Stănescu C-G

Faculty of Law, University of Copenhagen, Njalsgade 76, Office: 6A-3-32, 2300 Copenhagen, Denmark.

J Consum Policy (Dordr). 2021;44(4):531-557. doi: 10.1007/s10603-021-09495-z. Epub 2021 Aug 30.

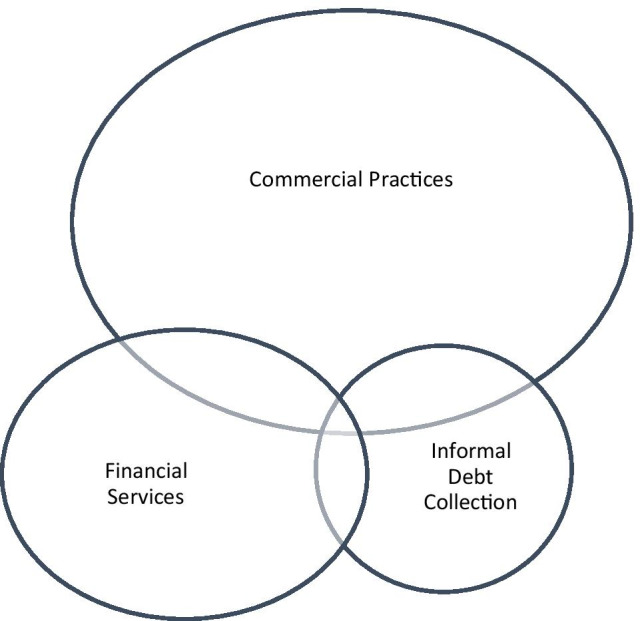

The loss of jobs and the decline in real incomes caused by the 2008 financial crisis and the COVID-19 pandemic have affected consumers' ability to repay their debts. These have led to high ratios of non-performing loans (NPLs), which affect the stability of the financial industry and undermine economic recovery. The result has been a need for faster debt enforcement and a drastic increase in abusive informal debt collection practices (IDCPs). In the EU, the need to regulate and harmonize abusive IDCPs surfaced in 2018 in connection to the Proposal for a Directive on Credit Servicers, Credit Purchasers and the Recovery of Collateral (CSDP). The directive would enable banks to outsource the servicing of NPLs to a specialized debt collector, but it contained no protection rules against abusive IDCPs. In this article, the researcher critically assesses the need for harmonization of the legal framework concerning abusive IDCPs in the EU, mainly from the standpoint of the initial and current text of the CSDP. Where necessary, the researcher will refer to both historical and comparative law perspectives. The researcher focuses on the legal character of informal debt collection, its relation to financial services, and its potential sui generis character. After that, the researcher will address the arguments for and against establishing pan-EU sector-specific legislation dedicated to IDCPs. Next, the researcher discusses the constitutional authority of the EU to regulate abusive IDCPs. Finally, the researcher will examine the interaction of the CSDP with other consumer (financial) protection instruments to identify the best solution for harmonizing abusive IDCPs at the EU level. The researcher will juxtapose several dichotomies: general versus sector-specific, procedural versus substantive, minimum versus maximum harmonization, and hard versus soft regulation. In the conclusion, the researcher shall synthesize the core problems and suggest an approach.

2008年金融危机和新冠疫情导致的就业岗位流失以及实际收入下降,影响了消费者偿还债务的能力。这些情况导致不良贷款率居高不下,影响了金融业的稳定性,破坏了经济复苏。结果是需要加快债务执行,并大幅增加滥用性的非正式债务催收行为。在欧盟,2018年,随着《信贷服务机构、信贷购买者及抵押物回收指令》(CSDP)提案的提出,对滥用性非正式债务催收行为进行监管和协调的必要性浮出水面。该指令将使银行能够将不良贷款的服务外包给专业债务催收机构,但其中没有针对滥用性非正式债务催收行为的保护规则。在本文中,研究者主要从CSDP的初始文本和当前文本的角度,批判性地评估欧盟统一关于滥用性非正式债务催收行为的法律框架的必要性。必要时,研究者将参考历史和比较法的视角。研究者关注非正式债务催收的法律性质、其与金融服务的关系以及其潜在的特殊性质。之后,研究者将阐述支持和反对制定专门针对非正式债务催收行为的泛欧部门特定立法的论点。接下来,研究者讨论欧盟监管滥用性非正式债务催收行为的宪法权限。最后,研究者将研究CSDP与其他消费者(金融)保护工具的相互作用,以确定在欧盟层面统一滥用性非正式债务催收行为的最佳解决方案。研究者将并列几个二分法:一般与部门特定、程序与实体、最低限度与最大限度协调以及硬监管与软监管。在结论部分,研究者将综合核心问题并提出一种方法。