Kanamura Takashi

Graduate School of Advanced Integrated Studies in Human Survivability (GSAIS), Kyoto University, 1, Yoshida-Nakaadachi-cho, Sakyo-ku, Kyoto, 606-8306 Japan.

Environ Dev Sustain. 2022 Aug 3:1-41. doi: 10.1007/s10668-022-02460-x.

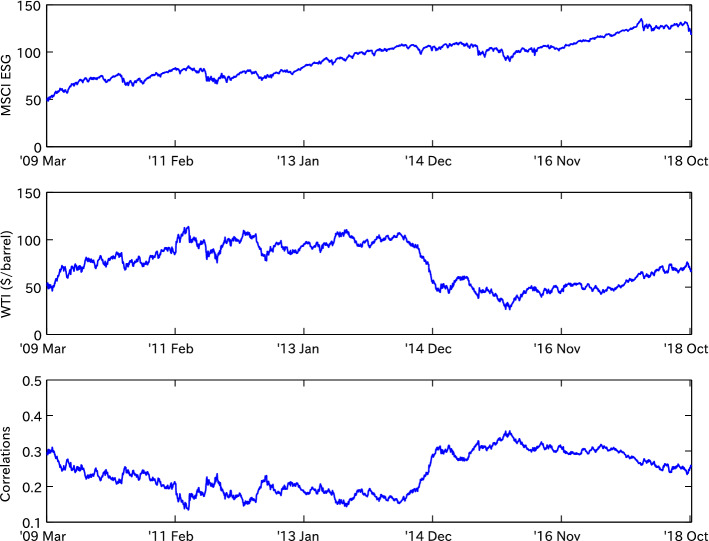

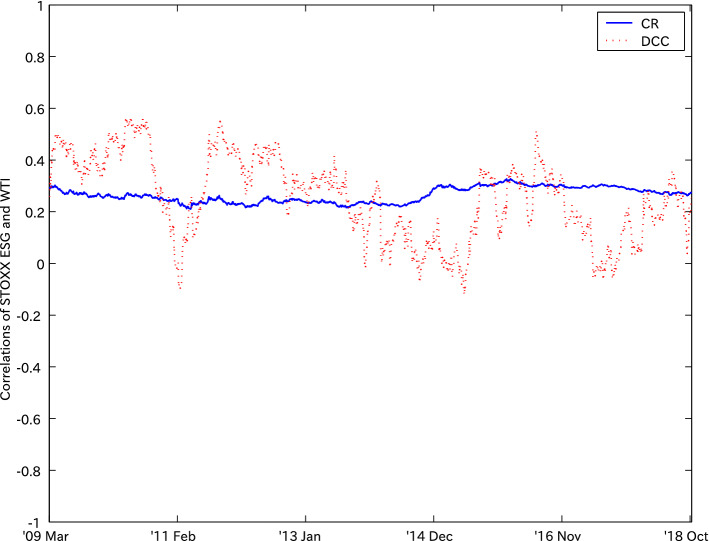

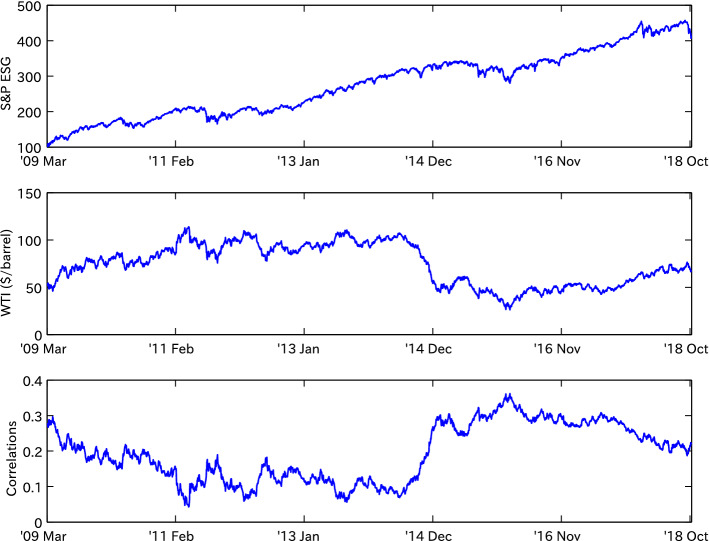

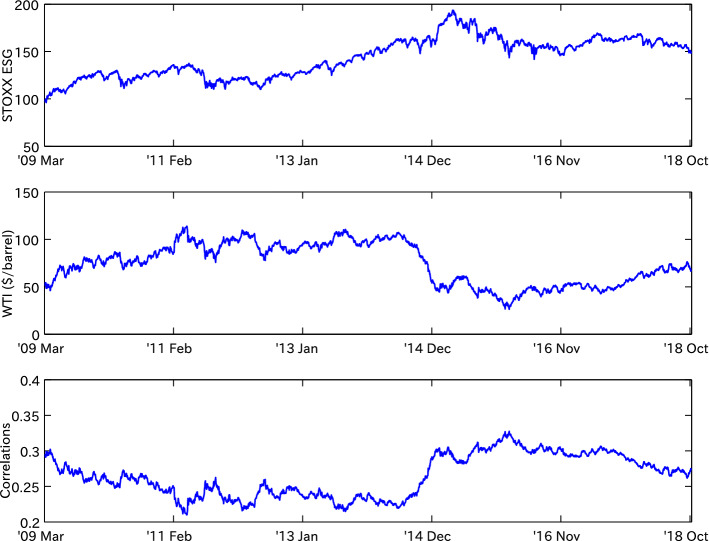

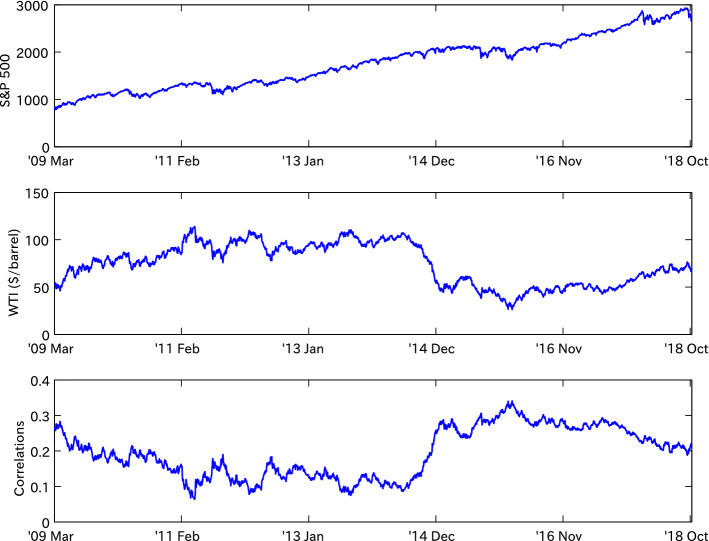

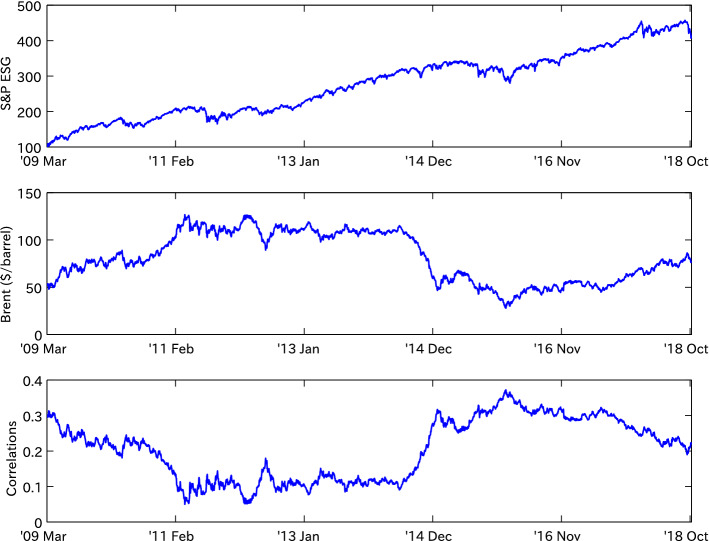

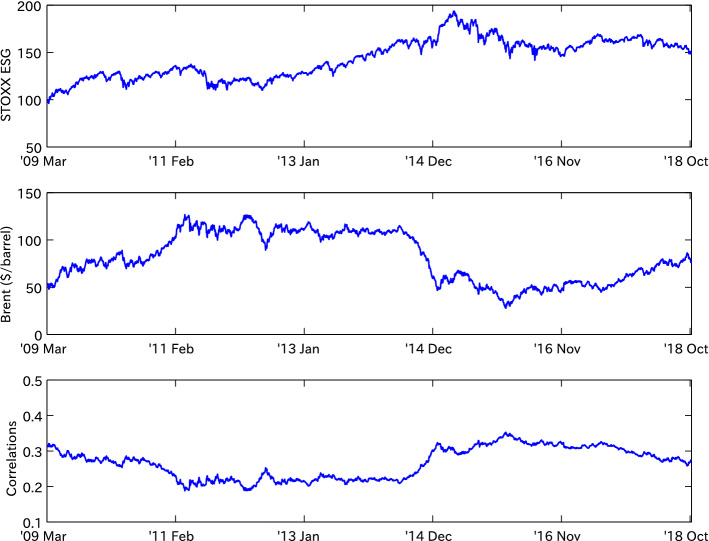

