Computational Biology and Machine Learning, Center for Cancer Research and Cell Biology, School of Medicine, Dentistry and Biomedical Sciences, Queen's University Belfast, Belfast, United Kingdom.

PLoS One. 2010 Sep 30;5(9):e12884. doi: 10.1371/journal.pone.0012884.

In this paper we investigate the definition and formation of financial networks. Specifically, we study the influence of the time scale on their construction.

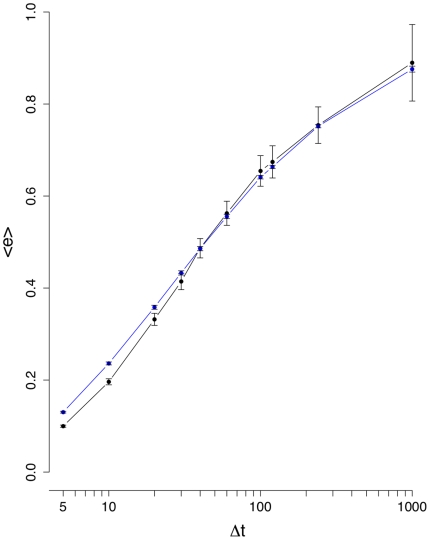

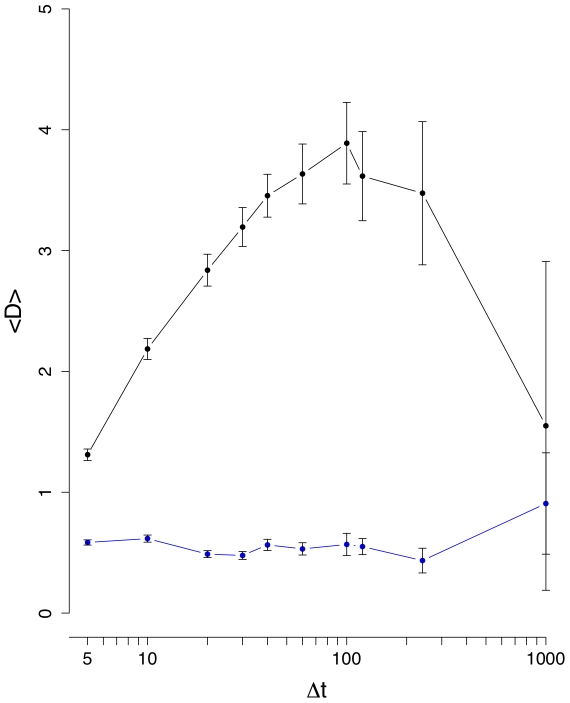

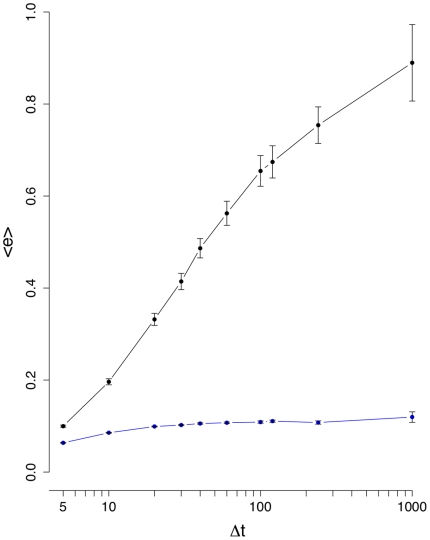

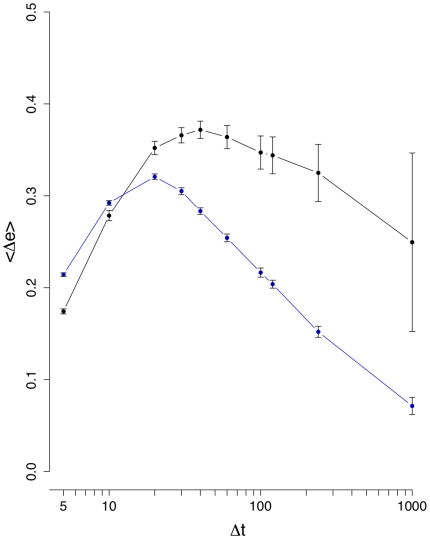

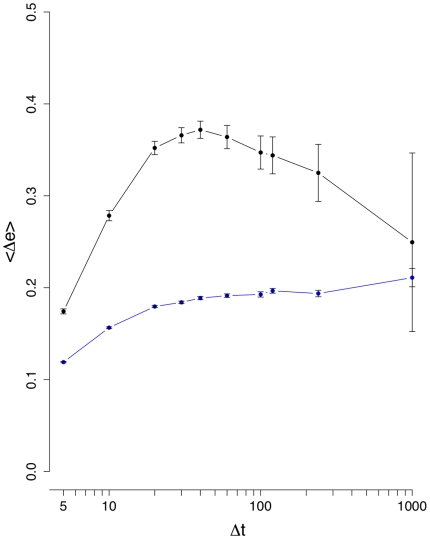

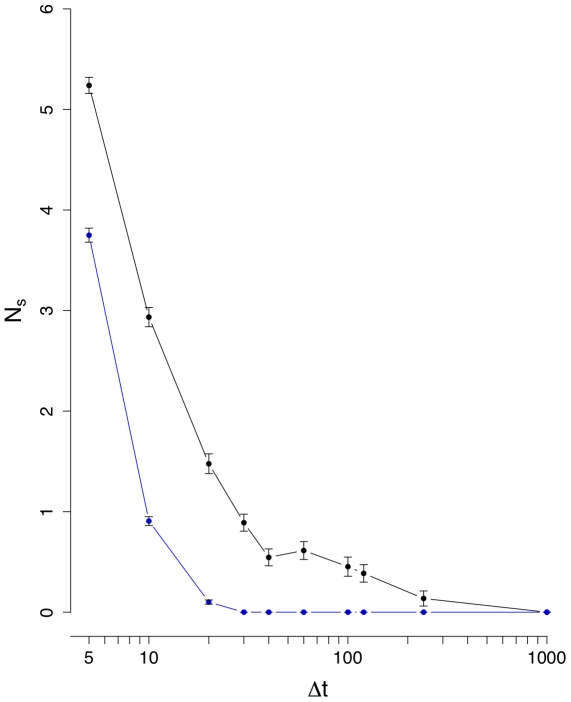

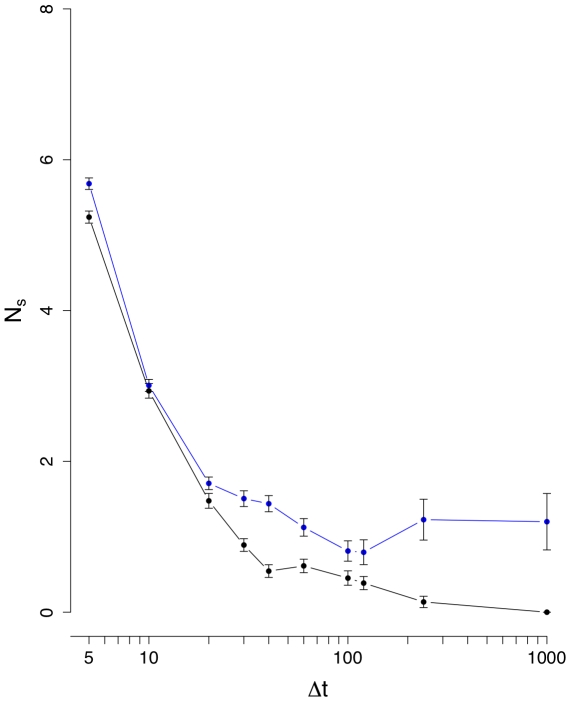

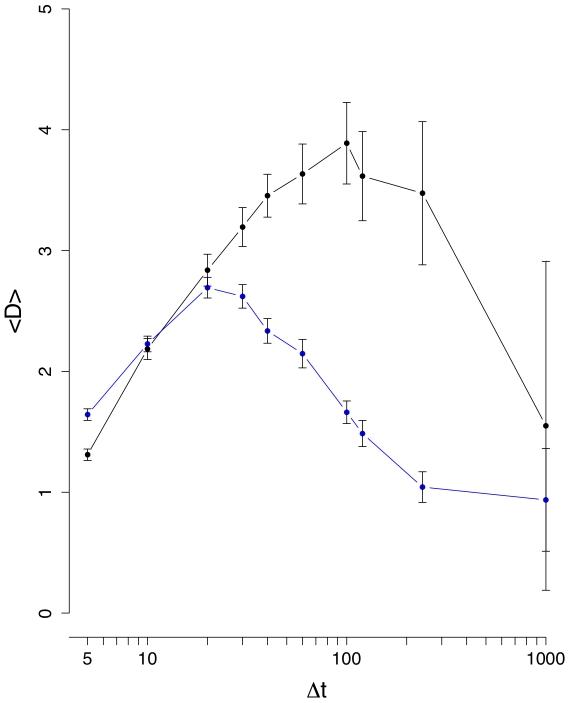

METHODOLOGY/PRINCIPAL FINDINGS: For our analysis we use correlation-based networks obtained from the daily closing prices of stock market data. More precisely, we use the stocks that currently comprise the Dow Jones Industrial Average (DJIA) and estimate financial networks where nodes correspond to stocks and edges correspond to none vanishing