Facultad de Economía y Negocios, Universidad Finis Terrae, Santiago, Chile.

Escuela de Negocios, Universidad Adolfo Ibáñez, Santiago, Chile.

PLoS One. 2021 May 20;16(5):e0250846. doi: 10.1371/journal.pone.0250846. eCollection 2021.

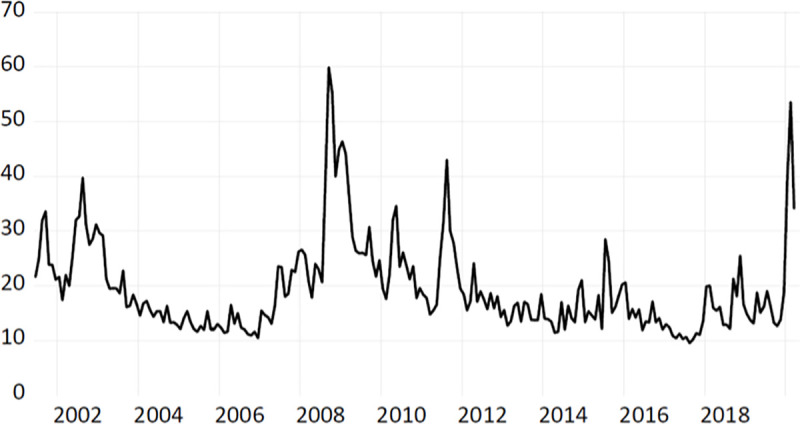

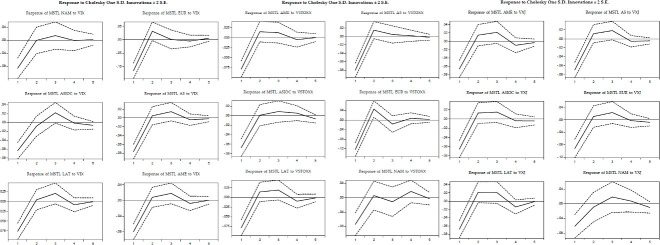

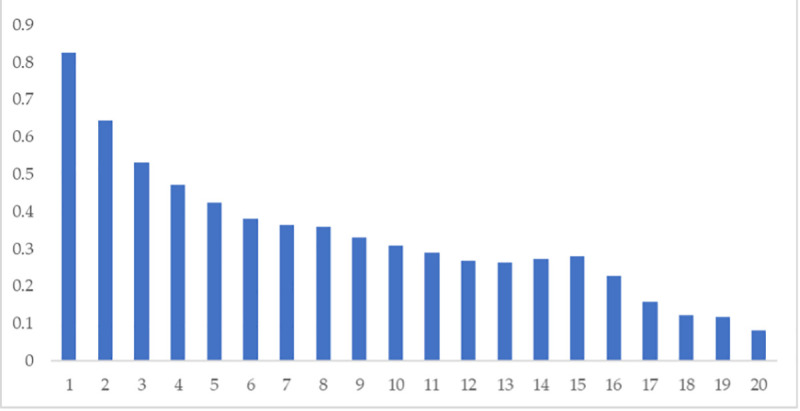

We explore the use of implied volatility indices as a tool for estimate changes in the synchronization of stock markets. Specifically, we assess the implied stock market's volatility indices' predictive power on synchronizing global equity indices returns. We built the correlation network of 26 stock indices and implemented in-sample and out-of-sample tests to evaluate the predictive power of VIX, VSTOXX, and VXJ implied volatility indices. To measure markets' synchronization, we use the Minimum Spanning Tree length and the length of the Planar Maximally Filtered Graph. Our results indicate a high predictive power of all the volatility indices, both individually and together, though the VIX predominates over the evaluated options. We find that an increase in the markets' volatility expectations, captured by the implied volatility indices, is a good Granger predictor of an increase in the synchronization of returns in the following month. Estimating, monitoring, and predicting returns' synchronization is essential for investment decision-making, especially for diversification strategies and regulating financial systems.

我们探索了隐含波动率指数作为衡量股票市场同步变化的工具的用途。具体来说,我们评估了隐含股票市场波动率指数对全球股票指数回报同步性的预测能力。我们构建了 26 个股票指数的相关网络,并进行了样本内和样本外测试,以评估 VIX、VSTOXX 和 VXJ 隐含波动率指数的预测能力。为了衡量市场同步性,我们使用最小生成树长度和平面最大过滤图长度。我们的结果表明,所有波动率指数都具有较高的预测能力,无论是单独使用还是一起使用,尽管 VIX 都优于评估的选项。我们发现,隐含波动率指数所捕捉的市场波动预期的增加,是下一个月回报同步性增加的一个很好的格兰杰预测指标。估计、监测和预测回报的同步性对于投资决策至关重要,尤其是对于多元化策略和监管金融系统。