Yi Xing, Bai Caiquan, Lyu Siyuan, Dai Lu

The Center for Economic Research, Shandong University, Ji'nan, Shandong 250100, PR China.

Department of Economics, Stony Brook University, Stony Brook, NY 11794, USA.

Financ Res Lett. 2021 Oct;42:101948. doi: 10.1016/j.frl.2021.101948. Epub 2021 Jan 26.

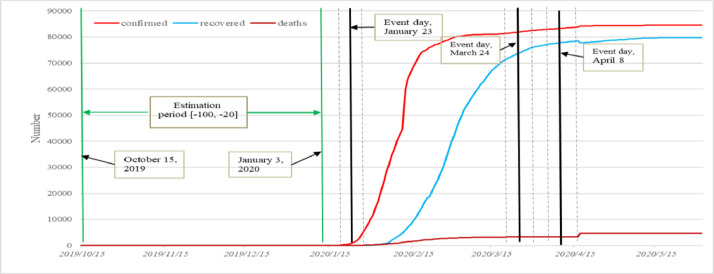

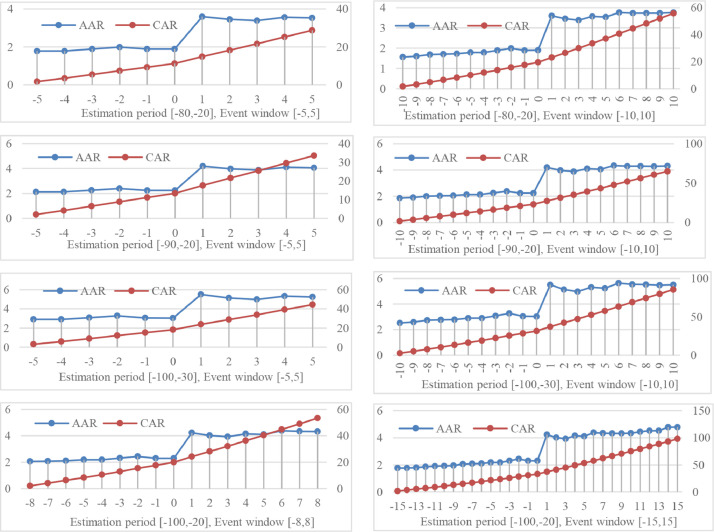

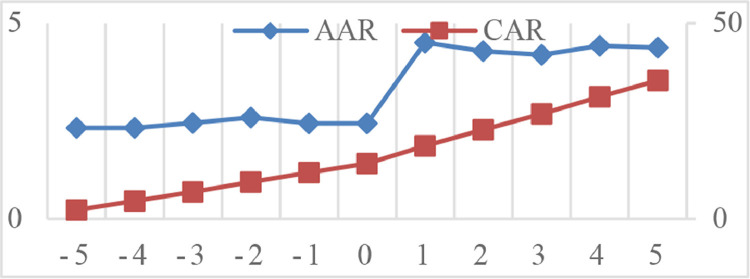

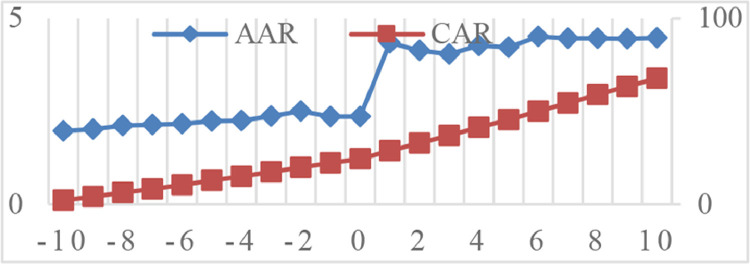

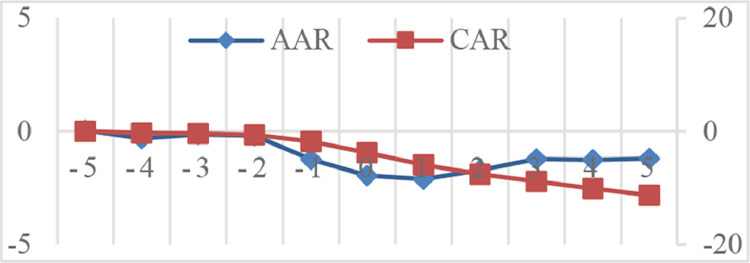

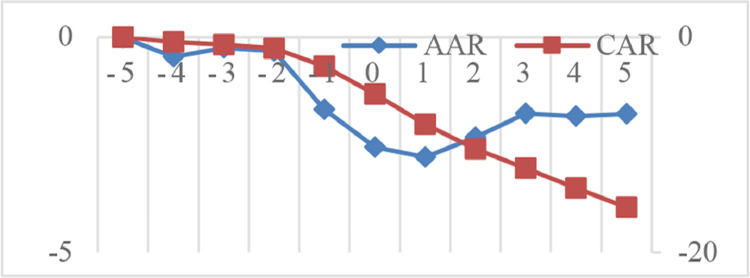

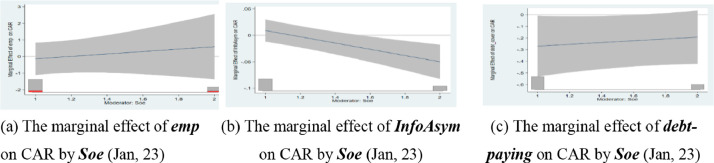

The paper applies the event study method and econometric models to investigate the impacts of COVID-19 on China's green bond market for the first time. We find that (1) the COVID-19 pandemic has significant impacts on China's green bond market and increases the cumulative abnormal return (CAR) of the green bonds greatly. After the pandemic is relieved, the CAR drops significantly; (2) the improving of bond issuers' governance capacity, the weakening of information asymmetry and the reinforcing of debt-paying ability can effectively mitigate the negative impacts and positively promote the recovery of bond issuers after the pandemic; (3) the impacts of bond issuers' governance capacity, information asymmetry and debt-paying ability on the CAR of green bonds are significantly heterogeneous before and after the pandemic due to their property rights and whether they are listed or not.

本文首次运用事件研究法和计量经济模型来考察新冠疫情对中国绿色债券市场的影响。我们发现:(1)新冠疫情对中国绿色债券市场有显著影响,大幅提高了绿色债券的累计超额收益率(CAR)。疫情缓解后,CAR显著下降;(2)债券发行人治理能力的提升、信息不对称的减弱以及偿债能力的增强能够有效减轻负面影响,并在疫情后对债券发行人的复苏起到积极的促进作用;(3)由于债券发行人的产权性质以及是否上市,其治理能力、信息不对称和偿债能力对绿色债券CAR的影响在疫情前后存在显著的异质性。