Liu Yuntong, Wei Yu, Wang Qian, Liu Yi

School of Finance, Yunnan University of Finance and Economics, Kunming, Yunnan, China.

Faculty of Transportation Engineering, Kunming University of Science and Technology, Kunming, Yunnan, China.

Financ Res Lett. 2022 Mar;45:102145. doi: 10.1016/j.frl.2021.102145. Epub 2021 May 23.

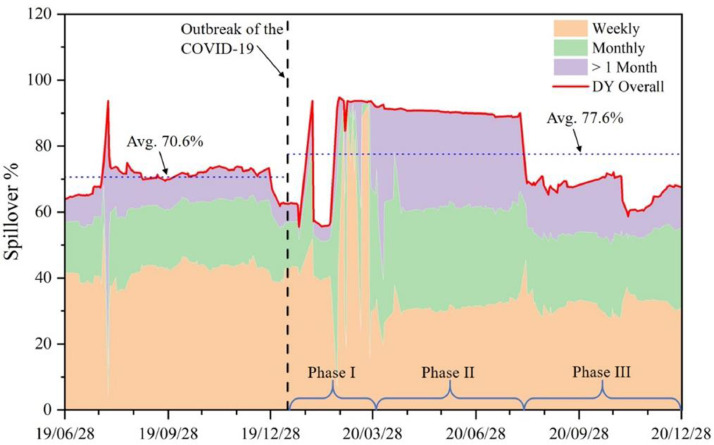

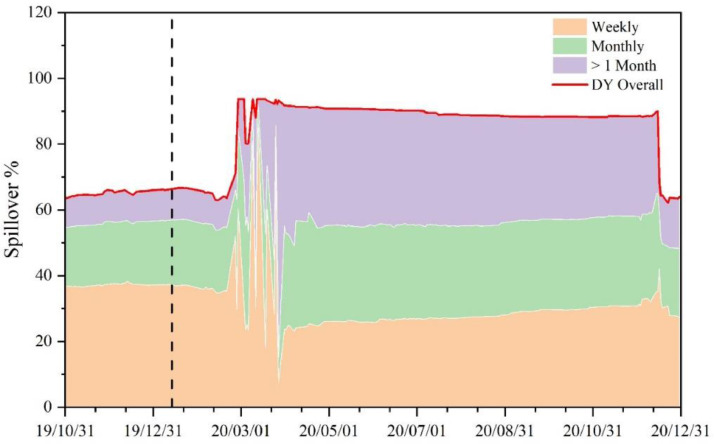

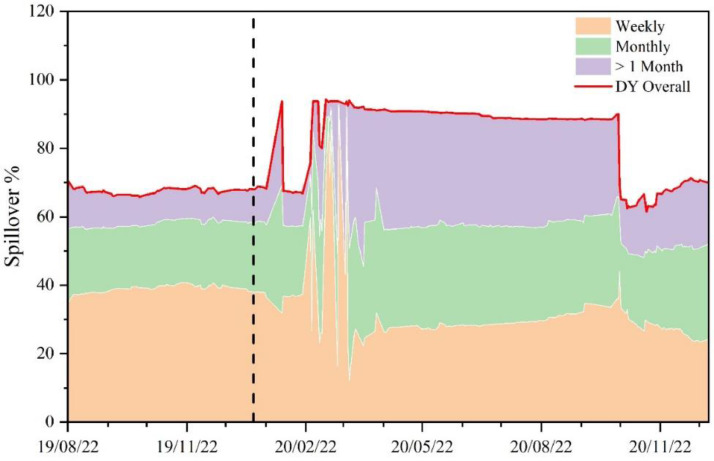

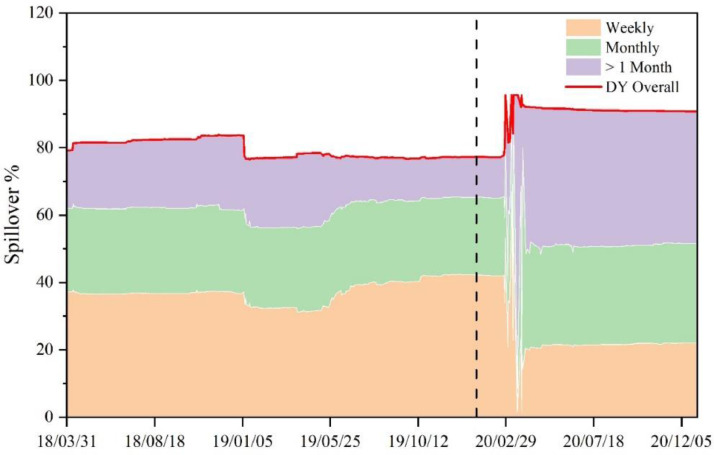

This paper examines the risk contagion among international stock markets during the COVID-19 pandemic by using the realized volatility information from sixteen major stock markets in the world. The empirical evidence based on the connectedness methods of Diebold and Yilmaz (2012) and Baruník and Křehlík (2018) shows that the COVID-19 epidemic significantly increases the risk contagion effects in international stock markets. Besides, the risk spillovers from stock markets in European and American regions increase rapidly but those in Asian markets decrease obviously after the outbreak of COVID-19 pandemic. Finally, the risk contagion among international stock markets caused by the pandemic can last for about 6 to 8 months. These results provide important implications regarding to financial risk management and macroprudential design.

本文通过运用来自全球16个主要股票市场的已实现波动率信息,研究了新冠疫情期间国际股票市场之间的风险传染情况。基于迪博尔德和伊尔马兹(2012年)以及巴鲁尼克和克雷利克(2018年)的连通性方法的实证证据表明,新冠疫情显著增强了国际股票市场中的风险传染效应。此外,新冠疫情爆发后,欧美地区股票市场的风险溢出迅速增加,而亚洲市场的风险溢出则明显减少。最后,疫情引发的国际股票市场间的风险传染可持续约6至8个月。这些结果为金融风险管理和宏观审慎设计提供了重要启示。