correlation coefficients. That means only if a correlation coefficient is statistically significant different from zero, we include an edge in the network. This construction procedure results in unweighted, undirected networks. By separating the time series of stock prices in non-overlapping intervals, we obtain one network per interval. The length of these intervals corresponds to the time scale of the data, whose influence on the construction of the networks will be studied in this paper.

CONCLUSIONS/SIGNIFICANCE: Numerical analysis of four different measures in dependence on the time scale for the construction of networks allows us to gain insights about the intrinsic time scale of the stock market with respect to a meaningful graph-theoretical analysis.

本文研究金融网络的定义和形成。具体而言,我们研究了时间尺度对其构建的影响。

方法/主要发现:我们使用基于相关的网络进行分析,这些网络来自股票市场数据的每日收盘价。更确切地说,我们使用当前构成道琼斯工业平均指数(DJIA)的股票,并估计金融网络,其中节点对应于股票,边对应于非零相关系数。这意味着只有当相关系数在统计学上显著不同于零时,我们才会在网络中包含一条边。这种构建过程产生了无权重、无向的网络。通过将股票价格的时间序列分割成不重叠的区间,我们为每个区间获得一个网络。这些区间的长度对应于数据的时间尺度,本文将研究该时间尺度对网络构建的影响。

结论/意义:对构建网络的时间尺度上的四个不同度量的数值分析,使我们能够深入了解股票市场的内在时间尺度,以便进行有意义的图论分析。