School of Business, Ningbo University, Ningbo, Zhejiang, China.

School of Economics and Management, Northeast Agricultural University, Harbin, Heilongjiang, China.

PLoS One. 2021 Nov 8;16(11):e0259308. doi: 10.1371/journal.pone.0259308. eCollection 2021.

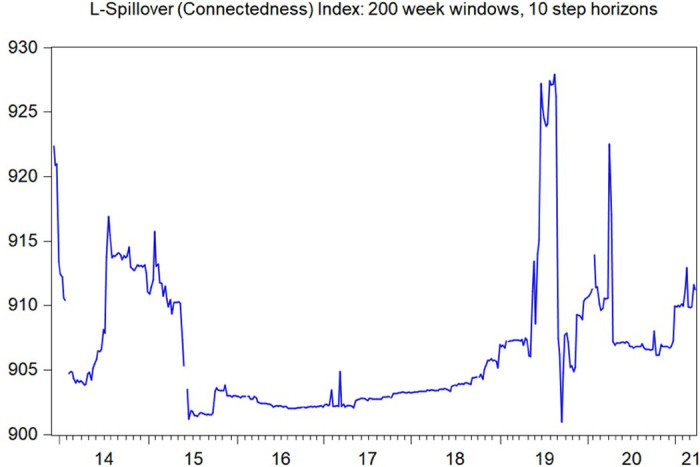

The risk spillover among financial markets has been noticeably investigated in a burgeoning number of literature. Given those doctrines, we scrutinize the impact persistence of volatility spillover and illiquidity spillover of Chinese commodity markets in this paper. Based on the sample from 2010 to 2020, we reveal that there is a cross-market spillover of volatility and illiquidity in China and also, interactions between volatility and illiquidity in different financial markets are pronounced. More importantly, we demonstrate that different commodity markets have different responsiveness to stock market shocks, which embeds their market characteristics. Specifically, we discover that the majority of the traders in gold market might be hedger and therefore gold market is more sensitive to stock market illiquidity shock and thus the shock impact in persistent. On the other hand, agricultural markets like corn and soybean markets might be dominated by investors and thus those markets respond to the stock market volatility shocks and the shock impact in persistent over 10 periods given the first period of risk shock happening. In fact, different Chinese commodity markets' responsiveness towards Chinese stock market risk shocks indicates the stock market risk impact persistence in Chinese commodity markets. This result can help policymakers to understand the policy propagation effect according to this risk spillover channel and risk impact persistence mechanism in China.

金融市场之间的风险溢出已经在大量文献中得到了明显的研究。基于这些理论,我们在本文中考察了中国商品市场波动溢出和流动性溢出的影响持续性。基于 2010 年至 2020 年的样本,我们发现中国存在跨市场的波动和流动性溢出,不同金融市场之间的波动和流动性相互作用显著。更重要的是,我们证明了不同的商品市场对股票市场冲击的反应不同,这反映了它们的市场特征。具体来说,我们发现黄金市场的大多数交易者可能是套期保值者,因此黄金市场对股票市场流动性冲击更为敏感,冲击的持续影响也更为持久。另一方面,像玉米和大豆这样的农产品市场可能由投资者主导,因此这些市场对股票市场波动冲击更为敏感,并且在风险冲击发生后的前 10 个时期内,冲击的持续影响较为持久。事实上,中国不同商品市场对中国股票市场风险冲击的反应表明,股票市场风险在中国商品市场的影响具有持续性。这一结果可以帮助政策制定者根据中国的风险溢出渠道和风险影响持续性机制,了解政策的传播效果。