Palaios Panagiotis, Papapetrou Evangelia

Department of Accounting, Economics and Finance, The American College of Greece, Athens, Greece.

Department of Economics, National and Kapodistrian University of Athens, 1 Sofokleous Str, 10559 Athens, Greece.

J Econ Struct. 2022;11(1):30. doi: 10.1186/s40008-022-00291-7. Epub 2022 Dec 8.

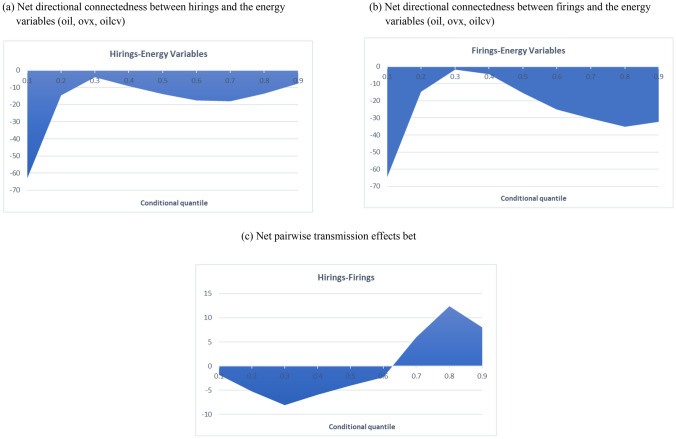

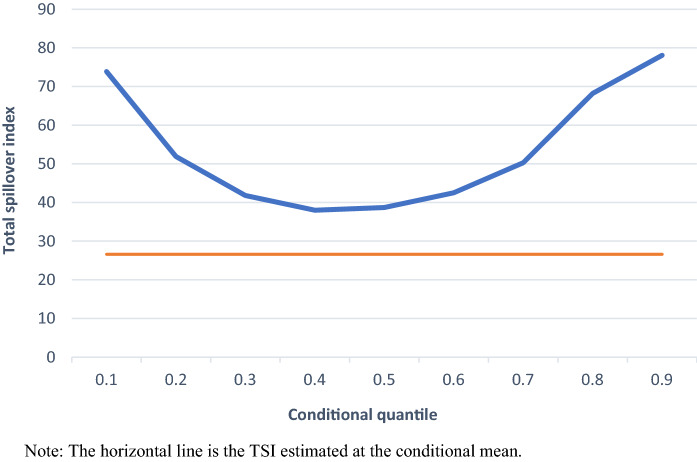

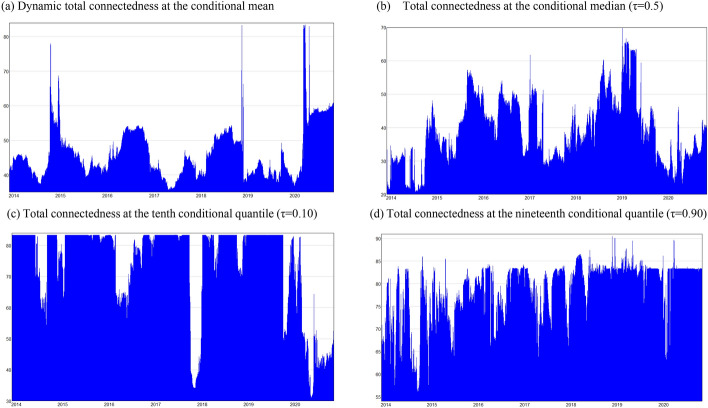

This paper examines the spillover effects transmission mechanism between oil prices, oil price uncertainty and oil price volatility on labour market in Greece, using static and dynamic quantile connectedness methodology (Diebold and Yilmaz Diebold and Yilmaz, Int J Forecast 28:57-66, 2012; Ando et al. Ando T, Greenwood-Nimmo N, Shin Y (2018) 'Quantile connectedness: Modelling tail behavior in the topology of financial networks', Working Paper. https://ssrn.com/abstract=3164772.). There is empirical evidence that the oil price variable is the most influential node of the energy variables on hirings and firings, suggesting the endogeneity of the labour market variables. Rolling estimation analysis based on the quantile VAR to capture the volatility spillovers across the whole conditional distribution shows a large variation of the total connectedness index, which is responsive to exogenous adverse and beneficial shocks. Further, our results point to a strong effect due to the COVID-19 pandemic and the state intervention to sustain the pandemic on the labour market. Overall, the analysis reveals a substantial higher time-varying connectedness of the system at the tails of the distribution, indicating that changes in energy markets asymmetrically affect the Greek labour market in recessionary and flourishing states of the economy, rather than normal times.

本文采用静态和动态分位数连通性方法(迪博尔德和伊尔马兹,《国际预测杂志》28:57 - 66,2012;安藤等人,安藤T、格林伍德 - 尼莫N、申Y(2018)“分位数连通性:金融网络拓扑中的尾部行为建模”,工作论文。https://ssrn.com/abstract=3164772.),研究了油价、油价不确定性和油价波动对希腊劳动力市场的溢出效应传导机制。有实证证据表明,油价变量是能源变量中对雇佣和解雇影响最大的节点,这表明劳动力市场变量存在内生性。基于分位数向量自回归的滚动估计分析用于捕捉整个条件分布上的波动溢出,结果显示总连通性指数变化很大,该指数对外生的不利和有利冲击有响应。此外,我们的结果表明,新冠疫情以及国家为应对疫情而进行的干预对劳动力市场产生了强烈影响。总体而言,分析揭示了该系统在分布尾部存在显著更高的时变连通性,这表明能源市场的变化在经济衰退和繁荣状态下对希腊劳动力市场产生不对称影响,而不是在正常时期。