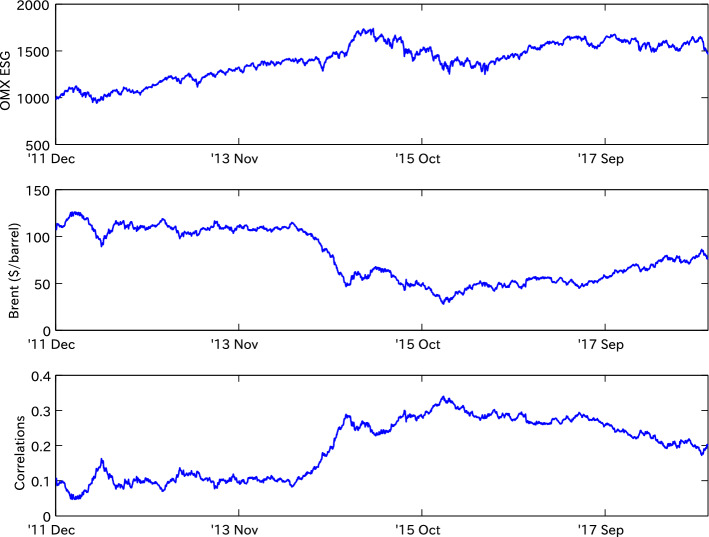

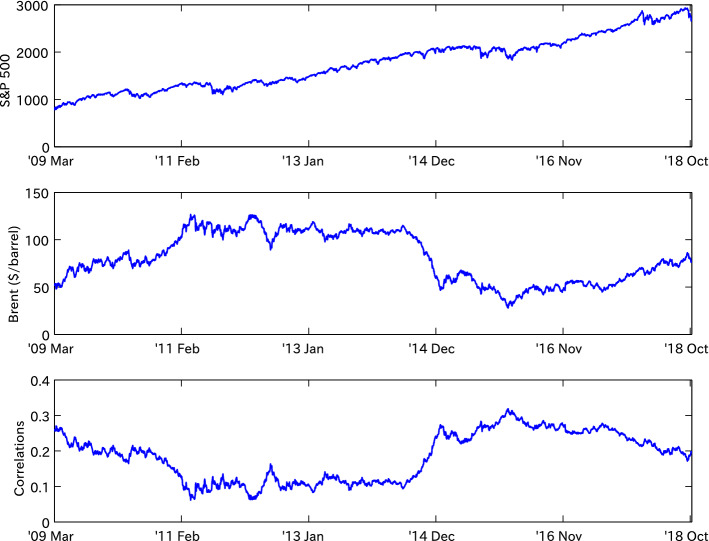

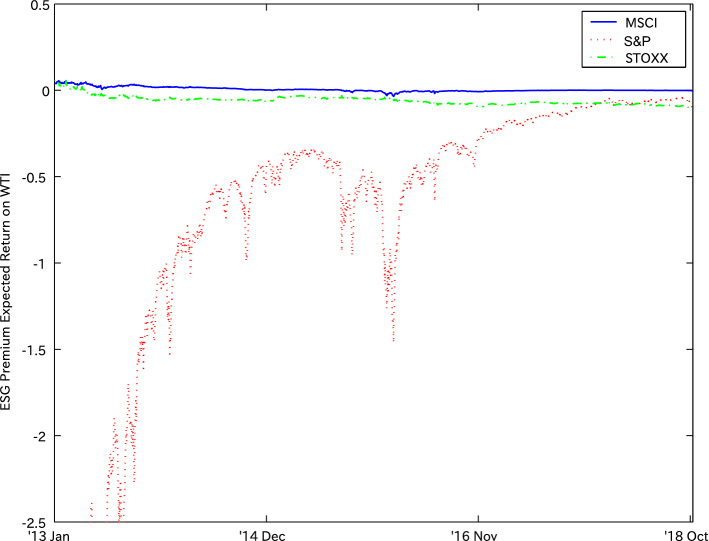

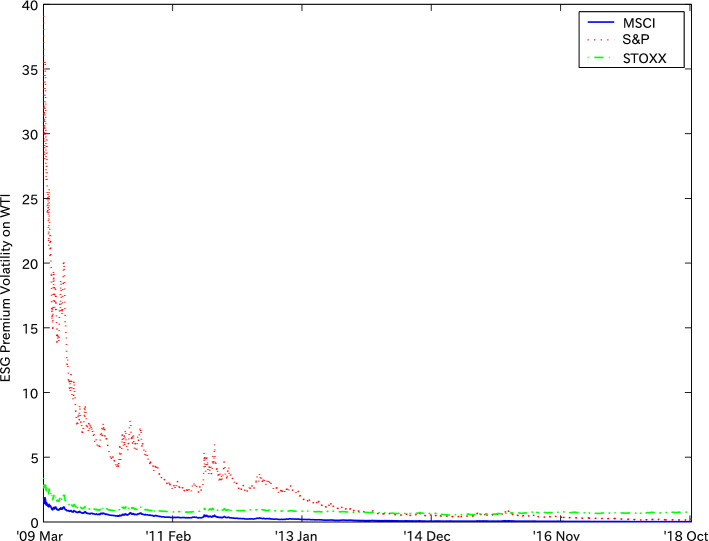

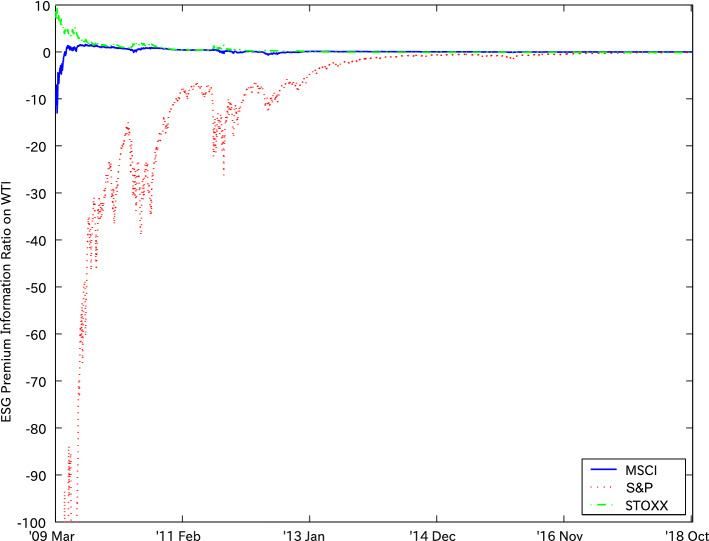

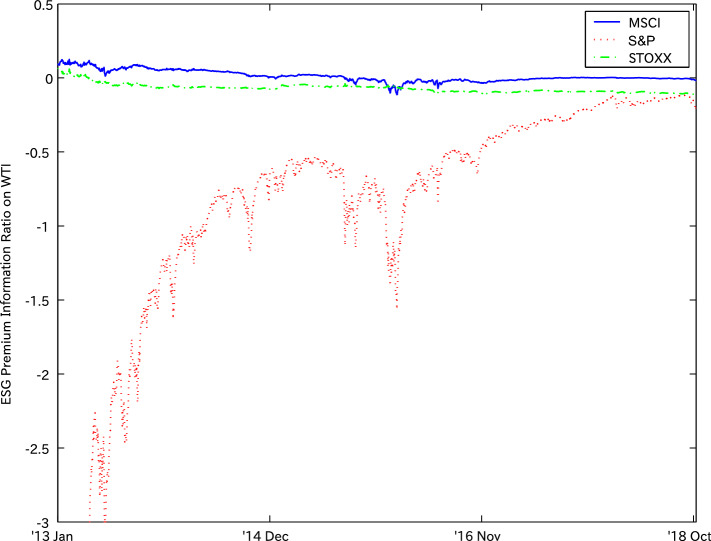

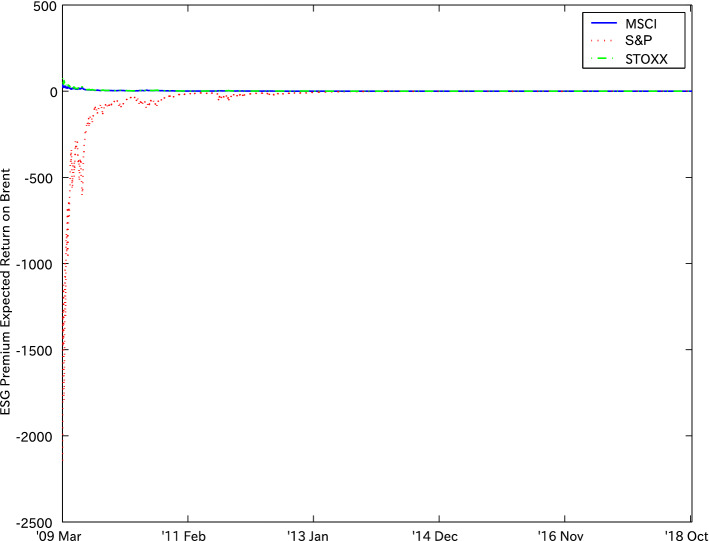

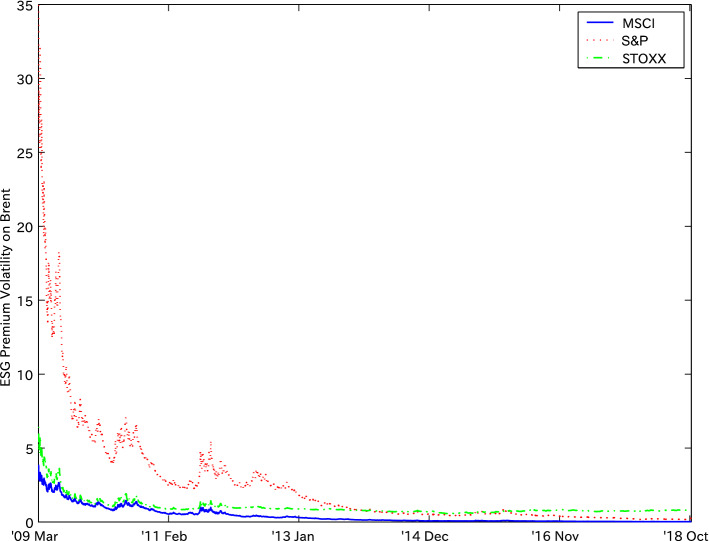

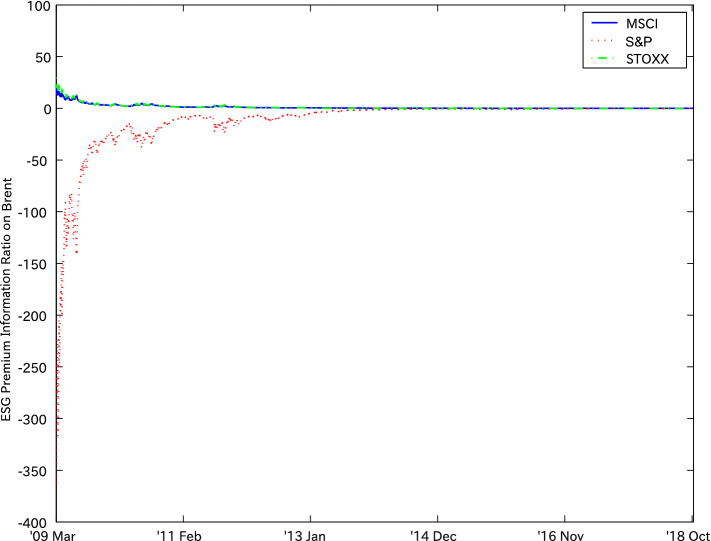

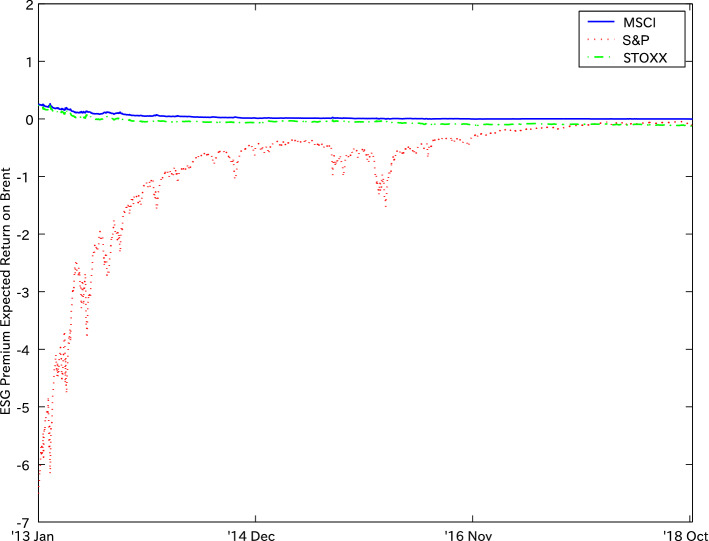

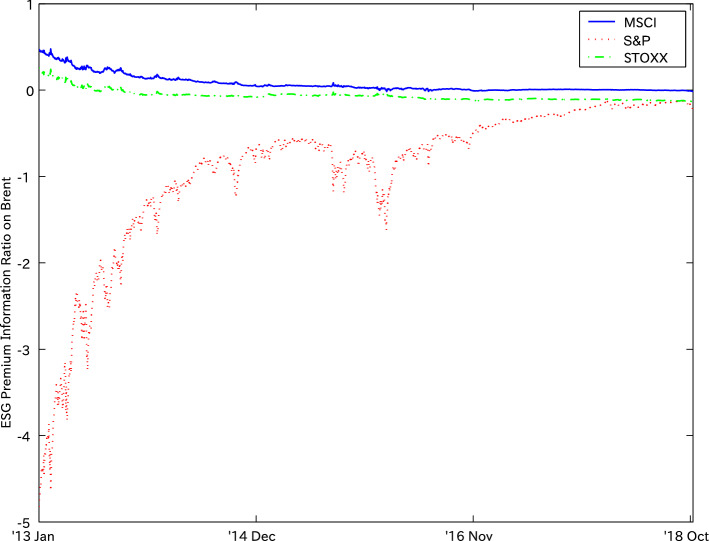

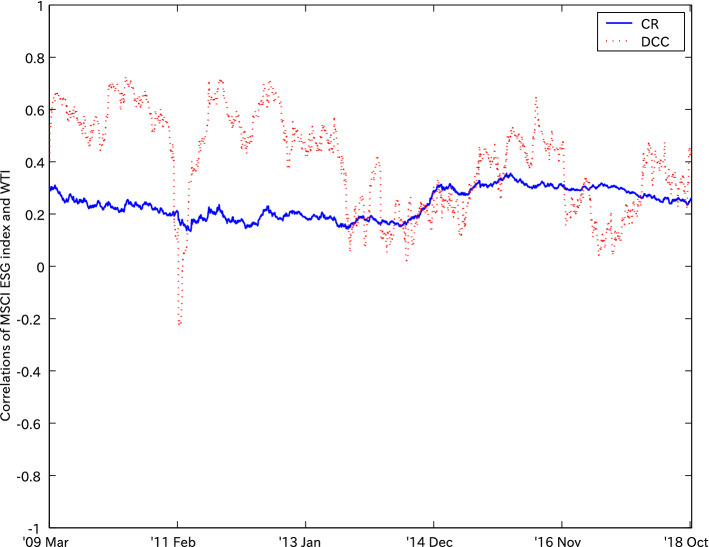

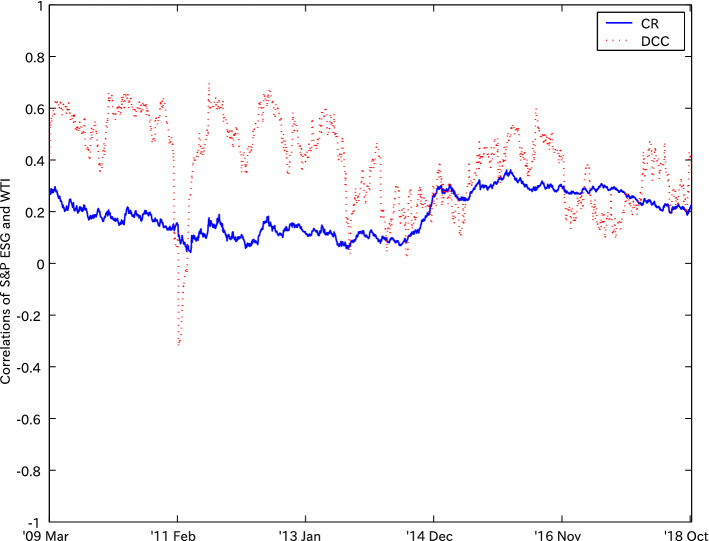

