Indiana University Bloomington, USA.

University of Pittsburgh, PA, USA.

Inquiry. 2020 Jan-Dec;57:46958020933765. doi: 10.1177/0046958020933765.

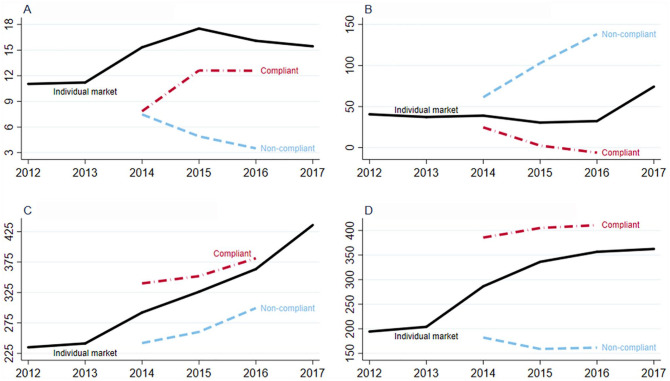

One of the Affordable Care Act's (ACA) signature reforms was creating centralized Health Insurance Marketplaces to offer comprehensive coverage in the form of comprehensive insurance complying with the ACA's coverage standards. Yet, even after the ACA's implementation, millions of people were covered through noncompliant plans, primarily in the form of continued enrollment in "grandmothered" and "grandfathered" plans that predated ACA's full implementation and were allowed under federal and state regulations. Newly proposed and enacted federal legislation may grow the noncompliant segment in future years, and the employment losses of 2020 may grow reliance on individual market coverage further. These factors make it important to understand how the noncompliant segment affects the compliant segment, including the Marketplaces. We show, first, that the noncompliant segment of the individual insurance market substantially outperformed the compliant segment, charging lower premiums but with vastly lower costs, suggesting that insurers have a strong incentive to enter the noncompliant segment. We show, next, that state's decisions to allow grandmothered plans is associated with stronger financial performance of the noncompliant market, but weaker performance of the compliant segment, as noncompliant plans attract lower-cost enrollees. This finding indicates important linkages between the noncompliant and compliant segments and highlights the role state policy can play in the individual insurance market. Taken together, our results point to substantial cream-skimming, with noncompliant plans enrolling the healthiest enrollees, resulting in higher average claims cost in the compliant segment.

《平价医疗法案》(ACA)的一项标志性改革措施是创建集中的医疗保险市场,以综合保险的形式提供全面覆盖,符合 ACA 的覆盖标准。然而,即使在 ACA 实施之后,仍有数百万人通过不符合规定的计划获得了保障,主要是以继续参加“祖母”和“祖父”计划的形式,这些计划在 ACA 全面实施之前就已经存在,并得到了联邦和州法规的允许。新提出并颁布的联邦立法可能会在未来几年增加不符合规定的部分,而 2020 年的就业损失可能会进一步增加对个人市场覆盖的依赖。这些因素使得了解不符合规定的部分如何影响符合规定的部分,包括市场,变得非常重要。我们首先表明,个人保险市场的不符合规定部分表现明显优于符合规定部分,收取较低的保费,但成本却大大降低,这表明保险公司有强烈的动机进入不符合规定部分。接下来,我们表明,允许“祖母”计划的州的决策与不符合规定市场的财务表现较强以及符合规定部分的表现较弱有关,因为不符合规定的计划吸引了低成本的参保者。这一发现表明了不符合规定和符合规定部分之间的重要联系,并强调了州政策在个人保险市场中可以发挥的作用。总之,我们的研究结果表明,不符合规定的计划吸引了最健康的参保者,导致符合规定部分的平均索赔成本更高,存在大量的优质客户筛选现象。