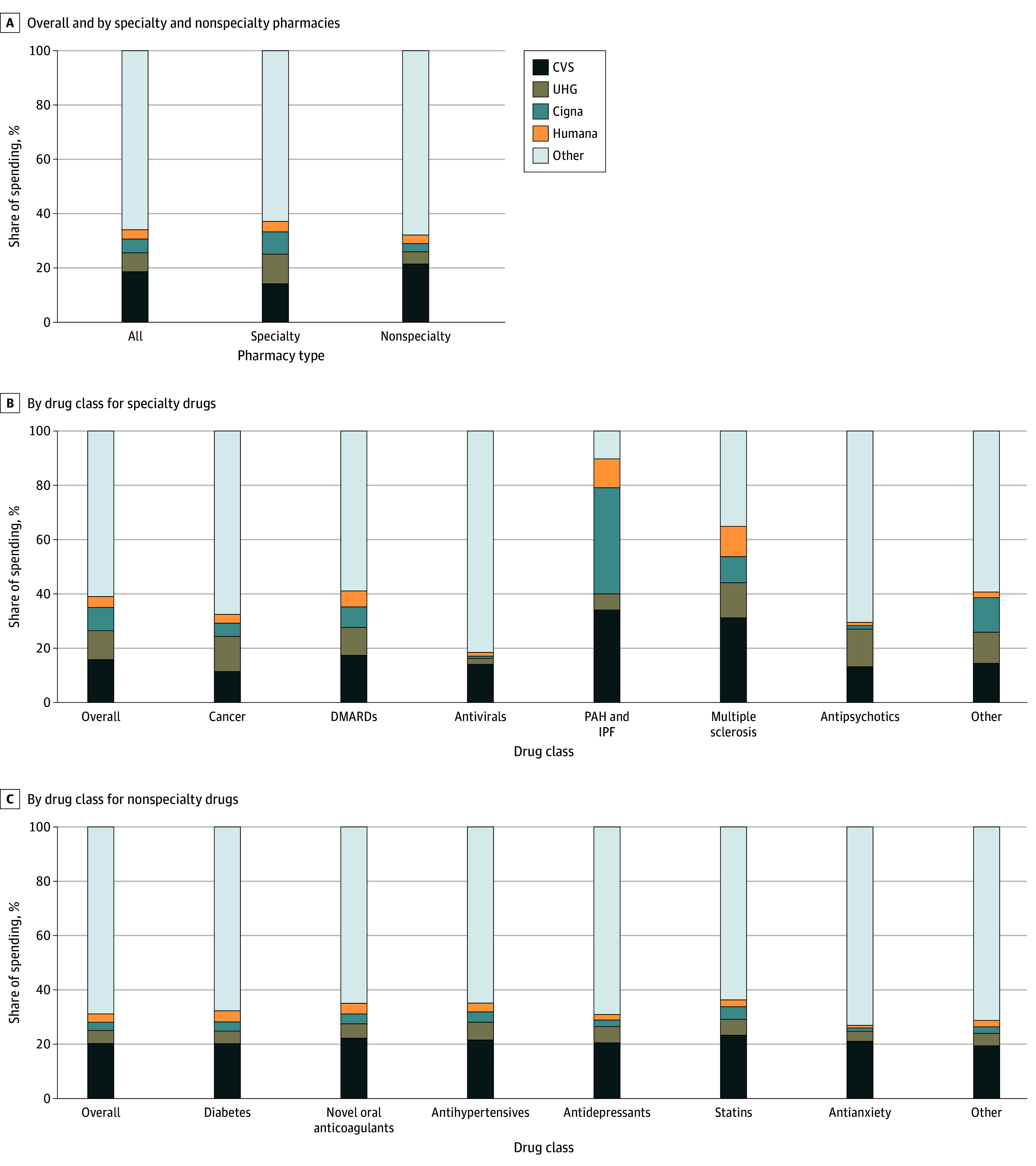

Among 10 455 726 patients (54.8% women; mean [SD] age, 71.8 [10.7] years), 34.1% of all pharmacy and 37.1% of specialty pharmacy spending occurred through Cigna, CVS, Humana, or UnitedHealth Group pharmacies. Among specialty molecules, market shares varied by drug class (antivirals: 18.5%; antipsychotics: 29.5%; cancer: 32.5%; disease-modifying antirheumatic drugs: 41.1%; multiple sclerosis: 64.8%; pulmonary arterial hypertension and idiopathic pulmonary fibrosis: 89.7%). Across molecule-firm combinations, a 19.8 (95% CI, 18.0-21.6)-percentage point and 13.9 (95% CI, 13.1-14.7)-percentage point greater share of claims were filled at insurer-PBM-owned pharmacies than would be expected without steering for specialty and nonspecialty categories, respectively.

This cross-sectional study found that insurer-PBM firms represented an important portion of the Medicare Part D market, especially for certain drug classes, and that insurer-PBM firms steered patients to their own pharmacies, despite certain pharmacy network protections in Medicare. These findings underscore the need to understand the impacts of insurer-PBM and pharmacy integration on medication access and costs for Medicare patients.

综合保险公司和药品福利管理机构(PBM)所拥有的药房,即保险公司 - PBM药房的流行情况,日益受到监管关注。然而,对于这些药房在医疗保险中的作用,人们知之甚少,而医疗保险中的药房网络保护可能会影响市场动态。

评估保险公司 - PBM所拥有药房的流行情况,以及保险公司 - PBM在医疗保险中引导患者前往其自有药房的程度。

设计、设置和参与者:这项横断面研究使用了2021年1月1日至12月31日期间登记的20%美国受益人的医疗保险D部分处方配药索赔数据。数据于2024年3月至11月进行分析。

处方配药。

主要结局是保险公司 - PBM所拥有药房的总体支出份额,按药房类型(专科和非专科)以及药物类别划分。对于按索赔量排名前100的专科和非专科分子,确定了4家主要保险公司 - PBM(信诺、CVS、哈门那和联合健康集团)的2个数量指标:指数公司自有药房所填充的指数公司保险索赔份额,以及指数公司自有药房所填充的其他公司保险索赔份额。评估这些数量指标之间的差异,以评估保险公司 - PBM将患者引导至其自有药房的程度。

在10455726名患者中(54.8%为女性;平均[标准差]年龄为71.8[10.7]岁),所有药房支出的34.1%和专科药房支出的37.1%是通过信诺、CVS、哈门那或联合健康集团的药房发生的。在专科分子中,市场份额因药物类别而异(抗病毒药物:18.5%;抗精神病药物:29.5%;癌症药物:32.5%;改善病情的抗风湿药物:41.1%;多发性硬化症药物:64.8%;肺动脉高压和特发性肺纤维化药物:89.7%)。在分子 - 公司组合中,与没有引导的情况下相比,专科和非专科类别中,保险公司 - PBM所拥有药房填充的索赔份额分别高出19.8(95%置信区间,18.0 - 21.6)个百分点和13.9(95%置信区间,13.1 - 14.7)个百分点。

这项横断面研究发现,保险公司 - PBM公司在医疗保险D部分市场中占重要部分,尤其是对于某些药物类别,并且尽管医疗保险中有某些药房网络保护措施,保险公司 - PBM公司仍将患者引导至其自有药房。这些发现强调了了解保险公司 - PBM与药房整合对医疗保险患者用药可及性和成本影响的必要性。