Department of Financial Engineering, Ajou University, Yeongtong-gu, Suwon, Republic of Korea.

Department of Data Science, Ajou University, Yeongtong-gu, Suwon, Republic of Korea.

PLoS One. 2019 Feb 15;14(2):e0212320. doi: 10.1371/journal.pone.0212320. eCollection 2019.

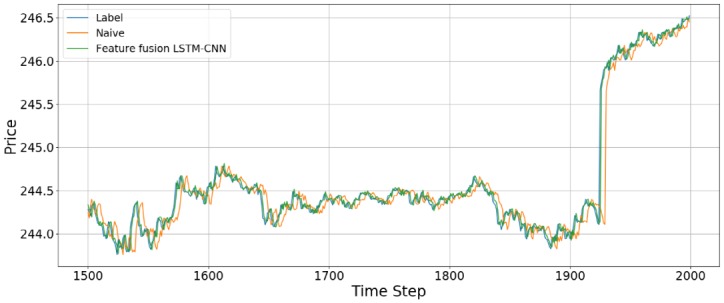

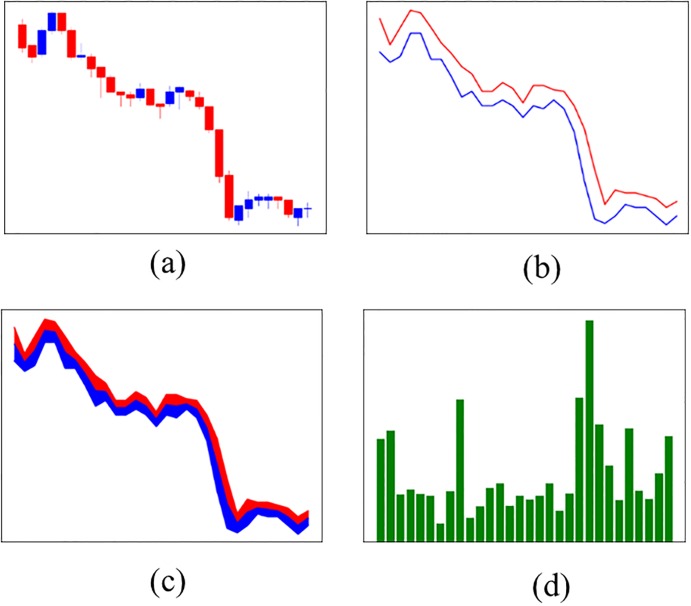

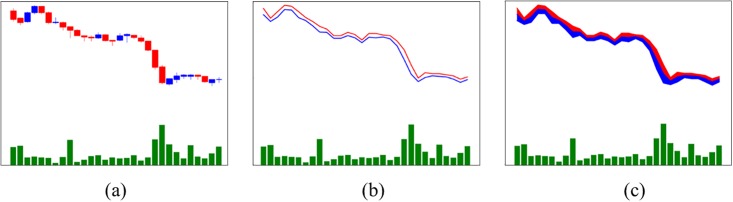

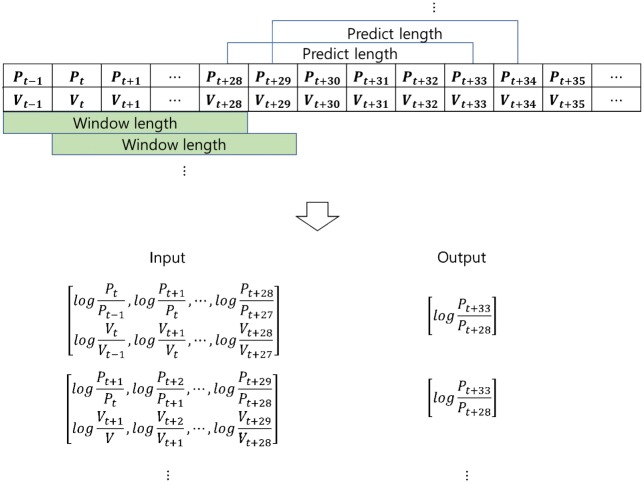

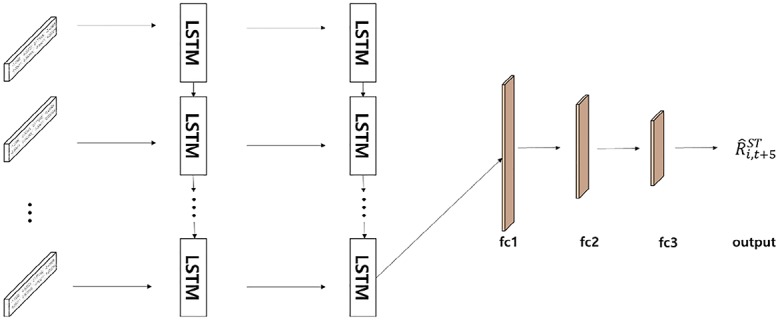

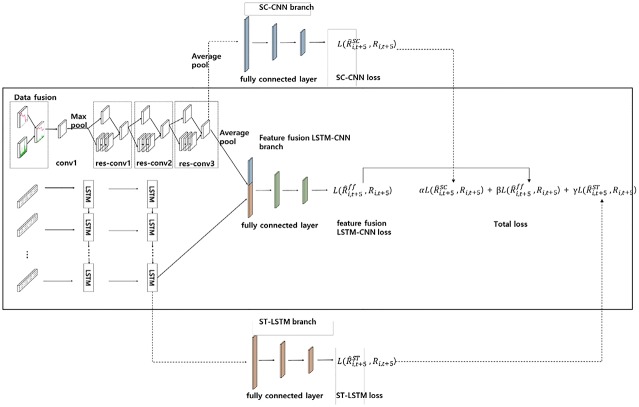

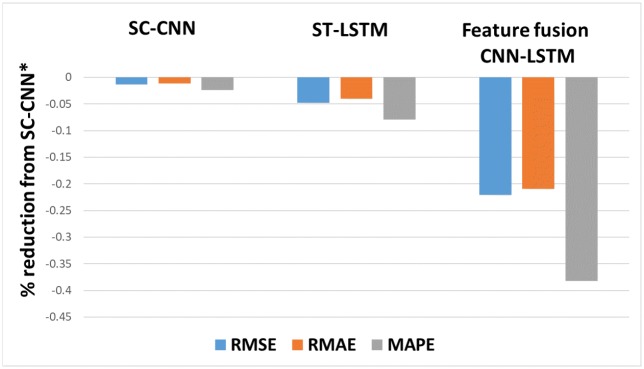

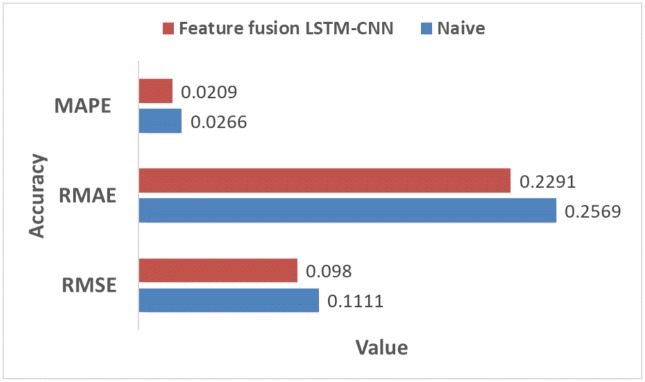

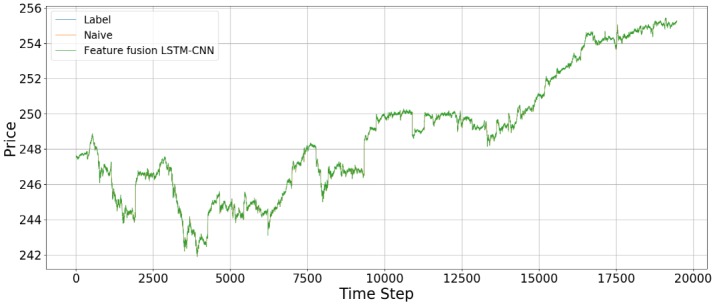

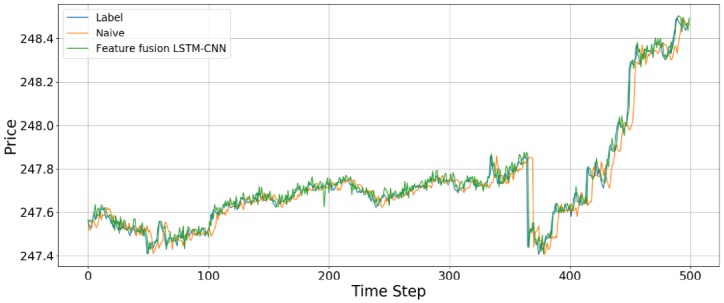

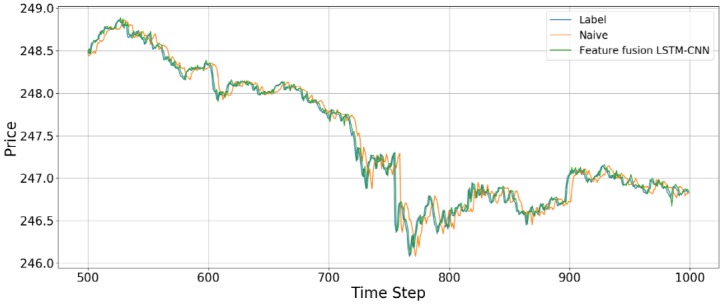