The objectives of this study are to analyze the presence of environmental values in ESG indexes based on the positive value relationship between energy and the environment found in existing studies and to identify the characteristics of environmental, social, and governance (ESG) investments by examining the performance of ESG investments compared to market portfolios, as well as to consider the implications of ESG investment in clean energy policy based on the results of the empirical analysis of this study. This paper contributes threefold. First, using a supply and demand-based pricing model, we propose a new model of the expected return, risk, and performance ratio of the ESG premiums defined by the log price differences between ESG indexes and a market portfolio to analyze how ESG investments perform. Second, based on the empirical findings of this study that the correlation between ESG indexes and energy prices is a decreasing function of the latter in contrast to other environmental assets, this paper suggests that ESG indexes cannot adequately demonstrate environmental values but reflect social and governance values, i.e., (E)SG, in the complementary perspective. Third, using the empirical findings of this study that the information ratio of the ESG premium tends to be positive but declines and approaches zero over time, this paper indicates that although ESG investments can be significant compared to market index investments, the significance is limited because ESG investment performance converges with market portfolio performance. In conclusion, two points should be noted about ESG investing in clean energy policy: given the dilution of environmental values in ESG investing, a clear distinction should be made between ESG investing and renewable energy investing; even if investments in renewable energy projects are treated as ESG investments, reflecting current market trends, we should be prepared for the fact that the superior investment performance due to social and governance values, rather than environmental values, will not last long.

