Živkov Dejan, Manić Slavica, Pavkov Ivan

Novi Sad Business School, University of Novi Sad, Vladimira Perića Valtera 4, 21000 Novi Sad, Serbia.

Faculty of Economics in Belgrade, University of Belgrade, Kamenička 6, 11000 Beograd, Serbia.

Empir Econ. 2022;63(2):1109-1134. doi: 10.1007/s00181-021-02148-7. Epub 2021 Oct 23.

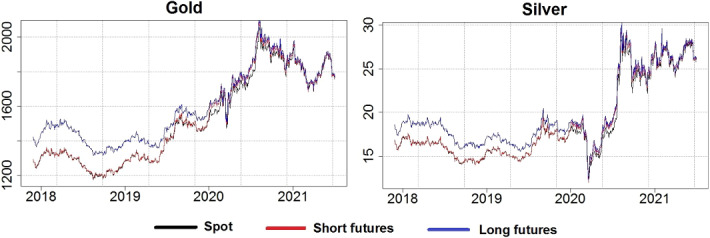

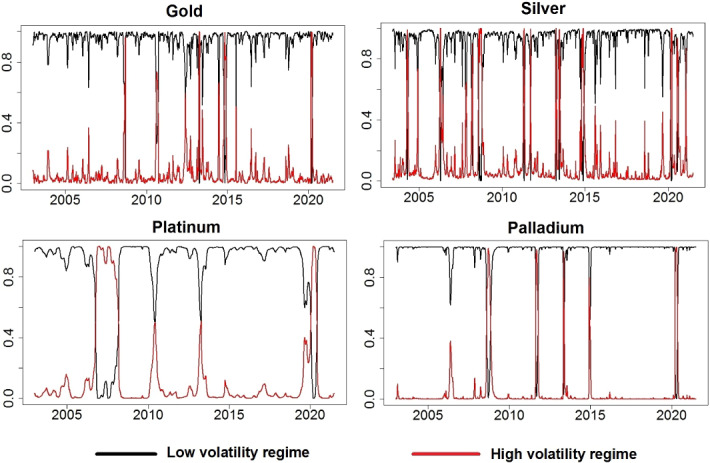

This paper researches two volatility transmission phenomena that take place within ('heat wave') and between ('meteor shower') spot and futures markets of four precious metals-gold, silver, platinum and palladium. We create conditional volatilities by considering three types of Markov switching GARCH models in combination with three different distribution functions. Conditional volatilities are subsequently embedded in Markov switching mean model. We find that 'heat wave' effect is more intense than 'meteor shower' effect, and this applies for both spot and futures markets of all precious metals. The results indicate that 'heat wave' effect is more intense in high than in low volatility periods, and also this effect is stronger in futures markets than in spot markets. 'Meteor shower' effect is stronger in low volatility regime than in high volatility regime, which is particularly true for the futures markets. Rolling regression results are in line with switching parameters. In addition, we find that 'meteor shower' effect, from futures to spot market, is stronger when short-term futures are analysed long-term futures.

本文研究了四种贵金属——黄金、白银、铂金和钯金的现货市场与期货市场内部(“热浪”)和之间(“流星雨”)发生的两种波动率传导现象。我们通过将三种类型的马尔可夫切换GARCH模型与三种不同的分布函数相结合来创建条件波动率。随后将条件波动率嵌入马尔可夫切换均值模型。我们发现,“热浪”效应比“流星雨”效应更强烈,这适用于所有贵金属的现货市场和期货市场。结果表明,“热浪”效应在高波动率时期比在低波动率时期更强烈,并且这种效应在期货市场中比在现货市场中更强。“流星雨”效应在低波动率状态下比在高波动率状态下更强,对于期货市场尤其如此。滚动回归结果与切换参数一致。此外,我们发现,当分析短期期货而非长期期货时,从期货市场到现货市场的“流星雨”效应更强。