Department of Health Policy and Management, Harvard T. H. Chan School of Public Health, Boston, Massachusetts.

Department of Information, Decisions and Operations, The Wharton School, University of Pennsylvania, Philadelphia.

JAMA Netw Open. 2018 Sep 7;1(5):e182008. doi: 10.1001/jamanetworkopen.2018.2008.

Financial incentives shared between physicians and patients were shown to significantly reduce low-density lipoprotein cholesterol (LDL-C) levels in a randomized clinical trial, but it is not known whether these health benefits are worth the added incentive and utilization costs required to achieve them.

To evaluate the long-term cost-effectiveness of financial incentives on LDL-C level control.

DESIGN, SETTING, AND PARTICIPANTS: In this economic evaluation, a previously validated microsimulation computer model was parameterized using individual-level data from the randomized clinical trial on financial incentives, National Health and Nutrition Examination Surveys for model population inputs, and other published sources. The study was conducted from April 15, 2016, to March 29, 2018.

The following interventions were used: (1) usual care, (2) trial control strategy (increased cholesterol level monitoring and use of electronic pill bottles), (3) financial incentives for physicians, (4) financial incentives for patients, and (5) incentives shared between physicians and patients.

Discounted costs (2017 US dollars), lifetime cardiovascular disease risk, quality-adjusted life-years (QALYs), and incremental cost-effectiveness ratios (ICERs).

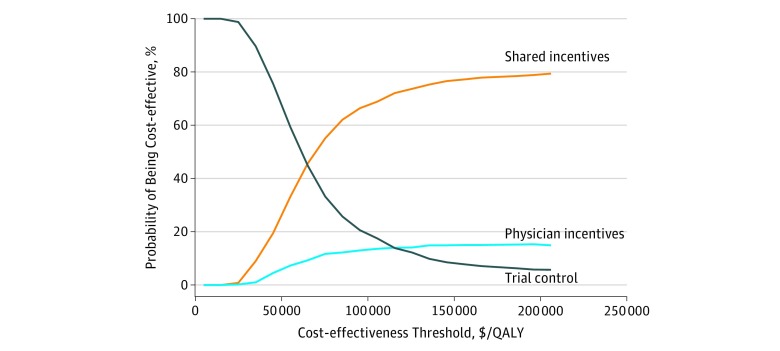

The model population (n = 1 000 000 [30.7% women]) had similar mean (SD) age (61.5 [11.9] years) and LDL-C level (153.9 mg/dL) as the observed trial population (n = 1503 [42.7% women]; age, 62.0 [8.7] years; and LDL-C level, 160.6 mg/dL). Using base-case assumptions (including a 10-year waning period of LDL-C level reductions), the usual-care strategy was dominated (higher costs and lower QALYs) by all other strategies. Strategies for physician- or patient-only incentives were dominated by the shared-incentives strategy, which had an ICER of $60 000/QALY compared with the trial control strategy. In a sensitivity analysis regarding the duration of LDL-C level reductions, the shared-incentives strategy remained cost-effective (ICERs <$100 000/QALY and <$150 000/QALY) for scenarios with LDL-C level reductions lasting, with linear waning, at least 7 and 5 years, respectively. In the 1-way sensitivity analysis for the time horizon of the analysis, the ICER of the shared-incentives strategy exceeded $100 000/QALY at 11 years and $150 000/QALY at 8 years. In probabilistic sensitivity analysis, the shared-incentives intervention was cost-effective in 69% to 77% of iterations using cost-effectiveness thresholds of $100 000 to $150 000/QALY. Cost-effectiveness results were also sensitive to the duration of intervention costs.

This study suggests that the financial incentives shared between patients and physicians for LDL-C level control meet conventional standards of cost-effectiveness, but these results appeared to be sensitive to assumptions about the durations of LDL-C level reductions and years of intervention costs included, as well as to the choice of time horizon.

随机临床试验表明,医生和患者之间的财务激励措施可显著降低低密度脂蛋白胆固醇(LDL-C)水平,但尚不清楚这些健康益处是否值得实现这些目标所需的额外激励措施和利用成本。

评估财务激励措施对 LDL-C 水平控制的长期成本效益。

设计、设置和参与者:在这项经济评估中,使用来自财务激励措施随机临床试验的个体水平数据、国家健康和营养检查调查的模型人群输入以及其他已发表的来源,对先前经过验证的微模拟计算机模型进行了参数化。该研究于 2016 年 4 月 15 日至 2018 年 3 月 29 日进行。

使用以下干预措施:(1)常规护理,(2)试验对照策略(增加胆固醇水平监测和使用电子药瓶),(3)医生的财务激励,(4)患者的财务激励,以及(5)医生和患者之间的激励共享。

贴现成本(2017 年美元)、终生心血管疾病风险、质量调整生命年(QALYs)和增量成本效益比(ICERs)。

模型人群(n=100 万[30.7%为女性])的平均(标准差)年龄(61.5[11.9]岁)和 LDL-C 水平(153.9mg/dL)与观察试验人群(n=1503[42.7%为女性];年龄 62.0[8.7]岁;LDL-C 水平 160.6mg/dL)相似。使用基本假设(包括 LDL-C 水平降低的 10 年衰减期),常规护理策略(成本更高,QALYs 更低)被所有其他策略所主导。仅针对医生或患者的激励策略被共享激励策略所主导,与试验对照策略相比,其 ICER 为 60000 美元/QALY。在关于 LDL-C 水平降低持续时间的敏感性分析中,对于 LDL-C 水平降低持续时间至少为 7 年和 5 年的情况,共享激励策略仍然具有成本效益(ICERs<100000 美元/QALY 和 <150000 美元/QALY),且呈线性衰减。在分析时间范围的 1 种敏感性分析中,共享激励策略的 ICER 在 11 年内超过 100000 美元/QALY,在 8 年内超过 150000 美元/QALY。在概率敏感性分析中,使用 100000 美元至 150000 美元/QALY 的成本效益阈值,共享激励干预在 69%至 77%的迭代中具有成本效益。成本效益结果也对 LDL-C 水平降低持续时间和包括的干预成本年限以及选择时间范围的假设敏感。

这项研究表明,医生和患者之间共享的 LDL-C 水平控制财务激励措施符合成本效益的常规标准,但这些结果似乎对 LDL-C 水平降低的持续时间和包括的干预成本年限以及时间范围的选择假设敏感。