Agliardi Elettra, Agliardi Rossella

Department of Economics, University of Bologna, piazza Scaravilli 2, 40126 Bologna, Italy.

Department of Mathematics, University of Bologna, Bologna, Italy.

Environ Resour Econ (Dordr). 2021;80(2):257-278. doi: 10.1007/s10640-021-00585-7. Epub 2021 Aug 2.

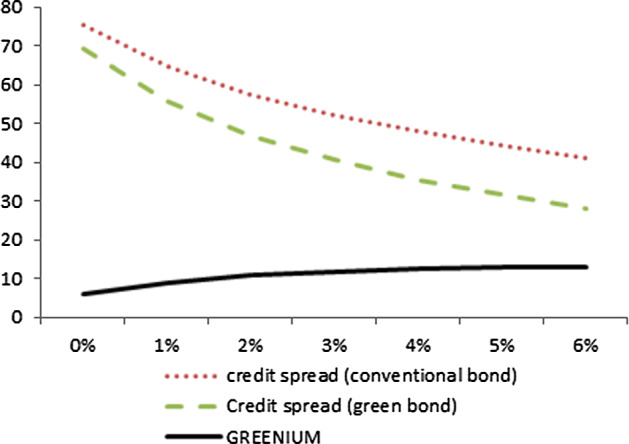

A novel structural model is developed to understand the determinants of green bond prices and the so-called 'greenium', that is, the premium that bondholders are willing to pay to invest in green securities rather than conventional ones. The presence of a greenium makes green bonds relatively cheap vehicles to fund environmentally sustainable projects and thus contributes to the shift to a green economy. Yet, evidence on the greenium is mixed and the determinants of green bond yields are not fully understood. In this model two sources of uncertainty are introduced, that is, of cash flows of the firm and of the effectiveness of the financed green projects. The adoption of two risk factors brings in some mathematical complexity but allows for a better modelling of the multi-facet nature of these financial instruments. Our model is rich enough to generate both a positive and a negative premium, as both have been detected in the empirical literature. Thus, we shed light on possible heterogeneity concerning the existence of a greenium in the green bond universe. Moreover, we show how green bonds affect the issuer's creditworthiness, depending on the correlation of the green project with the core business of the firm and study their impact on investors' portfolio allocation.

为理解绿色债券价格的决定因素以及所谓的“绿色溢价”(即债券持有人愿意为投资绿色证券而非传统证券支付的溢价),开发了一种新颖的结构模型。绿色溢价的存在使绿色债券成为为环境可持续项目融资的相对低成本工具,从而有助于向绿色经济转型。然而,关于绿色溢价的证据喜忧参半,且绿色债券收益率的决定因素尚未完全明晰。在该模型中引入了两个不确定性来源,即公司现金流的不确定性和所融资绿色项目有效性的不确定性。采用两个风险因素带来了一定的数学复杂性,但能更好地对这些金融工具的多面性质进行建模。我们的模型足够丰富,能够产生正溢价和负溢价,因为实证文献中都已发现了这两种情况。因此,我们揭示了绿色债券领域中绿色溢价存在可能的异质性。此外,我们展示了绿色债券如何根据绿色项目与公司核心业务的相关性影响发行人的信用状况,并研究它们对投资者投资组合配置的影响。