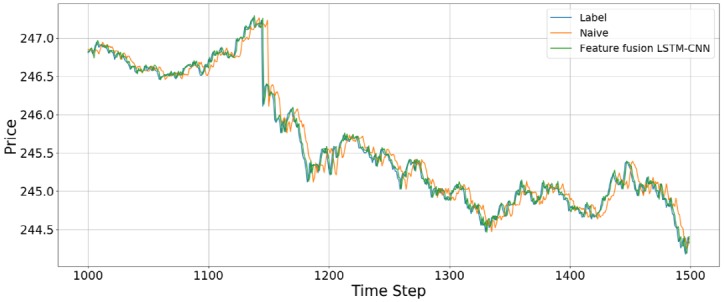

Forecasting stock prices plays an important role in setting a trading strategy or determining the appropriate timing for buying or selling a stock. We propose a model, called the feature fusion long short-term memory-convolutional neural network (LSTM-CNN) model, that combines features learned from different representations of the same data, namely, stock time series and stock chart images, to predict stock prices. The proposed model is composed of LSTM and a CNN, which are utilized for extracting temporal features and image features. We measure the performance of the proposed model relative to those of single models (CNN and LSTM) using SPDR S&P 500 ETF data. Our feature fusion LSTM-CNN model outperforms the single models in predicting stock prices. In addition, we discover that a candlestick chart is the most appropriate stock chart image to use to forecast stock prices. Thus, this study shows that prediction error can be efficiently reduced by using a combination of temporal and image features from the same data rather than using these features separately.

预测股票价格在制定交易策略或确定买卖股票的适当时机方面起着重要作用。我们提出了一种模型,称为特征融合长短时记忆卷积神经网络(LSTM-CNN)模型,该模型结合了从同一数据的不同表示形式(即股票时间序列和股票图表图像)中学到的特征,以预测股票价格。所提出的模型由 LSTM 和 CNN 组成,用于提取时间特征和图像特征。我们使用 SPDR S&P 500 ETF 数据相对于单个模型(CNN 和 LSTM)来衡量所提出模型的性能。我们的特征融合 LSTM-CNN 模型在预测股票价格方面优于单个模型。此外,我们发现蜡烛图是最适合用于预测股票价格的股票图表图像。因此,本研究表明,通过使用同一数据的时间和图像特征的组合而不是分别使用这些特征,可以有效地降低预测误差。