Banerjee Ameet Kumar

Xavier Institute of Management, Xavier University, Bhubaneswar, Odisha, 751 013, India.

Financ Res Lett. 2021 Nov;43:102018. doi: 10.1016/j.frl.2021.102018. Epub 2021 Mar 13.

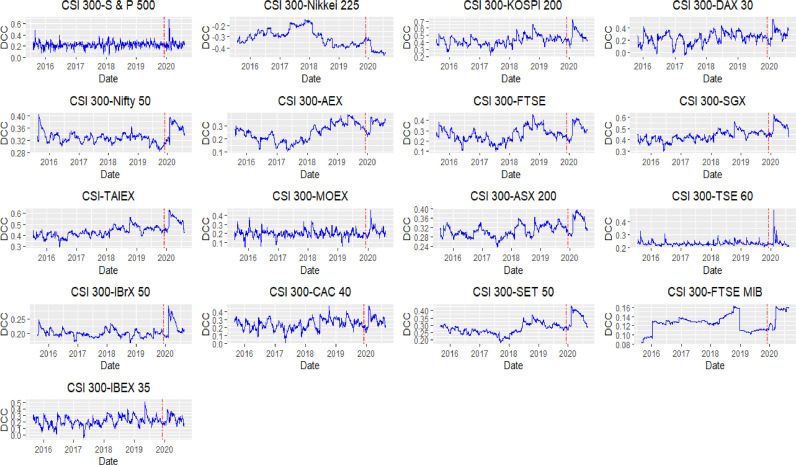

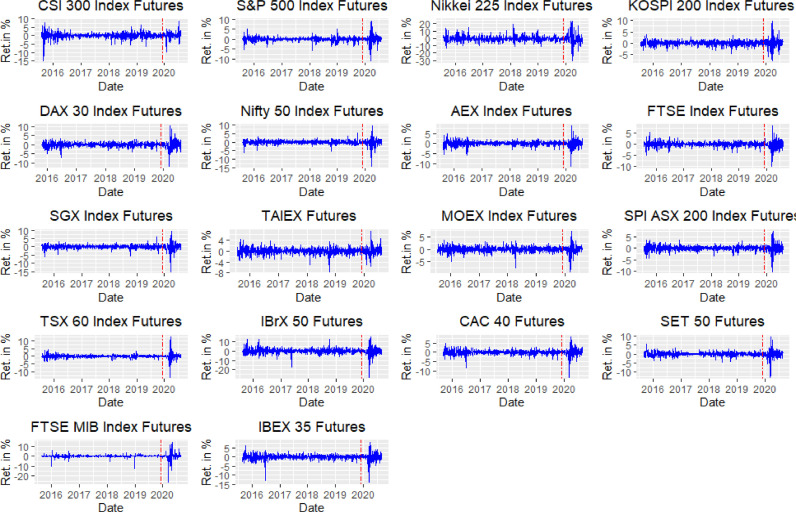

The paper aims to investigate the existence of financial contagion between China and its major trading partners during the ongoing COVID-19 pandemic using the multivariate ADCC-EGARCH model. The analysis results reveal significant financial contagion in most developed and emerging markets having significant trade relationships with China during COVID-19 syndrome. The evidence about financial contagion is vital for regulators and different classes of market participants for varying purposes, and hence the results should find practical implications similar to policymakers, investors, and risk managers.

本文旨在运用多元ADCC-EGARCH模型,研究在当前新冠疫情期间中国与其主要贸易伙伴之间是否存在金融传染。分析结果显示,在新冠疫情期间,与中国有重要贸易关系的大多数发达和新兴市场都存在显著的金融传染。金融传染的证据对监管机构和不同类型的市场参与者出于不同目的而言至关重要,因此这些结果应能为政策制定者、投资者和风险管理者等带来类似的实际影响。