Bermejo Ramón, Figuerola-Ferretti Isabel, Hevia Tomas, Santos Alvaro

Universidad Pontificia Comillas, C/ Alberto Aguilera, 23, 28015, Madrid, Spain.

C/ Castelló, 77-5 planta, 28006, Madrid, Spain.

Heliyon. 2021 Oct 12;7(10):e08168. doi: 10.1016/j.heliyon.2021.e08168. eCollection 2021 Oct.

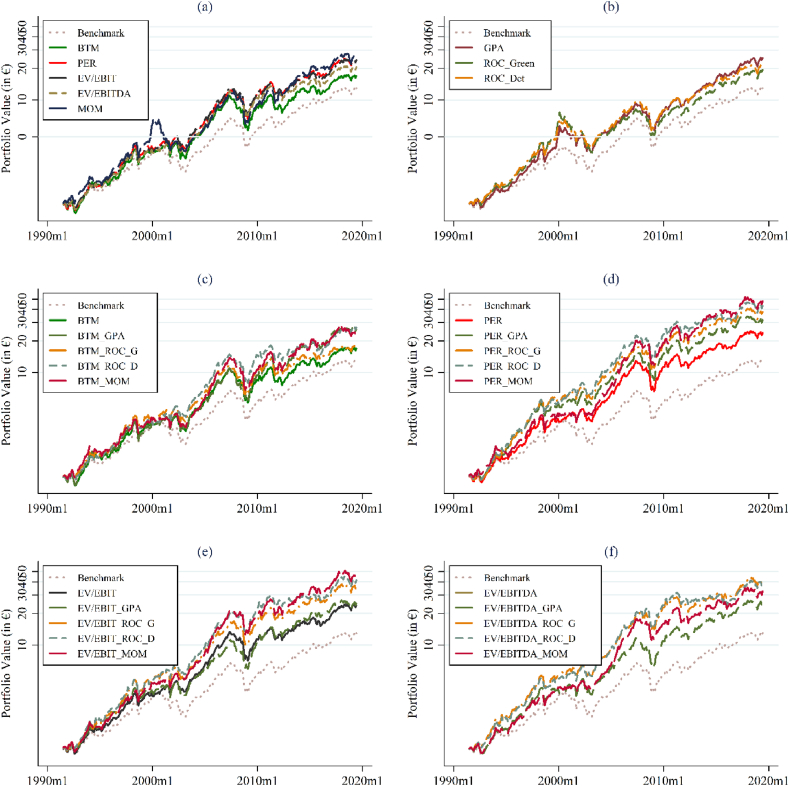

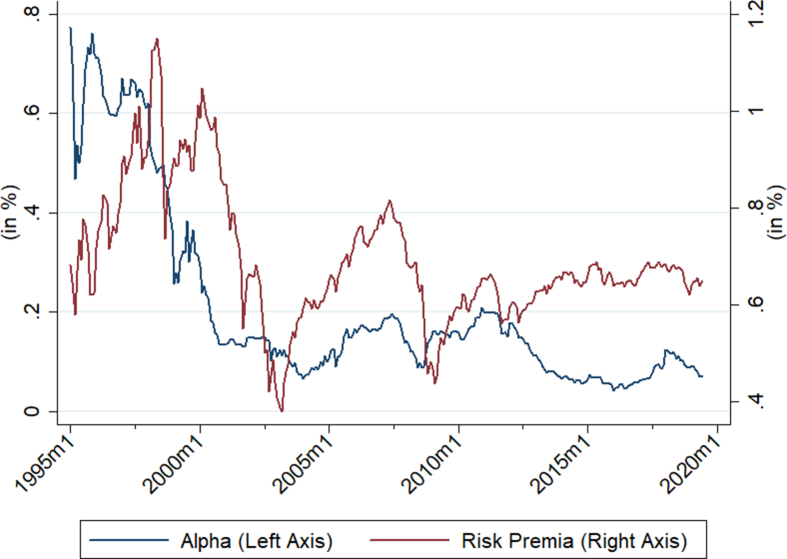

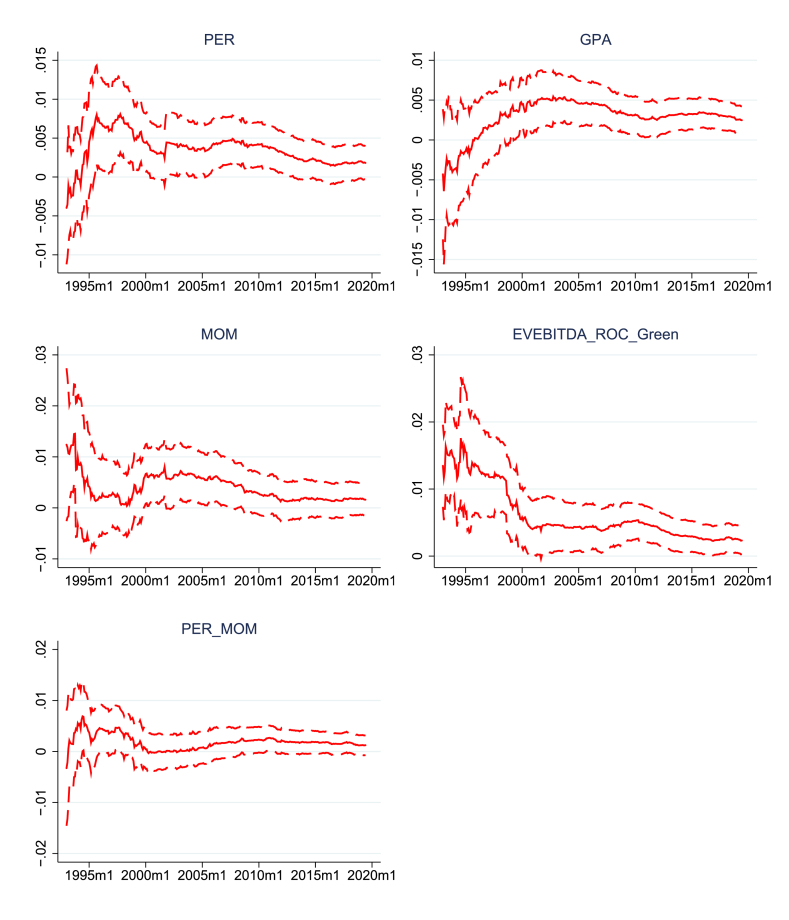

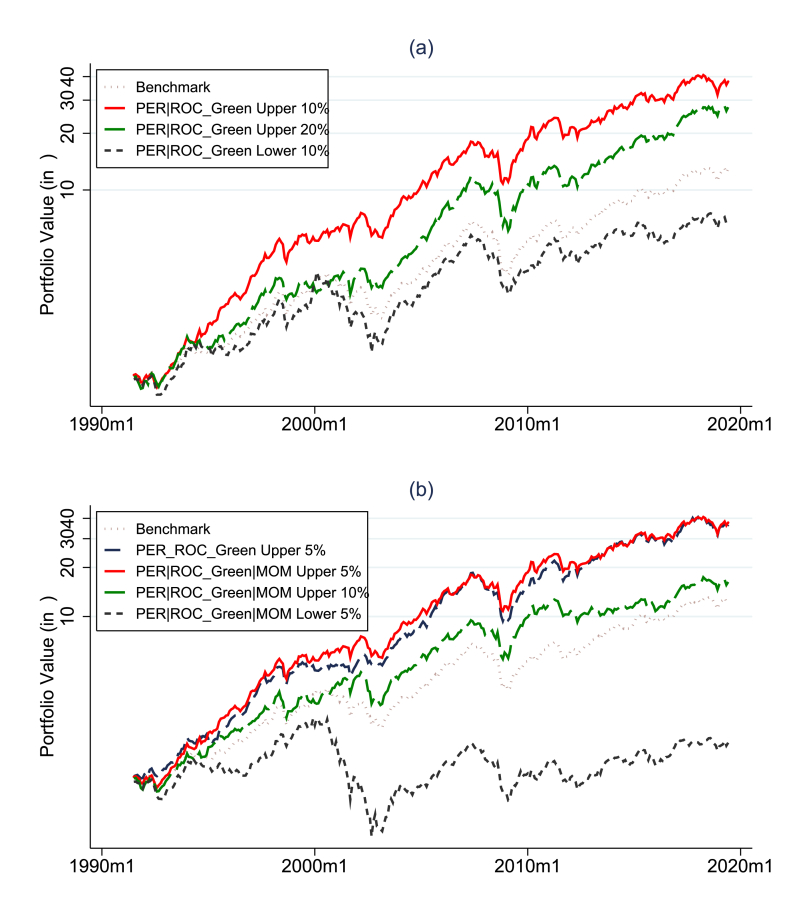

This paper uses European high capitalization corporate data for the 1991-2019 period to demonstrate that a systematic active management portfolio based on the identification of value, profitability, and momentum factors can outperform competing benchmark strategies. Factor investment methodologies received significant attention in the literature in the U.S. market but their application to European corporates is more limited. The authors construct several systematic investment strategies combining different metrics measuring the three factors. Reported results show that a) combined (mixed/conditional) strategies deliver positive alphas