本研究的目的是基于现有研究中发现的能源与环境之间的正向价值关系,分析环境价值在ESG指数中的存在情况;通过考察ESG投资相对于市场投资组合的表现,识别环境、社会和治理(ESG)投资的特征;并根据本研究的实证分析结果,思考ESG投资对清洁能源政策的影响。本文有三个方面的贡献。第一,使用基于供求的定价模型,我们提出了一个新的模型,用于分析由ESG指数与市场投资组合之间的对数价格差异所定义的ESG溢价的预期回报、风险和绩效比率,以分析ESG投资的表现。第二,基于本研究的实证结果,即与其他环境资产相比,ESG指数与能源价格之间的相关性是能源价格的递减函数,本文表明ESG指数不能充分体现环境价值,而是从互补的角度反映社会和治理价值,即(E)SG。第三,利用本研究的实证结果,即ESG溢价的信息比率往往为正,但随着时间的推移会下降并趋近于零,本文指出,尽管与市场指数投资相比,ESG投资可能具有重要意义,但这种意义是有限的,因为ESG投资表现会与市场投资组合表现趋同。总之,在清洁能源政策中的ESG投资方面应注意两点:鉴于ESG投资中环境价值的稀释,应明确区分ESG投资和可再生能源投资;即使将可再生能源项目投资视为ESG投资以反映当前市场趋势,我们也应做好准备,即由于社会和治理价值而非环境价值带来的卓越投资表现不会持续太久。