Department of Sociology, School of Public Administration, Guangzhou University, Guangzhou, 510006, China.

Sci Rep. 2021 Sep 21;11(1):18759. doi: 10.1038/s41598-021-98361-6.

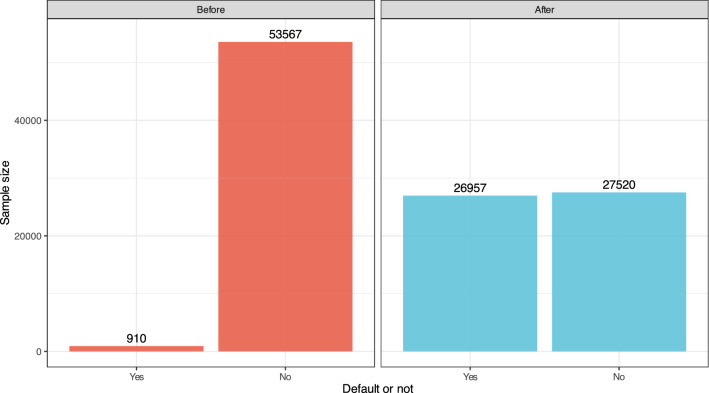

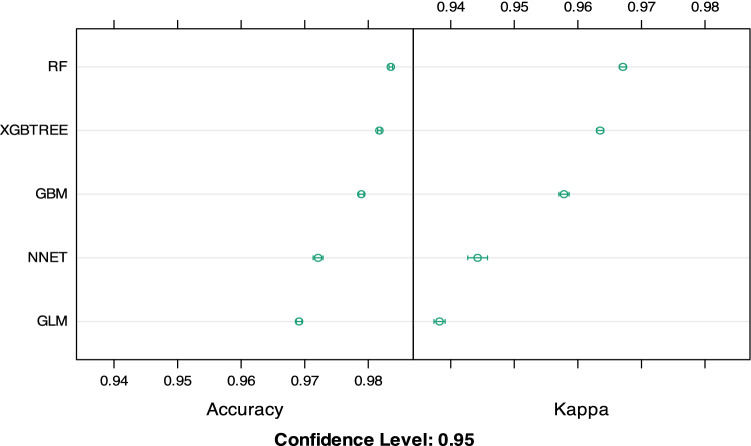

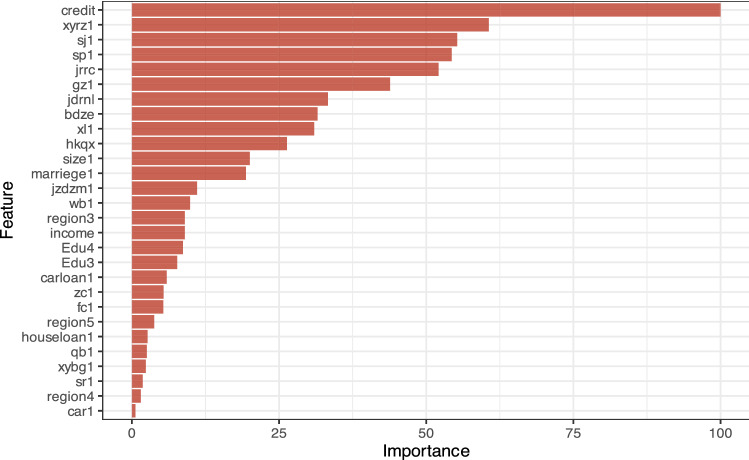

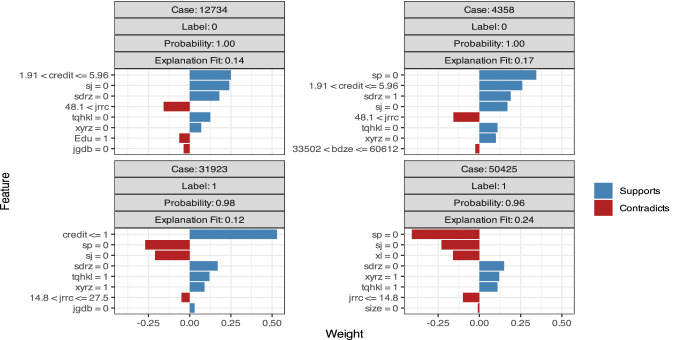

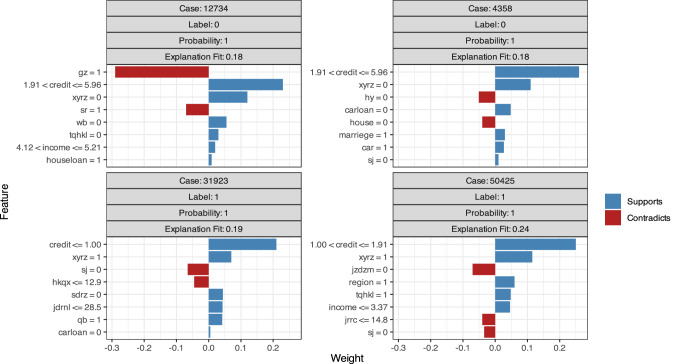

Repayment failures of borrowers have greatly affected the sustainable development of the peer-to-peer (P2P) lending industry. The latest literature reveals that existing risk evaluation systems may ignore important signals and risk factors affecting P2P repayment. In our study, we applied four machine learning methods (random forest (RF), extreme gradient boosting tree (XGBT), gradient boosting model (GBM), and neural network (NN)) to predict important factors affecting repayment by utilizing data from Renrendai.com in China from Thursday, January 1, 2015, to Tuesday, June 30, 2015. The results showed that borrowers who have passed video, mobile phone, job, residence or education level verification are more likely to default on loan repayment, whereas those who have passed identity and asset certification are less likely to default on loans. The accuracy and kappa value of the four methods all exceed 90%, and RF is superior to the other classification models. Our findings demonstrate important techniques for borrower screening by P2P companies and risk regulation by regulatory agencies. Our methodology and findings will help regulators, banks and creditors combat current financial disasters caused by the coronavirus disease 2019 (COVID-19) pandemic by addressing various financial risks and translating credit scoring improvements.

借款人的还款违约极大地影响了点对点 (P2P) 借贷行业的可持续发展。最新文献表明,现有的风险评估系统可能忽略了影响 P2P 还款的重要信号和风险因素。在我们的研究中,我们应用了四种机器学习方法(随机森林 (RF)、极端梯度提升树 (XGBT)、梯度提升模型 (GBM) 和神经网络 (NN)),利用中国人人贷网 2015 年 1 月 1 日星期四至 2015 年 6 月 30 日星期二的数据来预测影响还款的重要因素。结果表明,通过视频、手机、工作、居住或教育水平验证的借款人更有可能拖欠贷款还款,而通过身份和资产认证的借款人则不太可能拖欠贷款。四种方法的准确性和 Kappa 值均超过 90%,且 RF 优于其他分类模型。我们的研究结果为 P2P 公司进行借款人筛选和监管机构进行风险监管提供了重要技术。我们的方法和研究结果将有助于监管机构、银行和债权人应对由 2019 冠状病毒病 (COVID-19) 大流行引起的当前金融危机,解决各种金融风险并提高信用评分。