School of Sciences, Changzhou Institute of Technology, Changzhou 213000, China.

Comput Intell Neurosci. 2022 Jul 15;2022:5246309. doi: 10.1155/2022/5246309. eCollection 2022.

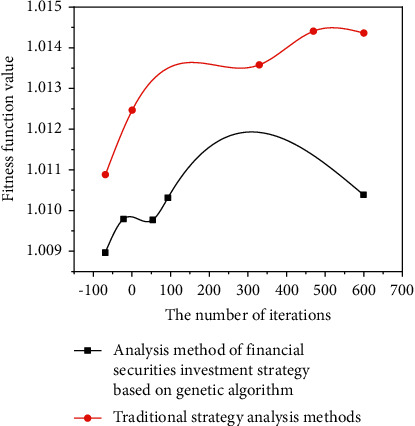

In order to address the application of genetic optimization algorithms to financial investment portfolio issues, the optimal allocation rate must be high and the risk is low. This paper uses quadratic programming algorithms and genetic algorithms as well as quadratic programming algorithms, Matlab planning solutions for genetic algorithms, and genetic algorithm toolboxes to solve Markowitz's mean variance model. The mathematical model for introducing sparse portfolio strategies uses the decomposition method of penalty functions as an algorithm for solving nonconvex sparse optimization strategies to solve financial portfolio problems. The merging speed of the quadratic programming algorithm is fast, and the merging speed depends on the selection of the initial value. The genetic algorithm performs very well in global searches, but local search capabilities are insufficient and the pace of integration into the next stage is slow. To solve this, using a genetic algorithm toolbox is quick and easy. The results of the experiments show that the final solution of the decomposition method of the fine function is consistent with the solution of the integrity of the genetic algorithm. 67% of the total funds will be spent on local car reserves and 33% on wine reserves. When data scales are small, quadratic programming algorithms and genetic algorithms can provide effective portfolio feedback, and the method of breaking down penalty functions to ensure the reliability and effectiveness of algorithm combinations is widely used in sparse financial portfolio issues.

为了解决遗传优化算法在金融投资组合问题中的应用,必须实现高的最优配置率和低风险。本文使用二次规划算法和遗传算法以及二次规划算法、Matlab 规划遗传算法的解决方案,以及遗传算法工具箱来解决 Markowitz 的均值方差模型。引入稀疏投资组合策略的数学模型使用罚函数的分解方法作为求解非凸稀疏优化策略的算法来解决金融投资组合问题。二次规划算法的合并速度很快,合并速度取决于初始值的选择。遗传算法在全局搜索中表现出色,但局部搜索能力不足,下一阶段的整合速度较慢。为了解决这个问题,可以使用遗传算法工具箱来快速简便地解决。实验结果表明,精细函数分解方法的最终解与遗传算法的整体解一致。67%的总资金将用于当地汽车储备,33%用于葡萄酒储备。当数据规模较小时,二次规划算法和遗传算法可以提供有效的投资组合反馈,而分解罚函数的方法则可以确保算法组合的可靠性和有效性,这种方法在稀疏金融投资组合问题中得到了广泛应用。