Li Shouwei, Xu Tao, He Jianmin

School of Economics and Management, Southeast University, Nanjing, 211189 China.

Springerplus. 2016 Sep 13;5(1):1535. doi: 10.1186/s40064-016-3203-4. eCollection 2016.

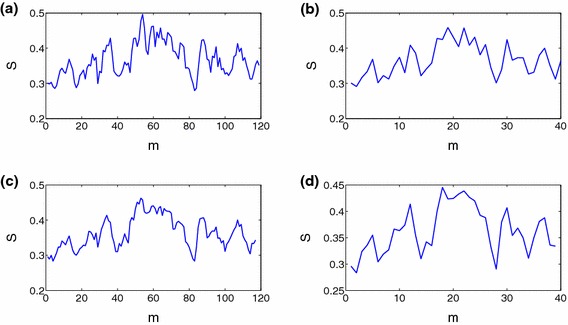

In this paper, we adopt the network synchronization to measure the collective behavior in the financial market, and then analyze the factors that affect the collective behavior. Based on the data from the Chinese financial market, we find that the clustering coefficient, the average shortest path length and the volatility fluctuation have a positive effect on the collective behavior respectively, while the average return has a negative effect on it; the effect of the average shortest path length on the collective behavior is the greatest in the above four variables; the above results are robust against the window size and the time interval between adjacent windows of the stock network; the effect of network structures and stock market properties on the collective behavior during the financial crisis is the same as those during other periods.

在本文中,我们采用网络同步来度量金融市场中的集体行为,进而分析影响集体行为的因素。基于中国金融市场的数据,我们发现聚类系数、平均最短路径长度和波动率波动分别对集体行为有正向影响,而平均回报率对集体行为有负向影响;在上述四个变量中,平均最短路径长度对集体行为的影响最大;上述结果对于股票网络的窗口大小和相邻窗口之间的时间间隔具有稳健性;金融危机期间网络结构和股票市场属性对集体行为的影响与其他时期相同。