Department of Health Policy and Management, Harvard T.H. Chan School of Public Health, Boston, Massachusetts.

Department of Health Policy, Vanderbilt University, Nashville, Tennessee.

JAMA Health Forum. 2021 Jun 14;2(6):e210771. doi: 10.1001/jamahealthforum.2021.0771. eCollection 2021 Jun.

The Affordable Care Act created 2 new coverage options for uninsured adults: Medicaid expansion, which in most states provides comprehensive coverage without premiums and deductibles; and private marketplace coverage, which requires a premium contribution and cost-sharing, though with generous federal subsidies at lower incomes. How enrollment rates compare in the marketplace vs Medicaid is an important policy question as states continue to weigh alternative coverage options such as Medicaid buy-in programs, enrolling Medicaid-eligible populations into marketplace plans, or creating a public option.

To assess the association between income eligibility for Medicaid vs marketplace coverage and insurance enrollment among low-income adults in Colorado.

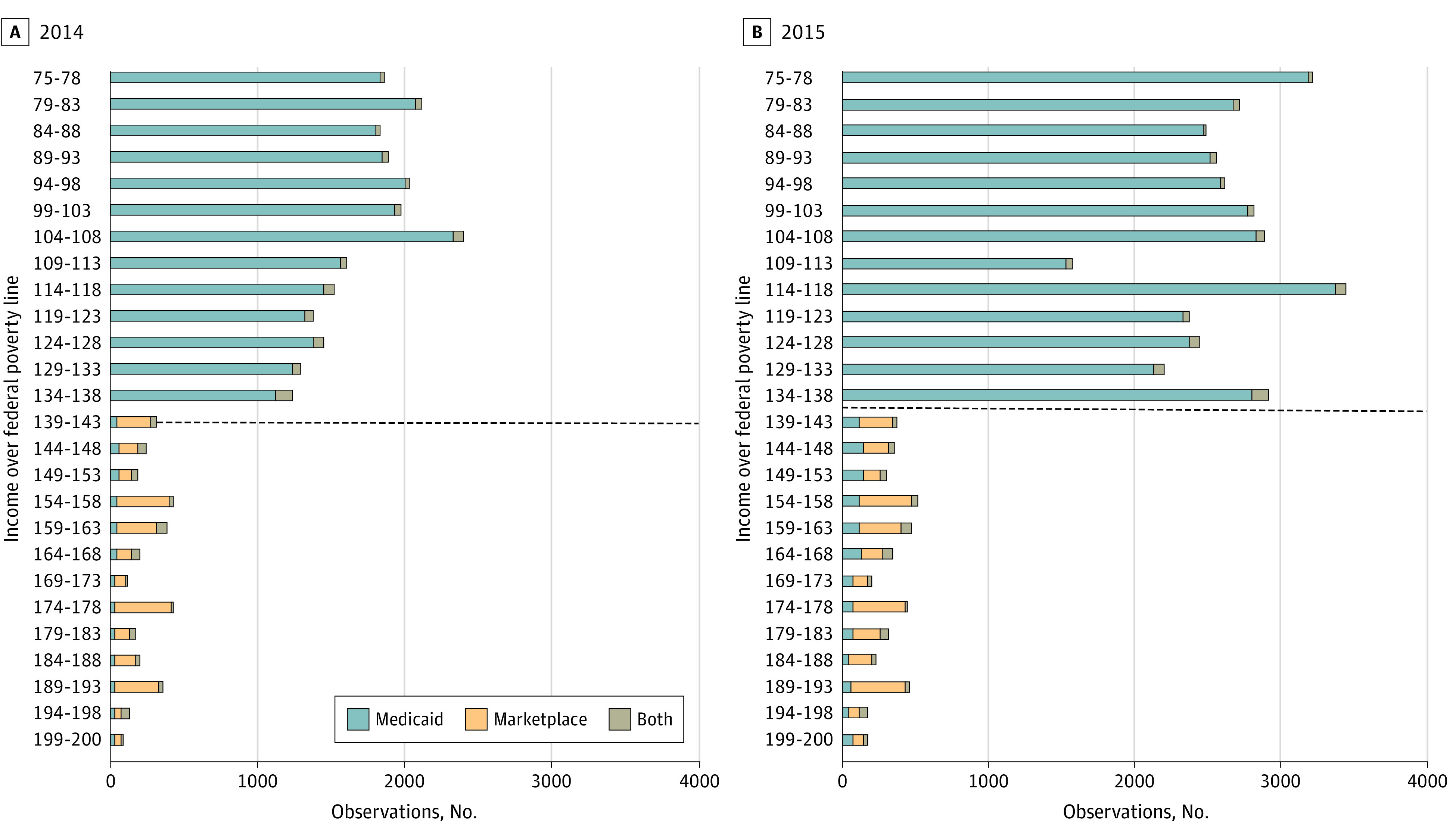

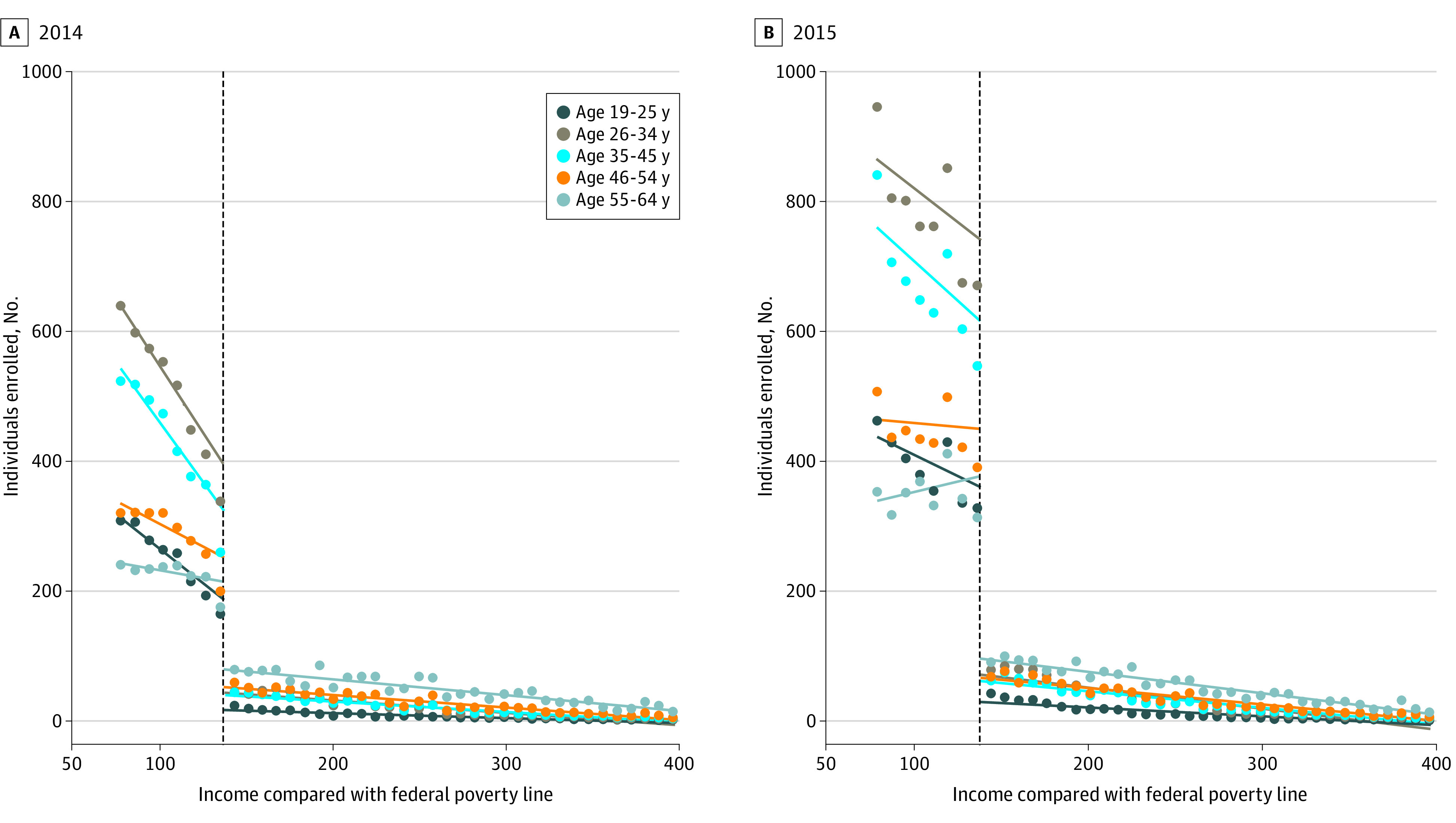

Using 2014 and 2015 all-payer claims data from Colorado and detailed income eligibility information, we used a regression discontinuity design to assess the difference in Medicaid and marketplace enrollment just below and just above 138% of the federal poverty level (FPL), the eligibility threshold between the 2 programs. The sample included nonpregnant adults aged 19 to 64 years with incomes between 75% to 400% FPL. We stratified our analysis by age, sex, chronic condition status, and urban vs rural residence. Analysis was conducted from January to October 2020.

The main outcome was total enrollment in either Medicaid or marketplace coverage during marketplace's Open Enrollment period. Income-based health insurance eligibility was assessed as a percentage of FPL at the time of initial application for coverage.

