Fassas Athanasios P

Department of Accounting and Finance, University of Thessaly, Geopolis Campus, 41500, Larissa, Greece.

Heliyon. 2020 Dec 13;6(12):e05715. doi: 10.1016/j.heliyon.2020.e05715. eCollection 2020 Dec.

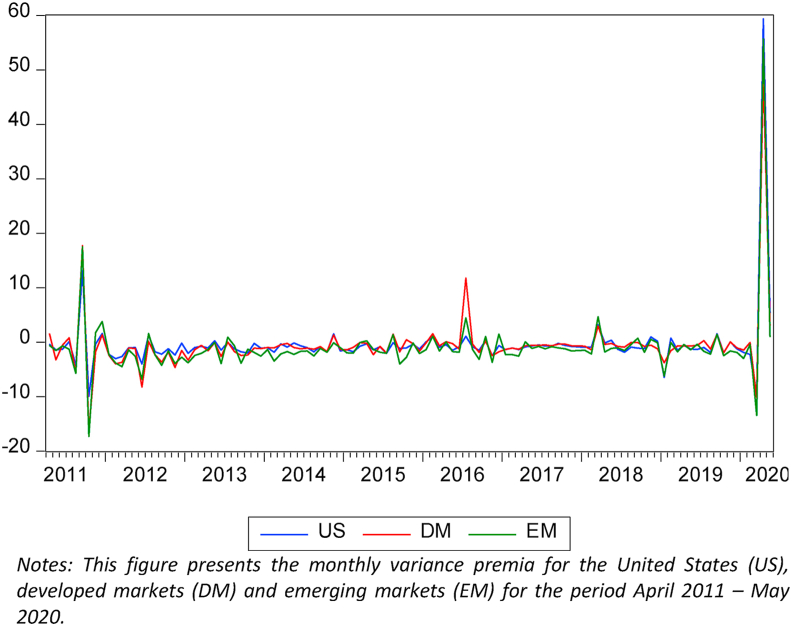

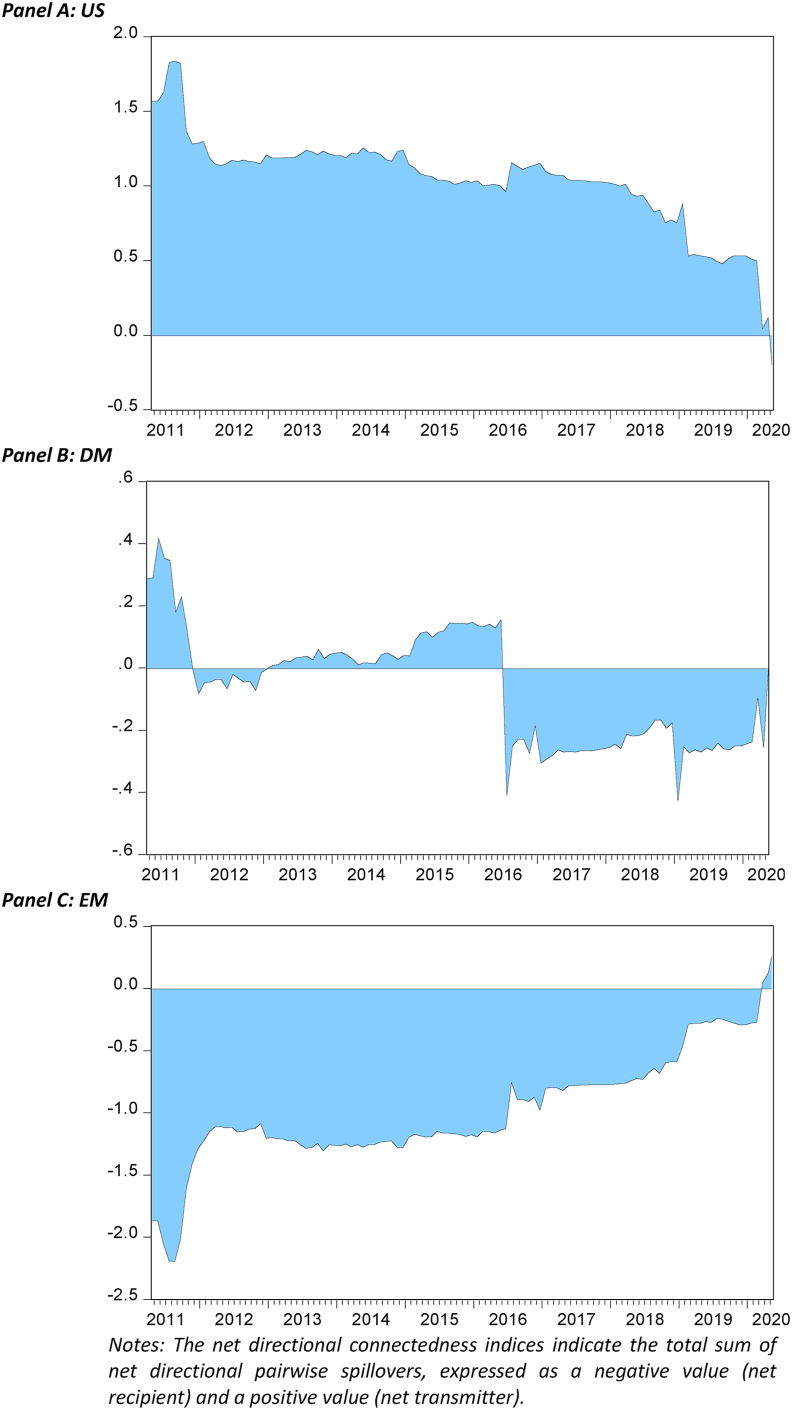

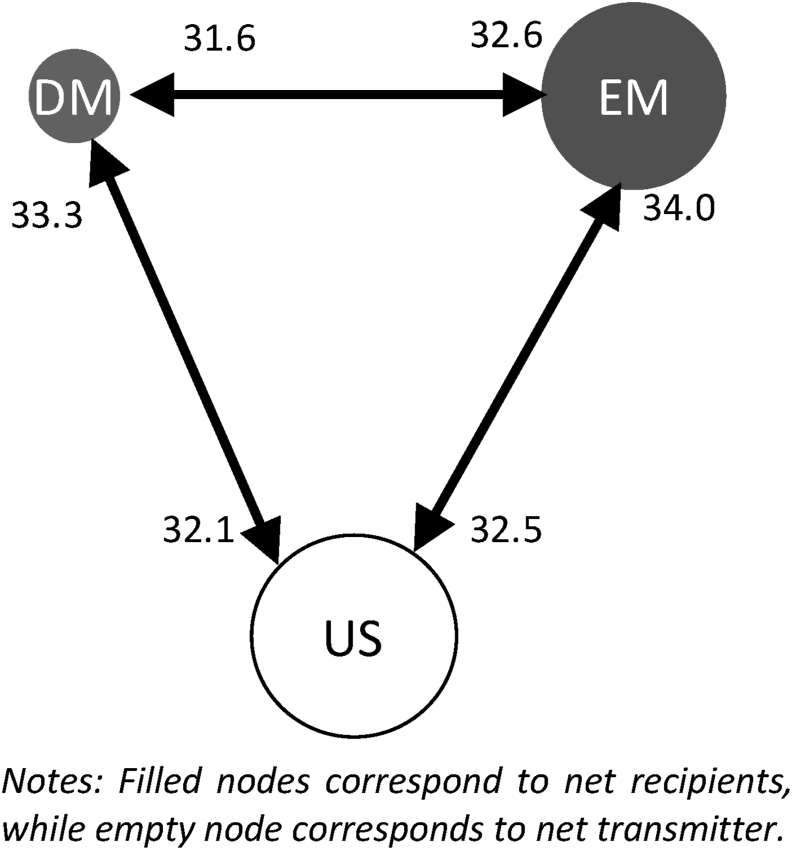

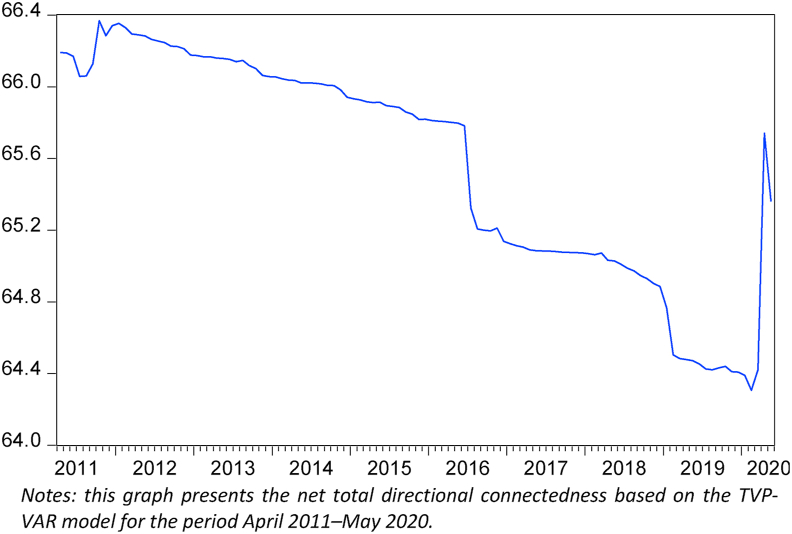

This study investigates the dynamic connectedness across the variance risk premium in international developed and emerging equity markets based on a Bayesian time-varying parameter vector autoregressive methodology. The empirical results indicate that the total spillover index is on average 65.6%, indicating a high, albeit declining, level of interconnectedness across the investor sentiment in the three markets under review until early 2020. Following the COVID-19 outbreak though, the total investors' risk aversion connectedness - as expected - strengthens, but more importantly, its dynamics alter, indicating that the risk aversion of emerging markets is an important contributor to the connectedness of international markets.

本研究基于贝叶斯时变参数向量自回归方法,考察国际发达和新兴股票市场方差风险溢价之间的动态关联性。实证结果表明,总溢出指数平均为65.6%,这表明在2020年初之前,所考察的三个市场的投资者情绪之间存在高度的关联性,尽管这种关联性在下降。然而,在新冠疫情爆发后,投资者的总体风险厌恶关联性——正如预期的那样——增强了,但更重要的是,其动态发生了变化,这表明新兴市场的风险厌恶是国际市场关联性的一个重要因素。