and significantly outperform their pure strategy counterparts and b) while there exists a time changing performance of selected metrics the iterative combination of factors delivers the highest performance with average annualized compounded returns of up to about 17%. Three Key Takeaways: 1. This paper documents the existence of alpha-generating factor strategies based on a combination of value, profitability, and momentum metrics. Combined (mixed/conditional) portfolios significantly outperform their pure strategy counterparts. 2. The iterative combination of factors delivers the highest performance with annualized compounded returns of up to 17%. 3. In line with the recent literature, we find decaying returns to factor strategies.

本文使用1991 - 2019年期间欧洲高市值公司数据来证明,基于价值、盈利能力和动量因子识别的系统性主动管理投资组合能够超越竞争基准策略。因子投资方法在美国市场的文献中受到了广泛关注,但其在欧洲公司中的应用较为有限。作者构建了几种结合不同指标来衡量这三个因子的系统性投资策略。报告结果显示:a)组合(混合/条件)策略产生了正的阿尔法收益,显著优于其纯策略对应物;b)虽然所选指标的表现随时间变化,但因子的迭代组合带来了最高的绩效,年化复合平均回报率高达约17%。三个关键要点:1. 本文证明了基于价值、盈利能力和动量指标组合的产生阿尔法收益的因子策略的存在。组合(混合/条件)投资组合显著优于其纯策略对应物。2. 因子的迭代组合带来了最高的绩效,年化复合回报率高达17%。3. 与近期文献一致,我们发现因子策略的收益在衰减。