Navrongo Health Research Centre, Ghana Health Service, P, O, Box 114, Navrongo, Ghana.

Int J Equity Health. 2011 Jun 27;10:26. doi: 10.1186/1475-9276-10-26.

Financial protection against the cost of unforeseen ill health has become a global concern as expressed in the 2005 World Health Assembly resolution (WHA58.33), which urges its member states to "plan the transition to universal coverage of their citizens". An important element of financial risk protection is to distribute health care financing fairly in relation to ability to pay. The distribution of health care financing burden across socio-economic groups has been estimated for European countries, the USA and Asia. Until recently there was no such analysis in Africa and this paper seeks to contribute to filling this gap. It presents the first comprehensive analysis of the distribution of health care financing in relation to ability to pay in Ghana.

Secondary data from the Ghana Living Standard Survey (GLSS) 2005/2006 were used. This was triangulated with data from the Ministry of Finance and other relevant sources, and further complemented with primary household data collected in six districts. We implored standard methodologies (including Kakwani index and test for dominance) for assessing progressivity in health care financing in this paper.

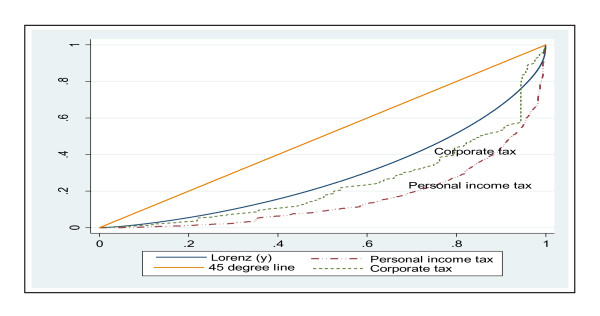

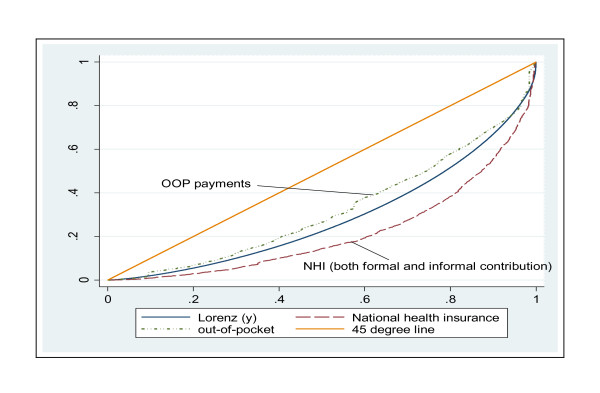

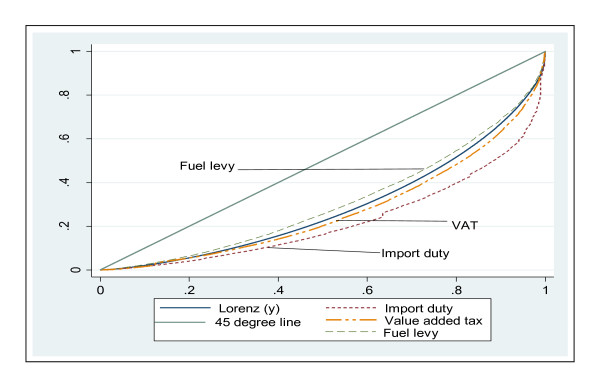

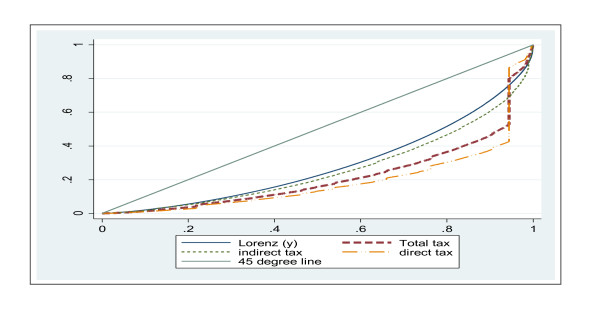

Ghana's health care financing system is generally progressive. The progressivity of health financing is driven largely by the overall progressivity of taxes, which account for close to 50% of health care funding. The national health insurance (NHI) levy (part of VAT) is mildly progressive and formal sector NHI payroll deductions are also progressive. However, informal sector NHI contributions were found to be regressive. Out-of-pocket payments, which account for 45% of funding, are regressive form of health payment to households.

For Ghana to attain adequate financial risk protection and ultimately achieve universal coverage, it needs to extend pre-payment cover to all in the informal sector, possibly through funding their contributions entirely from tax, and address other issues affecting the expansion of the National Health Insurance. Furthermore, the pre-payment funding pool for health care needs to grow so budgetary allocation to the health sector can be enhanced.

正如 2005 年世界卫生大会决议(WHA58.33)所表达的那样,防范无法预见的健康不良所带来的费用的财务保障已成为全球关注的问题,该决议敦促其成员国“计划向其公民普及覆盖”。财务风险保护的一个重要内容是按照支付能力公平分配医疗保健融资。已经对欧洲国家、美国和亚洲的医疗保健融资负担在社会经济群体中的分配情况进行了估计。直到最近,非洲还没有进行此类分析,本文旨在为此做出贡献。本文首次全面分析了加纳与支付能力相关的医疗保健融资分配情况。

使用了来自加纳生活水平调查(GLSS)2005/2006 的二级数据。这些数据与财政部和其他相关来源的数据进行了三角剖分,并进一步使用在六个地区收集的主要家庭数据进行了补充。我们在本文中使用了标准方法(包括卡卡温指数和优势检验)来评估医疗保健融资的累进性。

加纳的医疗保健融资系统总体上是累进的。医疗融资的累进性主要是由税收的整体累进性驱动的,税收占医疗保健资金的近 50%。国家健康保险(NHI)税(增值税的一部分)略有累进性,正规部门 NHI 工资扣除也具有累进性。然而,非正式部门的 NHI 缴费被发现是倒退的。占资金 45%的自付费用是向家庭提供医疗服务的倒退形式的支付。

为了使加纳实现充分的财务风险保护并最终实现全民覆盖,它需要通过完全从税收中为其缴费提供资金,将预付款覆盖范围扩大到所有非正式部门,并解决影响国家健康保险扩大的其他问题。此外,医疗保健预付款融资池需要增长,以便能够增加对卫生部门的预算分配。