Di Michael, Xu Ke

Department of Economics, University of Victoria, PO Box 1700 STN CSC, Victoria, BC V8N 2Y2 Canada.

Financ Res Lett. 2022 Dec;50:103289. doi: 10.1016/j.frl.2022.103289. Epub 2022 Aug 29.

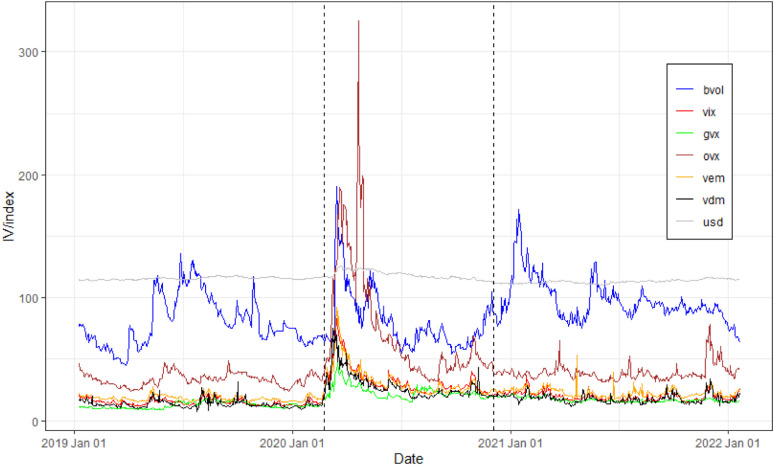

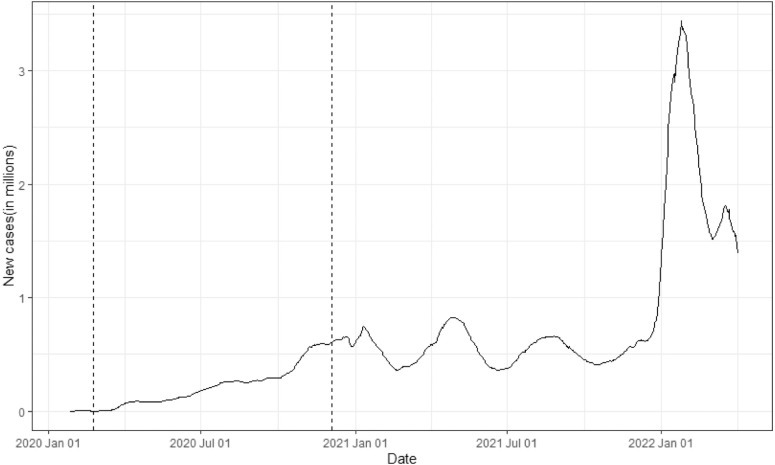

This paper examines implied volatility spillovers and connectedness between Bitcoin and a broad range of traditional financial assets (U.S. equity market, gold, crude oil, emerging markets and developing markets) from January 8, 2019 to January 20, 2022. Vector Auto-Regression and Generalized Forecast Error Variance Decomposition are used to compare results before COVID-19, during COVID-19 and after the vaccine becomes available. Results indicate higher connectedness during COVID-19 but very low connectedness after the vaccine is available, signaling recovery in financial markets. We also find that Bitcoin is a strong transmitter of volatility during COVID-19.

本文研究了2019年1月8日至2022年1月20日期间比特币与一系列传统金融资产(美国股票市场、黄金、原油、新兴市场和发展中市场)之间的隐含波动率溢出效应和关联性。运用向量自回归和广义预测误差方差分解来比较新冠疫情之前、疫情期间以及疫苗可用之后的结果。结果表明,在新冠疫情期间关联性较高,但在疫苗可用之后关联性非常低,这表明金融市场正在复苏。我们还发现,在新冠疫情期间比特币是波动率的一个强大传播者。