Zebende G F, Santos Dias R M T, de Aguiar L C

State University of Feira de Santana, Bahia, Brazil.

Institute Polytechnic of Setúbal, Portugal.

Heliyon. 2022 Jan 24;8(1):e08808. doi: 10.1016/j.heliyon.2022.e08808. eCollection 2022 Jan.

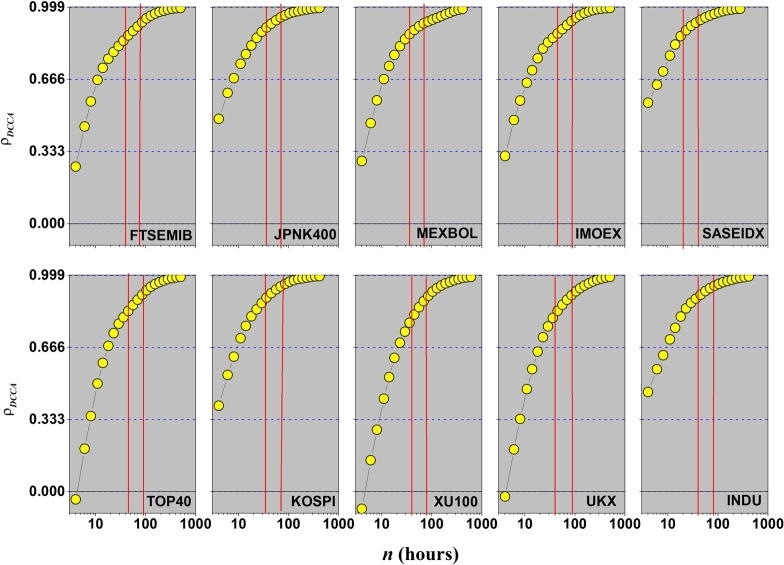

Given the importance of the financial markets in the global context, data analysis and new statistical approach are always welcome, especially if we are referring to G-20 group (the world's richest countries). As we know, the pandemic outbreak of COVID-19 has affected the global economy, and its impact seems to be inevitable (as it was in 2020). From the perspective of what was raised above, this paper aims to analyze the stock market efficiency in 21 indexes of G-20. We are going to do our analysis with intraday scale (of hour), from May 2019 to May 2020. In order to be successful in this analysis, we applied the DFA and the DCCA methods, to identify or not two points:i)Are G-20 stock market efficient in their weak form?ii)With open/close values, it is possible to identify some type of memory in G-20 group? The answer to these points will be given throughout this paper. For this purpose, the entire analysis will be divided into two different time-scale: Period I, time-scale less than five days and Period II, with time-scale greater than ten days. In the pandemic times of COVID-19, our results show that taking into account the DFA method, for time-scale shorter than 5 days, the stock markets tend to be efficient, whereas for time-scale longer than 10 days, the stock market tend to be inefficient. But, with DCCA method for cross-correlation analysis, the results for open/close indexes show different types of behaviors for each stock market index separately.

鉴于金融市场在全球背景下的重要性,数据分析和新的统计方法总是受到欢迎,特别是当我们提及二十国集团(世界上最富有的国家)时。如我们所知,新冠疫情的爆发已经影响了全球经济,而且其影响似乎不可避免(就像2020年那样)。从上述提出的内容来看,本文旨在分析二十国集团21个指数的股票市场效率。我们将在2019年5月至2020年5月期间以小时级的日内规模进行分析。为了在该分析中取得成功,我们应用了去趋势波动分析(DFA)和去趋势交叉相关分析(DCCA)方法,以确定以下两点:

i)二十国集团股票市场在弱式有效方面是否有效?

ii)通过开盘/收盘价,是否有可能在二十国集团中识别出某种类型的记忆?本文将给出这些问题的答案。为此,整个分析将分为两个不同的时间尺度:第一阶段,时间尺度小于五天;第二阶段,时间尺度大于十天。在新冠疫情期间,我们的结果表明,考虑到DFA方法,对于时间尺度短于5天的情况,股票市场倾向于有效,而对于时间尺度长于10天的情况,股票市场倾向于无效。但是,使用DCCA方法进行交叉相关分析时,开盘/收盘指数的结果分别显示了每个股票市场指数的不同行为类型。