Department of Applied Economics-ECOBAS, University of Vigo, Vigo, Galicia, Spain.

National research University Higher School of Economics, Perm, Russia.

PLoS One. 2021 May 3;16(5):e0249989. doi: 10.1371/journal.pone.0249989. eCollection 2021.

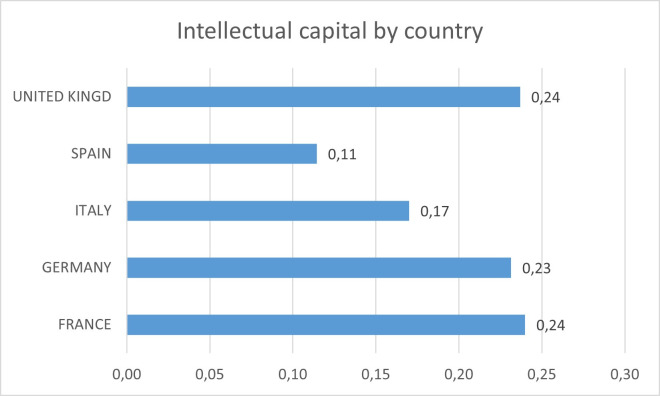

Intellectual capital is defined as the set of intangible assets that generate value for the company. Normally, the models that measure the intellectual capital make use of investments in intangible assets, as indicators of the generation of value by the company; or are based on a holistic measure, using another focus to validate. This research proposes a new method to measure intellectual capital, reconciling the use of financial measures for the management of intellectual capital and its antecedents in triangulated indices; it also determines relationship path coefficients, between constructs developed from a general conceptual model, based on the academic and professional literature. The proposed method combines component indicators with holistic indicators using a structural equation model, allowing differentiating the components of intellectual capital from the stock of intellectual capital. The method is applied to more than 1,600 European companies from 2004 to 2015 to assess its validity, presenting the monetary value of intellectual capital in these companies. The results allow a comparison of the situation of intellectual capital in companies in different countries and industries, opening an opportunity to disclosure intellectual capital.

智力资本被定义为为公司创造价值的无形资产集合。通常,衡量智力资本的模型利用无形资产投资作为公司创造价值的指标;或者基于整体衡量标准,使用另一个焦点来验证。本研究提出了一种新的智力资本衡量方法,协调使用财务措施来管理智力资本及其在三角指标中的前因;它还确定了关系路径系数,这些系数是基于学术和专业文献从一般概念模型中开发的结构构建的。所提出的方法使用结构方程模型将组成指标与整体指标相结合,允许从智力资本的存量中区分智力资本的组成部分。该方法应用于 2004 年至 2015 年来自欧洲的 1600 多家公司,以评估其有效性,并展示这些公司的智力资本的货币价值。结果允许比较不同国家和行业的公司的智力资本状况,为披露智力资本提供了机会。