Li Qian, Zhang Wei

School of Mathematics, Physics and Statistics, Shanghai University of Engineering Science, Shanghai, 201620 China.

School of Mathematics, South China University of Technology, Guangzhou, 510640 China.

Optim Lett. 2023;17(5):1181-1200. doi: 10.1007/s11590-022-01914-5. Epub 2022 Jul 31.

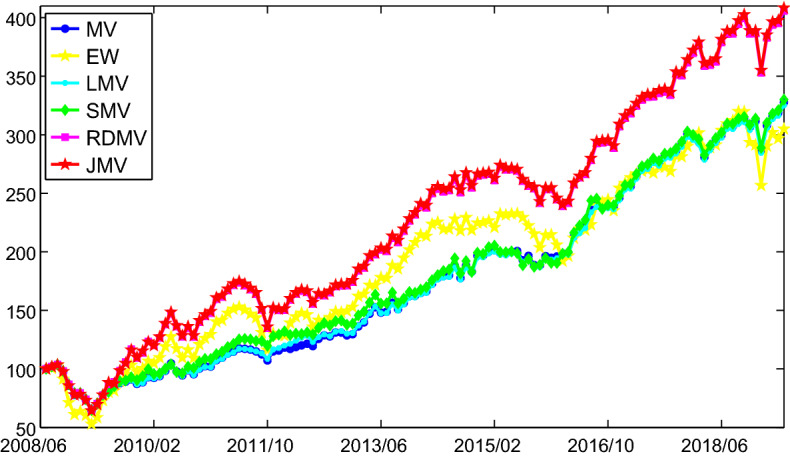

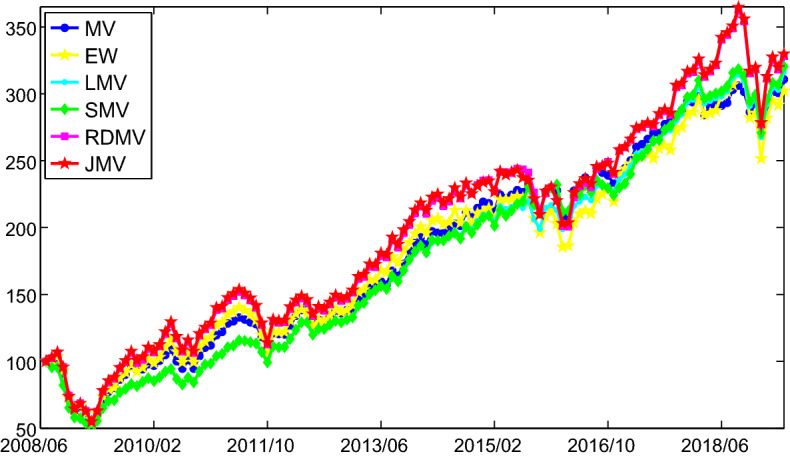

Portfolio risk management has become more important since some unpredictable factors, such as the 2008 financial crisis and the recent COVID-19 crisis. Although the risk can be actively managed by risk diversification, the high transaction cost and managerial concerns ensue by over diversifying portfolio risk. In this paper, we jointly integrate risk diversification and sparse asset selection into mean-variance portfolio framework, and propose an optimal portfolio selection model labeled as JMV. The weighted piecewise quadratic approximation is considered as a penalty promoting sparsity for the asset selection. The variance associated with the marginal risk regard as another penalty term to diversify the risk. By exposing the feature of JMV, we prove that the KKT point of JMV is the local minimizer if the regularization parameter satisfies a mild condition. To solve this model, we introduce the accelerated proximal gradient (APG) algorithm [Wen in SIAM J. Optim 27:124-145, 2017], which is one of the most efficient first-order large-scale algorithm. Meanwhile, the APG algorithm is linearly convergent to a local minimizer of the JMV model. Furthermore, empirical analysis consistently demonstrate the theoretical results and the superiority of the JMV model.

自2008年金融危机和近期的新冠疫情等一些不可预测因素出现以来,投资组合风险管理变得愈发重要。尽管风险可以通过风险分散来积极管理,但过度分散投资组合风险会带来高昂的交易成本和管理问题。在本文中,我们将风险分散和稀疏资产选择共同纳入均值-方差投资组合框架,并提出了一个名为JMV的最优投资组合选择模型。加权分段二次逼近被视为促进资产选择稀疏性的一种惩罚。与边际风险相关的方差被视为另一个用于分散风险的惩罚项。通过揭示JMV的特性,我们证明如果正则化参数满足一个温和条件,JMV的KKT点就是局部极小值点。为求解该模型,我们引入了加速近端梯度(APG)算法[Wen于《SIAM优化杂志》2017年第27卷:124 - 145页],它是最有效的一阶大规模算法之一。同时,APG算法线性收敛于JMV模型的一个局部极小值点。此外,实证分析一致证明了理论结果以及JMV模型的优越性。