Bacanin Nebojsa, Tuba Milan

Faculty of Computer Science, Megatrend University Belgrade, 11070 Belgrade, Serbia.

ScientificWorldJournal. 2014;2014:721521. doi: 10.1155/2014/721521. Epub 2014 May 29.

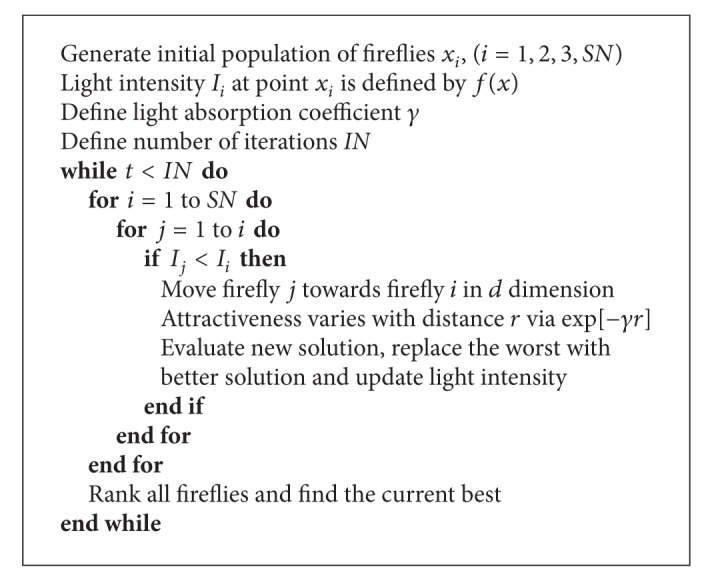

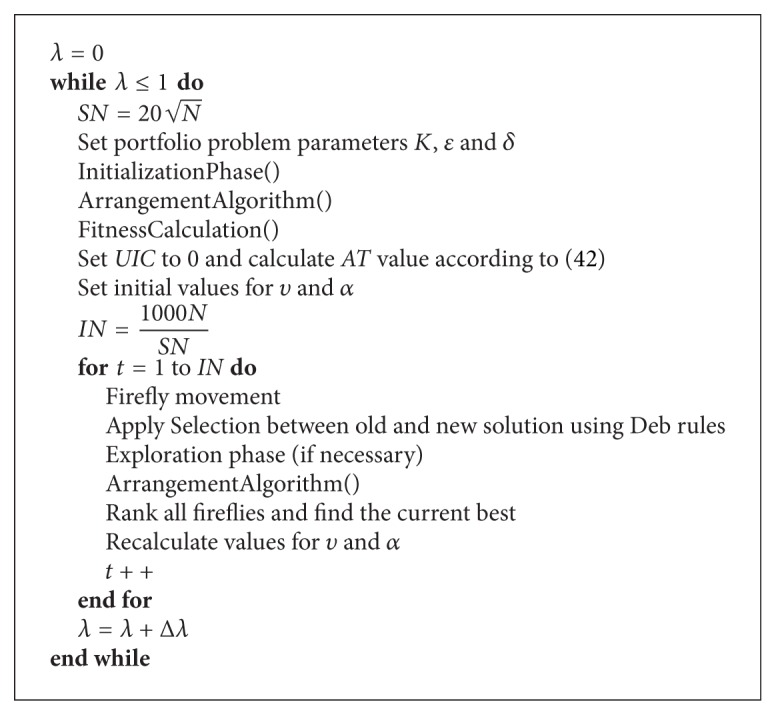

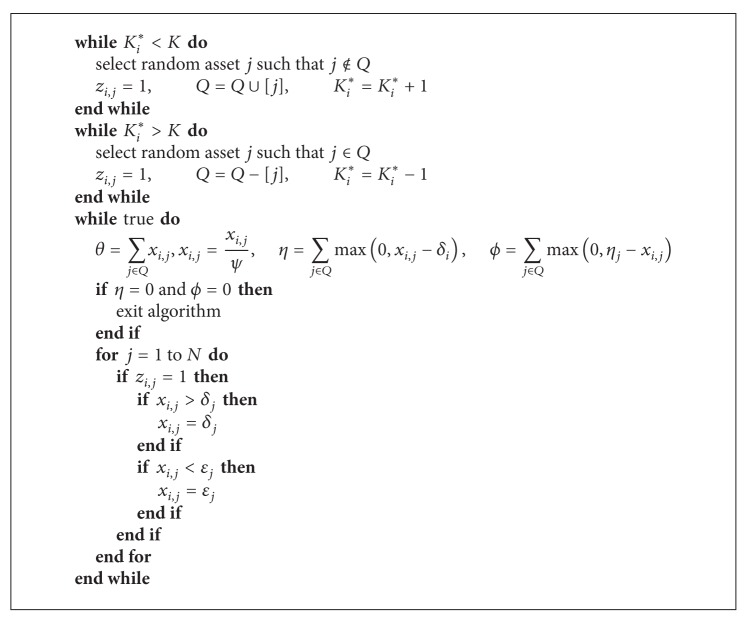

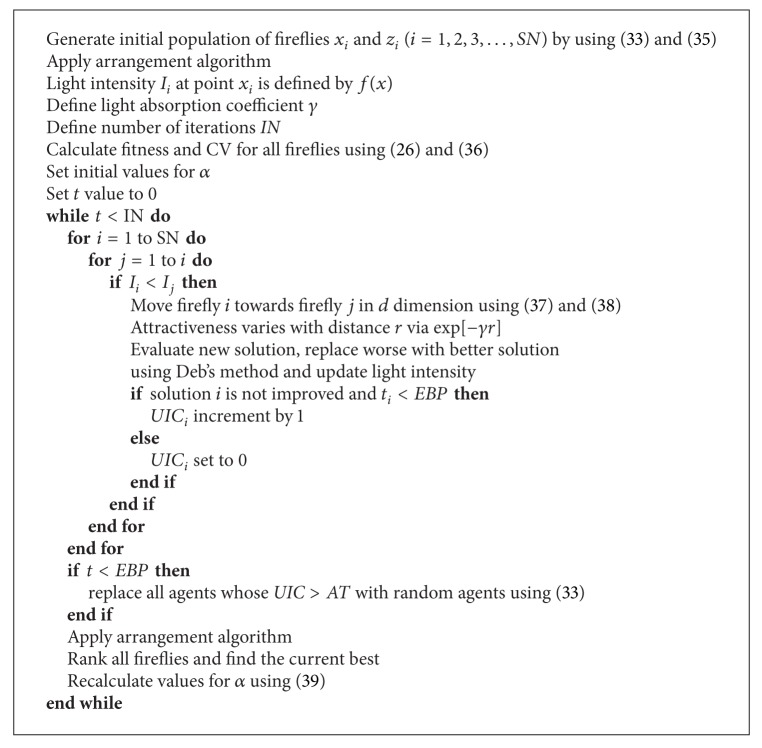

Portfolio optimization (selection) problem is an important and hard optimization problem that, with the addition of necessary realistic constraints, becomes computationally intractable. Nature-inspired metaheuristics are appropriate for solving such problems; however, literature review shows that there are very few applications of nature-inspired metaheuristics to portfolio optimization problem. This is especially true for swarm intelligence algorithms which represent the newer branch of nature-inspired algorithms. No application of any swarm intelligence metaheuristics to cardinality constrained mean-variance (CCMV) portfolio problem with entropy