Adegunsoye Emmanuel Adebayo, Tijani Akeem Abiade, Kolapo Adetomiwa

Department of Agricultural Economics, Obafemi Awolowo University, Ile-Ife, Nigeria.

Heliyon. 2024 Jun 8;10(12):e32741. doi: 10.1016/j.heliyon.2024.e32741. eCollection 2024 Jun 30.

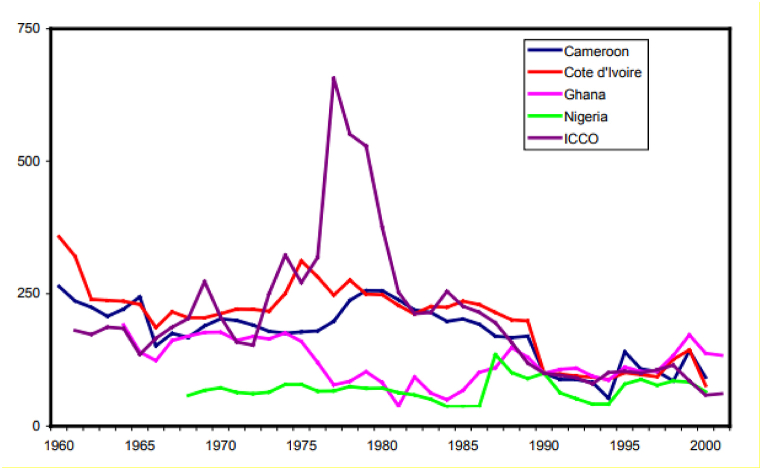

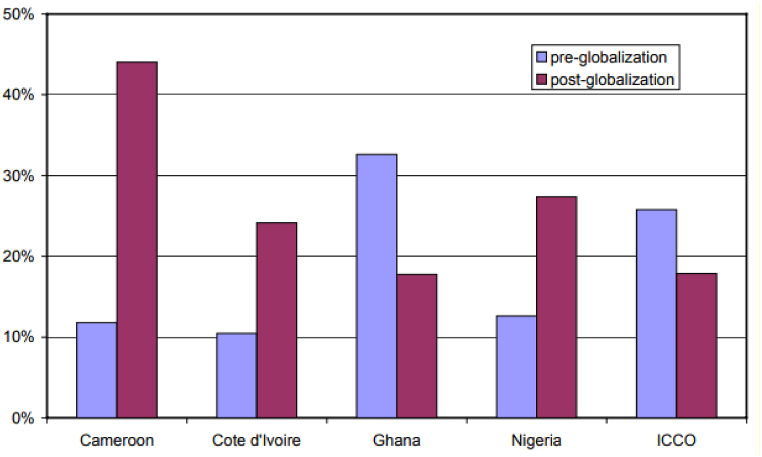

Cocoa producers respond differently to volatile price shocks, but the nature of these responses remains unknown, especially in the liberalized and non-liberalized markets in Nigeria and Ghana, respectively. Therefore, we assess the extent to which price volatility affects the supply of cocoa while also analyzing the effect of price volatility on Nigeria's cocoa producer price share vis-à-vis Ghana's cocoa producer price share. We further analyze how producers react given the asymmetric nature of price volatility in Nigeria and Ghana. Annual secondary data were obtained from the World Development Index, National Bureau of Statistics, International Cocoa Organization, Central Bank of Ghana, Nigeria, and so on, from 1970 to 2019. We used the Ordinary Least Squares method, generalized autoregressive conditional heteroskedastic (GARCH) model, extensions, and the Vector Error Correction Model (VECM) for this study's analysis. Our results show the presence of volatility in price series and that volatility is asymmetric in nature. The results of the supply response show that price volatility has no significant relationship with cocoa supply in Ghana. In contrast, price volatility has a significantly positive relationship with the supply of cocoa in Nigeria at the 1 % level. The results of the VECM show that, in the long run, the cocoa producer price in Ghana will be negatively affected by both international price volatility and inflation rates at 5 % and 1 %, respectively. We suggest that cocoa farmers should have licensing to sell commodities to the international market directly without interference from the marketing board.

可可生产国对价格波动冲击的反应各不相同,但这些反应的性质仍然未知,尤其是在尼日利亚和加纳分别实行自由化和非自由化的市场中。因此,我们评估价格波动对可可供应的影响程度,同时分析价格波动对尼日利亚可可生产者价格份额相对于加纳可可生产者价格份额的影响。我们还进一步分析了鉴于尼日利亚和加纳价格波动的不对称性质,生产者是如何做出反应的。年度二手数据取自世界发展指数、各国统计局、国际可可组织、加纳中央银行、尼日利亚中央银行等,时间跨度为1970年至2019年。我们使用普通最小二乘法、广义自回归条件异方差(GARCH)模型、扩展模型以及向量误差修正模型(VECM)进行本研究的分析。我们的结果表明价格序列存在波动,且波动在性质上是不对称的。供应反应结果表明,价格波动与加纳的可可供应没有显著关系。相比之下,价格波动与尼日利亚的可可供应在1%的水平上存在显著的正相关关系。向量误差修正模型的结果表明,从长期来看,加纳的可可生产者价格将分别受到国际价格波动和通货膨胀率的负面影响,影响程度分别为5%和1%。我们建议可可农民应该获得许可,以便在不受营销委员会干扰的情况下直接向国际市场销售商品。