Philip R. Lee Institute for Health Policy Studies, University of California San Francisco, CA, USA; Department of Psychiatry and Weill Institute for Neuroscience, University of California San Francisco, CA, USA.

Philip R. Lee Institute for Health Policy Studies, University of California San Francisco, CA, USA.

Drug Alcohol Depend. 2019 Apr 1;197:8-14. doi: 10.1016/j.drugalcdep.2019.01.001. Epub 2019 Feb 5.

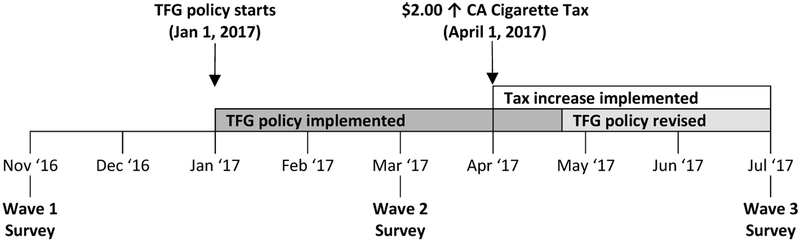

This study examined the impact of a tobacco-free grounds (TFG) policy and the California $2.00/pack tobacco tax increase on tobacco use among individuals in residential substance use disorder (SUD) treatment.

We conducted three cross-sectional surveys of clients enrolled in three residential SUD treatment programs. Wave 1 (Pre-TFG) included 190 clients, wave 2 (post-TFG and pre-tax increase) included 200 clients, and wave 3 (post-tax increase) included 201 clients. Demographic and tobacco-use characteristics were first compared between waves using bivariate comparisons. Regression models were used to compare each outcome with survey wave as the predictor, while adjusting for demographic characteristics and nesting of participants within programs.

Odds of clients being current smokers was lower (AOR = 0.43, 95%CI = 0.30,0.60) after implementation of TFG compared to baseline. Adjusted mean ratio (AMR) for cigarettes per day was lower post-TFG compared to baseline (AMR = 0.70, CI = 0.59, 0.83). There were no differences, across waves, in tobacco-related knowledge, attitudes, or services received by program clients, or use of nicotine replacement therapy. Increased cigarette taxation was not associated with reductions in client smoking.

Implementation of a TFG policy was associated with a lower prevalence of client smoking among individuals in residential SUD treatment. Increased state cigarette excise taxes were not associated with a further reduction in client smoking in the presence of TFG policies, though this may have been confounded by relaxing of the TFG policy. SUD treatment programs should promote TFG policies and increase tobacco cessation services for clients.

本研究考察了禁烟区(TFG)政策和加利福尼亚州每包 2.00 美元的烟草税增加对居住在物质使用障碍(SUD)治疗中的个体的烟草使用的影响。

我们对参加三个住院 SUD 治疗项目的患者进行了三次横断面调查。第 1 波(TFG 前)包括 190 名患者,第 2 波(TFG 后和税收增加前)包括 200 名患者,第 3 波(税收增加后)包括 201 名患者。使用双变量比较比较了各波之间的人口统计学和烟草使用特征。使用回归模型比较了每个结果与调查波作为预测因子的情况,同时调整了参与者在项目中的人口统计学特征和嵌套情况。

与基线相比,TFG 实施后,客户目前吸烟的可能性较低(OR=0.43,95%CI=0.30,0.60)。与基线相比,TFG 后每天的香烟数量调整平均比(AMR)较低(AMR=0.70,CI=0.59,0.83)。在各个波次之间,项目客户的烟草相关知识、态度或接受的服务或尼古丁替代疗法的使用方面没有差异。增加香烟税并没有导致客户吸烟减少。

实施 TFG 政策与居住在 SUD 治疗中的个体中客户吸烟率降低有关。在 TFG 政策存在的情况下,增加州香烟消费税并未与客户吸烟进一步减少相关联,尽管这可能因 TFG 政策的放宽而受到混淆。SUD 治疗计划应促进 TFG 政策并为客户增加戒烟服务。