constraint was found in the literature. This paper introduces modified firefly algorithm (FA) for the CCMV portfolio model with entropy constraint. Firefly algorithm is one of the latest, very successful swarm intelligence algorithm; however, it exhibits some deficiencies when applied to constrained problems. To overcome lack of exploration power during early iterations, we modified the algorithm and tested it on standard portfolio benchmark data sets used in the literature. Our proposed modified firefly algorithm proved to be better than other state-of-the-art algorithms, while introduction of entropy diversity constraint further improved results.

投资组合优化(选择)问题是一个重要且困难的优化问题,在添加必要的现实约束后,该问题在计算上变得难以处理。受自然启发的元启发式算法适用于解决此类问题;然而,文献综述表明,受自然启发的元启发式算法在投资组合优化问题中的应用非常少。对于代表受自然启发算法新分支的群体智能算法来说尤其如此。在文献中未发现任何群体智能元启发式算法应用于具有熵约束的基数约束均值 - 方差(CCMV)投资组合问题。本文针对具有熵约束的CCMV投资组合模型引入了改进的萤火虫算法(FA)。萤火虫算法是最新且非常成功的群体智能算法之一;然而,当应用于约束问题时,它存在一些不足之处。为了克服早期迭代中缺乏探索能力的问题,我们对该算法进行了改进,并在文献中使用的标准投资组合基准数据集上进行了测试。我们提出的改进萤火虫算法被证明比其他现有算法更好,而引入熵多样性约束进一步改善了结果。