Harkin Ben

Department of Psychology, University of Sheffield, Western Bank Sheffield, UK.

Front Psychol. 2017 Mar 7;8:327. doi: 10.3389/fpsyg.2017.00327. eCollection 2017.

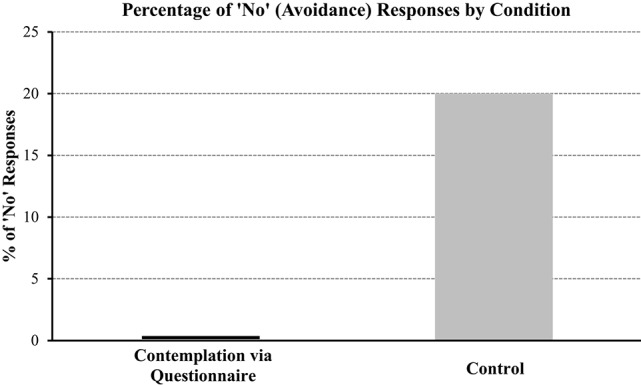

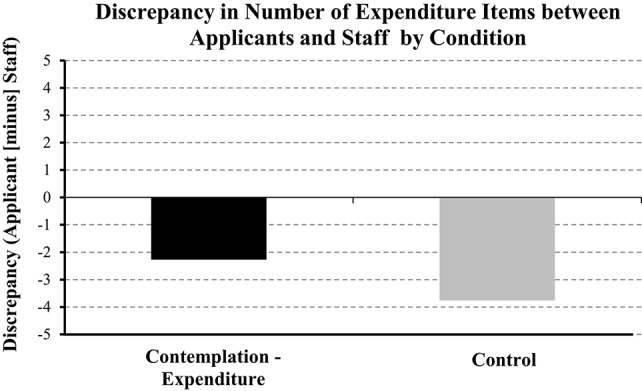

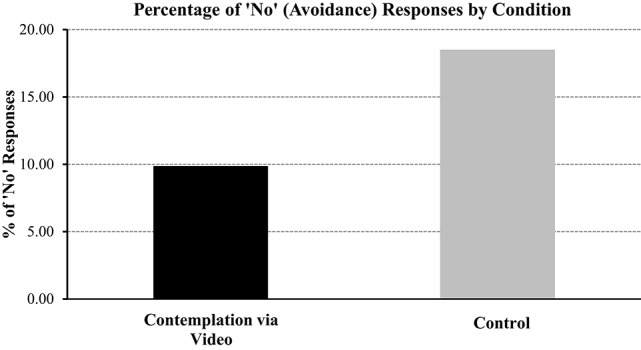

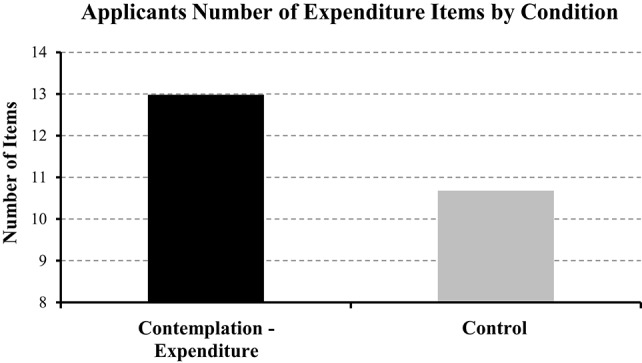

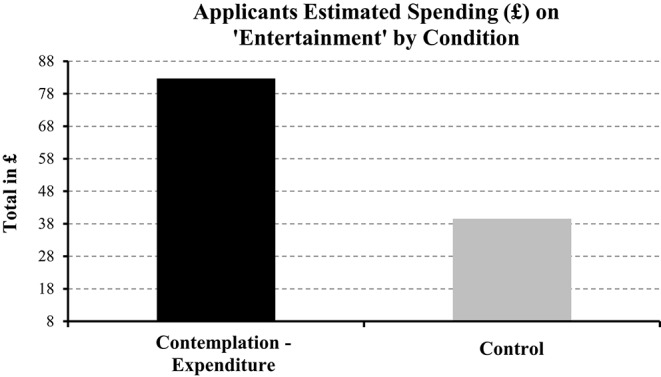

The present research tackles two main areas of financial mismanagement, namely avoiding debt-related information and underestimating expenditure. We draw upon research which has shown that inviting people to think about reasons for avoiding something actually serves to reduce the likelihood that they will then avoid it, and potentially improves what they know about it. Therefore, in three studies we investigated if prompting participants to contemplate their debt (Studies 1 and 2) and expenditure (Study 3) would decrease avoidance of debt-related information and improve estimates of expenditure, respectively. Conform to our expectations prompting contemplation via questionnaire (Study 1) and video (Study 2) reduced avoidance of debt-related information. In other words, contemplation reduced the likelihood that people would avoid viewing their risk of debt. The success of prompting contemplation via video offers a new and important addition to the literature on contemplation, which has previously focused on using the traditional questionnaire format. In Study 3 we observed that contemplation improved the estimates of expenditure that loan applicants at a credit union provided. Specifically, contemplation resulted in participants providing larger and more detailed accounts of their expenditure, and increased the agreement between staff and clients for the number of expenditure items provided by the clients. In sum, these findings suggest that contemplation in the context of the above financial decision-making is a robust intervention, as it was effective for different types of interventions (questionnaire and video), behaviors (avoidance of debt-related information and improving estimates of expenditure), and samples (students and university staff; Studies 1 and 2 loan applicants at a credit union; Study 3). We discuss the theoretical, policy and applied impact of these findings, and highlight limitations and considerations for future research.

本研究探讨了财务管理不善的两个主要方面,即回避债务相关信息和低估支出。我们借鉴了相关研究,该研究表明,邀请人们思考回避某事物的原因实际上有助于降低他们随后回避该事物的可能性,并有可能增进他们对该事物的了解。因此,在三项研究中,我们调查了促使参与者思考他们的债务(研究1和2)和支出(研究3)是否会分别减少对债务相关信息的回避并改善支出估计。正如我们所期望的,通过问卷调查(研究1)和视频(研究2)促使参与者思考,减少了对债务相关信息的回避。换句话说,思考降低了人们回避查看自己债务风险的可能性。通过视频促使思考的成功为关于思考的文献增添了新的重要内容,此前该文献主要集中在使用传统的问卷形式。在研究3中,我们观察到思考改善了信用合作社贷款申请人提供的支出估计。具体而言,思考使参与者能够提供更详细的支出账目,并增加了工作人员与客户在客户提供的支出项目数量上的一致性。总之,这些发现表明,在上述财务决策背景下的思考是一种有力的干预措施,因为它对不同类型的干预措施(问卷和视频)、行为(回避债务相关信息和改善支出估计)以及样本(学生和大学工作人员;研究1和2 信用合作社的贷款申请人;研究3)都有效。我们讨论了这些发现的理论、政策和应用影响,并强调了局限性以及对未来研究的考虑。