School of Accounting, Xijing University, Xi'an City, Shaanxi Province, People's Republic of China.

Department of Economics and Management Sciences, NED University of Engineering & Technology, Karachi City, Pakistan.

PLoS One. 2023 Jun 20;18(6):e0287135. doi: 10.1371/journal.pone.0287135. eCollection 2023.

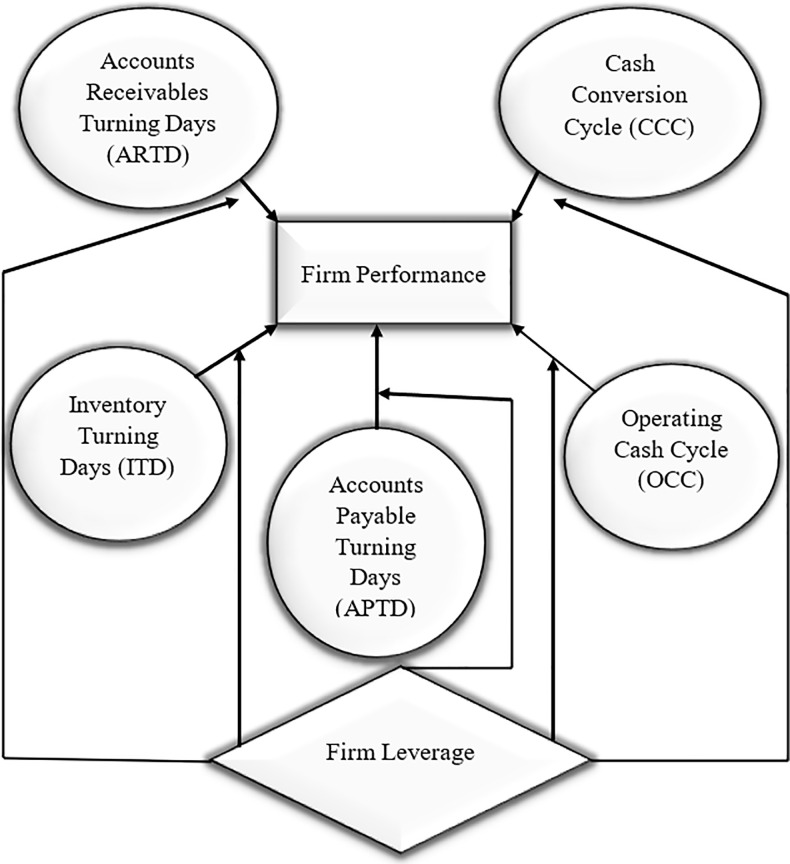

The main purpose of this research is to investigate the impact of changes in cash flow measures and metrics on firm financial performance. The study uses generalized estimating equations (GEEs) methodology to analyze longitudinal data for sample of 20288 listed Chinese non-financial firms from the period 2018:q2-2020:q1. The main advantage of GEEs method over other estimation techniques is its ability to robustly estimate the variances of regression coefficients for data samples that display high correlation between repeated measurements. The findings of study show that the decline in cash flow measures and metrics bring significant positive improvements in the financial performance of firms. The empirical evidence suggests that performance improvement levers (i.e. cash flow measures and metrics) are more pronounced in low leverage firms, suggesting that changes in cash flow measures and metrics bring more positive changes in low leverage firms' financial performance relatively to high leveraged firms. The results hold after mitigating endogeneity based on dynamic panel system generalized method of moments (GMM) and sensitivity analysis considering the robustness of main findings. The paper makes significant contribution to the literature related to cash flow management and working capital management. Since, this paper is among few to empirically study, how cash flow measures and metrics are related to firm performance from dynamic stand point especially from the context of Chinese non-financial firms.

本研究的主要目的是探讨现金流计量和指标的变化对企业财务绩效的影响。本研究采用广义估计方程(GEEs)方法,对 2018 年第二季度至 2020 年第一季度期间的 20288 家中国非金融上市公司的样本进行了纵向数据分析。GEEs 方法相对于其他估计技术的主要优势在于,它能够稳健地估计具有高度相关性的重复测量数据样本的回归系数方差。研究结果表明,现金流计量和指标的下降带来了企业财务绩效的显著积极改善。实证证据表明,在低杠杆率企业中,业绩提升杠杆(即现金流计量和指标)更为明显,这表明现金流计量和指标的变化相对于高杠杆率企业而言,在低杠杆率企业的财务绩效中带来了更为积极的变化。在基于动态面板系统广义矩估计(GMM)和考虑主要发现稳健性的敏感性分析缓解内生性问题后,结果仍然成立。本文为现金流管理和营运资金管理相关文献做出了重要贡献。因为,本文是少数从动态角度,特别是从中国非金融企业的角度,实证研究现金流计量和指标与企业绩效之间关系的论文之一。