Puertas Antonio M, Trinidad-Segovia Juan E, Sánchez-Granero Miguel A, Clara-Rahora Joaquim, de Las Nieves F Javier

Departamento de Química y Física, Universidad de Almería, 04.120, Almería, Spain.

Departamento de Economía y Empresa, Universidad de Almería, 04.120, Almería, Spain.

Sci Rep. 2021 Nov 29;11(1):23076. doi: 10.1038/s41598-021-02263-6.

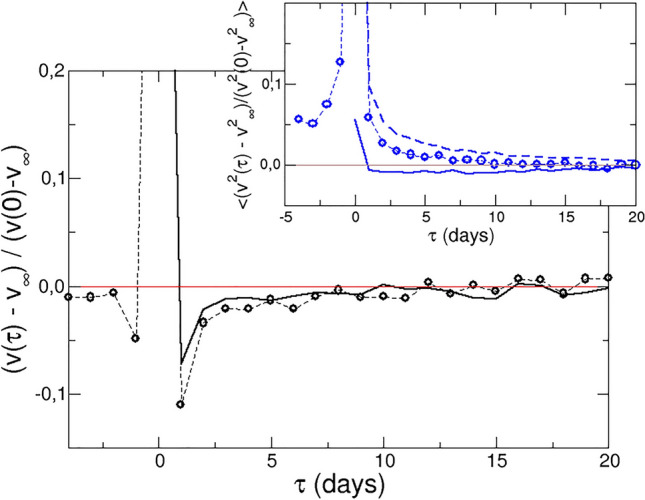

Linear response theory relates the response of a system to a weak external force with its dynamics in equilibrium, subjected to fluctuations. Here, this framework is applied to financial markets; in particular we study the dynamics of a set of stocks from the NASDAQ during the last 20 years. Because unambiguous identification of external forces is not possible, critical events are identified in the series of stock prices as sudden changes, and the stock dynamics following an event is taken as the response to the external force. Linear response theory is applied with the log-return as the conjugate variable of the force, providing predictions for the average response of the price and return, which agree with observations, but fails to describe the volatility because this is expected to be beyond linear response. The identification of the conjugate variable allows us to define the perturbation energy for a system of stocks, and observe its relaxation after an event.

线性响应理论将系统对弱外力的响应与其在平衡状态下受涨落影响的动力学联系起来。在此,该框架被应用于金融市场;具体而言,我们研究了纳斯达克过去20年中一组股票的动态。由于无法明确识别外力,所以在股价序列中将关键事件识别为突然变化,并将事件后的股票动态视为对外力的响应。线性响应理论以对数收益率作为力的共轭变量来应用,给出了价格和收益率平均响应的预测,这些预测与观测结果相符,但未能描述波动率,因为预计波动率超出了线性响应范围。共轭变量的识别使我们能够定义股票系统的扰动能量,并观察事件发生后它的弛豫情况。