Văn Lê, Bảo Nguyễn Khắc Quốc

UEH College of Technology and Design, University of Economics Ho Chi Minh City (UEH University), 59C Nguyen Dinh Chieu Street, Ward 6, District 3, Ho Chi Minh City, Viet Nam.

School of Finance, UEH College of Business, University of Economics Ho Chi Minh City (UEH University), 59C Nguyen Dinh Chieu Street, Ward 6, District 3, Ho Chi Minh City, Viet Nam.

Resour Policy. 2022 Aug;77:102634. doi: 10.1016/j.resourpol.2022.102634. Epub 2022 Mar 14.

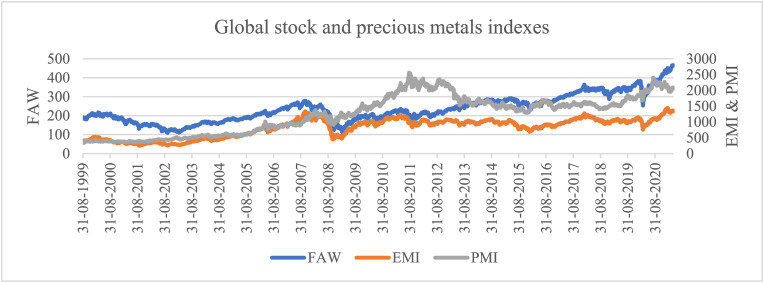

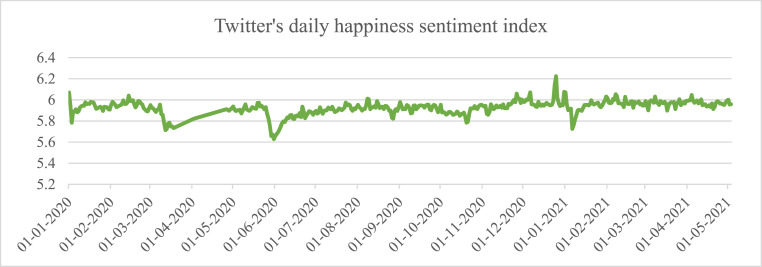

In this paper, we examine the relationship between global stock markets, as respectively represented by the FTSE All-World Series and the MSCI Emerging Markets indexes, and the S&P GSCI Precious Metals index from 01 September 1999 to 03 May 2021. We employ the conditional correlation multivariate generalized autoregressive conditional heteroskedasticity (MGARCH) to investigate this stock-precious metals nexus in terms of return and volatility spillovers. The study assesses impacts of the Covid-19 pandemic on the stock-precious metals nexus and further examine this relationship by supplementing the Twitter's Daily Happiness Sentiment index to the methodological framework for the period from 01 January 2020 to 03 May 2021. We find that precious metals positively influence stock markets before the Covid-19 outbreak and firmly play a valuable role due to their hedge and safe haven characteristics. In contrast, the bivariate GARCH framework does not provide statistically significant evidence on the stock-precious metals nexus during the Covid-19 pandemic. Meanwhile, the tri-variate GARCH approach with stock markets, precious metals, and happiness sentiment indexes reveals sufficiently complicated interactions between these return series. Prominently, past change in the happiness index negatively affects the stock returns but positively drives the performance of precious metals. These findings indirectly demonstrate the stock-precious metals nexus under impacts of the Covid-19 pandemic and reflect the demand of precious metals during crisis periods. Accordingly, we suggest a reasonable method of adjusting the proxies when no interaction effect is significantly found during unprecedented outbreaks.

在本文中,我们考察了1999年9月1日至2021年5月3日期间,分别由富时全球全市场指数系列和摩根士丹利资本国际新兴市场指数所代表的全球股票市场,与标准普尔高盛商品指数贵金属指数之间的关系。我们采用条件相关多元广义自回归条件异方差模型(MGARCH),从回报和波动溢出的角度研究这种股票与贵金属的关系。该研究评估了新冠疫情对股票与贵金属关系的影响,并在2020年1月1日至2021年5月3日期间,通过将推特每日幸福情绪指数纳入方法论框架,进一步考察了这种关系。我们发现,在新冠疫情爆发前,贵金属对股票市场有积极影响,并且由于其避险和避风港特性,确实发挥了重要作用。相比之下,二元GARCH框架并未为新冠疫情期间股票与贵金属的关系提供具有统计学意义的证据。同时,包含股票市场、贵金属和幸福情绪指数的三元GARCH方法揭示了这些回报序列之间足够复杂的相互作用。显著的是,幸福指数的过去变化对股票回报有负面影响,但对贵金属的表现有积极推动作用。这些发现间接证明了新冠疫情影响下的股票与贵金属关系,并反映了危机时期对贵金属的需求。因此,我们建议在前所未有的疫情爆发期间,当未发现显著的相互作用效应时,采用一种合理的代理调整方法。