Chai Shanglei, Chu Wenjun, Zhang Zhen, Li Zhilong, Abedin Mohammad Zoynul

Business School, Shandong Normal University, Jinan, 250014 China.

School of Economics and Management, China University of Petroleum, 66 West Changjiang Road, Huangdao District, Qingdao, 266555 China.

Ann Oper Res. 2022 Jan 6:1-28. doi: 10.1007/s10479-021-04452-y.

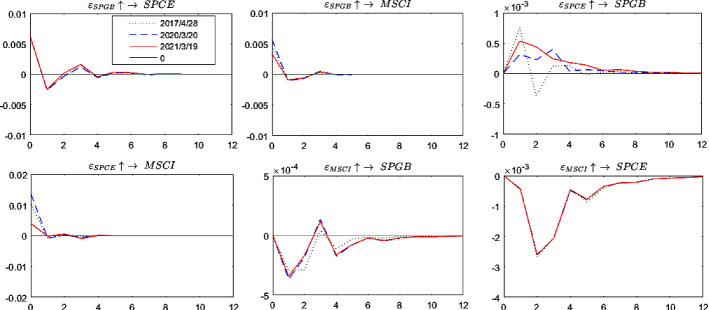

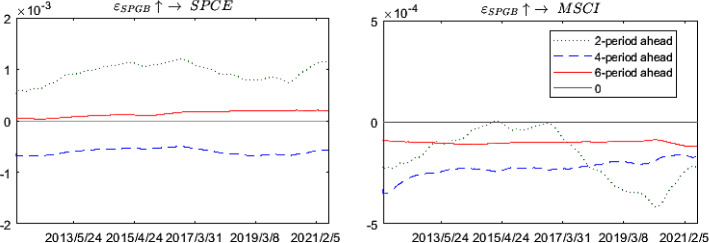

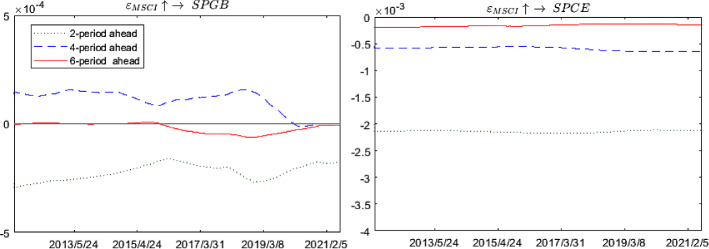

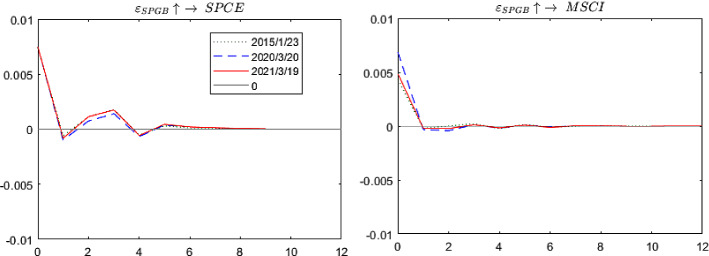

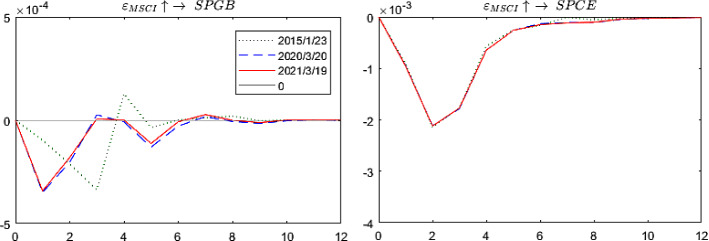

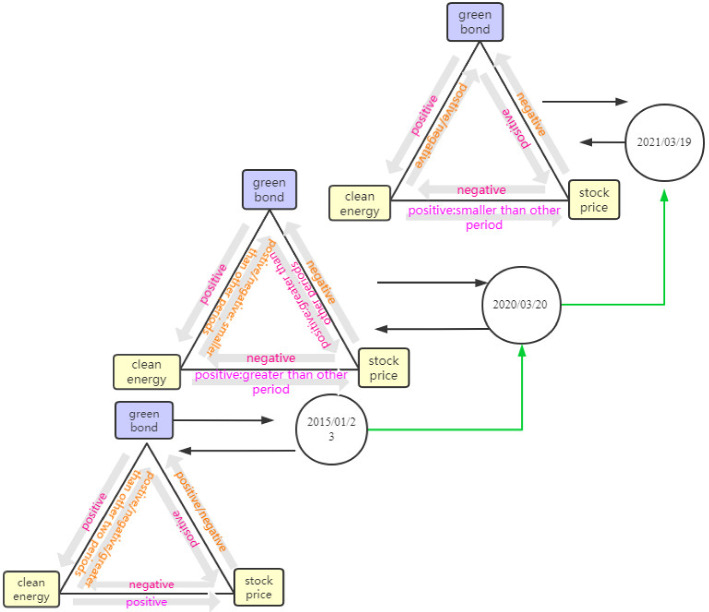

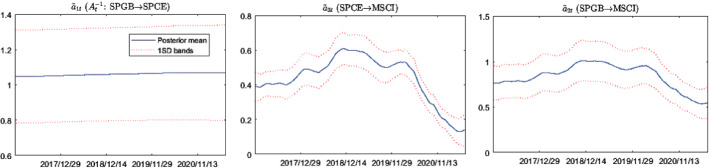

This paper uses weekly data from July 01, 2011 to July 09, 2021 to examine the dynamic nonlinear connectedness between the green bonds, clean energy, and stock price around the COVID-19 outbreak in the global markets. By building a time-varying parameter vector autoregression model (TVP-VAR), the comparison analyses of pre- and during the COVID-19 sample groups verify the existence of nonlinear and dynamic correlation among the three variables. First, prior to the COVID-19 pandemic, the simultaneous impacts of clean energy on stock price increased over time. Second, the results of impulse responses at different horizons indicate that green bonds lead to a short-term increase of clean energy, and it exerts an increasingly positive impacts after the COVID-19 outbreak. The COVID-19 has weakened the negative impacts of green bonds on stock price in the medium term. Finally, through the analysis of impulse responses at different points, we find that stock prices will rise when clean energy is subjected to a positive shock, and this positive effect is stronger during economic recovery period than in the other two periods.

本文使用2011年7月1日至2021年7月9日的周数据,研究全球市场中新冠疫情爆发前后绿色债券、清洁能源和股票价格之间的动态非线性关联。通过构建时变参数向量自回归模型(TVP-VAR),对新冠疫情样本组前后的比较分析验证了这三个变量之间存在非线性和动态相关性。首先,在新冠疫情大流行之前,清洁能源对股票价格的同步影响随时间增加。其次,不同滞后期的脉冲响应结果表明,绿色债券导致清洁能源短期增加,并且在新冠疫情爆发后其产生的积极影响越来越大。新冠疫情在中期减弱了绿色债券对股票价格的负面影响。最后,通过对不同时间点脉冲响应的分析,我们发现当清洁能源受到正向冲击时股票价格会上涨,并且这种积极效应在经济复苏期比在其他两个时期更强。