The primary analytical sample included 32 091 enrollees in 2014 and 55 451 in 2015, with incomes ranging from 120% to 156% FPL. Most enrollees were women (59.26% in 2014, 59.20% in 2015), resided in urban areas (70.36% in 2014, 73.08% in 2015), and had no chronic conditions (74.66% in 2014, 76.11% in 2015). For age, in 2014 and 2015, respectively, 13.22% and 13.93% were aged 19 to 25 years, 27.85% and 28.54% were aged 26 to 34 years, 23.58% and 24.34% were aged 35 to 44 years, 18.35% and 17.75% were aged 45 to 54 years, and 17.00% and 15.44% were aged 55 to 64 years. Marketplace enrollment was 81.3% (95% CI, -86.0% to -75.0%) lower than Medicaid enrollment in 2014 and 88.6% (95% CI, -90.8% to -86.0%) lower in 2015 among those close to the 138% FPL eligibility threshold. The drop-off in marketplace enrollment was largest among younger adults, aged 26 to 34 and 35 to 44 years: relative drop off -88.7% (95% CI, -93.3% to -80.8%) and -87.8% (95% CI, -90.8% to -83.9%) in 2014, and relative drop off -91.9% (95% CI, -94.5% to -87.9%) and -93.0% (95% CI, -94.5% to -91.1%) in 2015, respectively.

In this cross-sectional study using a regression-discontinuity analysis, meaningful gaps in insurance enrollment may have existed for those with incomes just above the eligibility threshold for Medicaid expansion, especially among younger adults. Policies expanding Medicaid income eligibility or zero-dollar premium marketplace plans are likely to be more effective at inducing enrollment than subsidized private plans with premium requirements.

平价医疗法案为无保险的成年人创造了 2 种新的保险选择:医疗补助扩展计划,该计划在大多数州提供全面保障,不收取保费和免赔额;私人市场保险,要求缴纳保费和共同支付费用,但在低收入者可以获得慷慨的联邦补贴。随着各州继续权衡替代保险选择,例如医疗补助购买计划、将符合医疗补助条件的人群纳入市场计划,或创建公共选择,市场与医疗补助的参保率比较是一个重要的政策问题。

评估科罗拉多州低收入成年人的收入是否符合医疗补助或市场保险资格与保险参保率之间的关联。

设计、地点和参与者:使用 2014 年和 2015 年科罗拉多州的所有支付者索赔数据和详细的收入资格信息,我们使用回归不连续性设计来评估联邦贫困水平(FPL)的 138%以下和以上的医疗补助和市场参保率之间的差异,138%是这两个计划的资格门槛。该样本包括年龄在 19 岁至 64 岁之间、收入在 FPL 的 75%至 400%之间的非孕妇成年人。我们按年龄、性别、慢性疾病状况和城市与农村居住情况对分析进行分层。分析于 2020 年 1 月至 10 月进行。

主要结果是在市场开放注册期间,市场保险和医疗补助的总参保率。基于收入的医疗保险资格按参保时收入占 FPL 的百分比评估。

主要分析样本包括 2014 年的 32091 名参保人和 2015 年的 55451 名参保人,收入范围从 FPL 的 120%到 156%。大多数参保人是女性(2014 年占 59.26%,2015 年占 59.20%),居住在城市地区(2014 年占 70.36%,2015 年占 73.08%),没有慢性疾病(2014 年占 74.66%,2015 年占 76.11%)。在年龄方面,2014 年和 2015 年分别有 13.22%和 13.93%的人年龄在 19 至 25 岁,27.85%和 28.54%的人年龄在 26 至 34 岁,23.58%和 24.34%的人年龄在 35 至 44 岁,18.35%和 17.75%的人年龄在 45 至 54 岁,17.00%和 15.44%的人年龄在 55 至 64 岁。2014 年,市场保险参保率比医疗补助参保率低 81.3%(95%CI,-86.0%至-75.0%),2015 年低 88.6%(95%CI,-90.8%至-86.0%),这是在接近 138%FPL 资格门槛的人群中。在市场保险参保率下降幅度最大的是 26 至 34 岁和 35 至 44 岁的年轻成年人:相对下降幅度分别为-88.7%(95%CI,-93.3%至-80.8%)和-87.8%(95%CI,-90.8%至-83.9%),2014 年和-91.9%(95%CI,-94.5%至-87.9%)和-93.0%(95%CI,-94.5%至-91.1%),2015 年。

在这项使用回归不连续性分析的横断面研究中,收入刚刚超过医疗补助扩大资格门槛的人,特别是年轻成年人,其保险参保率可能存在显著差距。扩大医疗补助收入资格或零保费市场保险计划的政策可能比有保费要求的补贴私人计划更有效地诱导参保。