Castka Pavel, Searcy Cory

UC Business School, University of Canterbury, Christchurch 8041, New Zealand.

Yeates School of Graduate Studies, Toronto Metropolitan University, 350 Victoria St., Toronto, ON M5B 2K3, Canada.

Bus Horiz. 2023 Jan-Feb;66(1):5-11. doi: 10.1016/j.bushor.2021.11.003. Epub 2021 Nov 18.

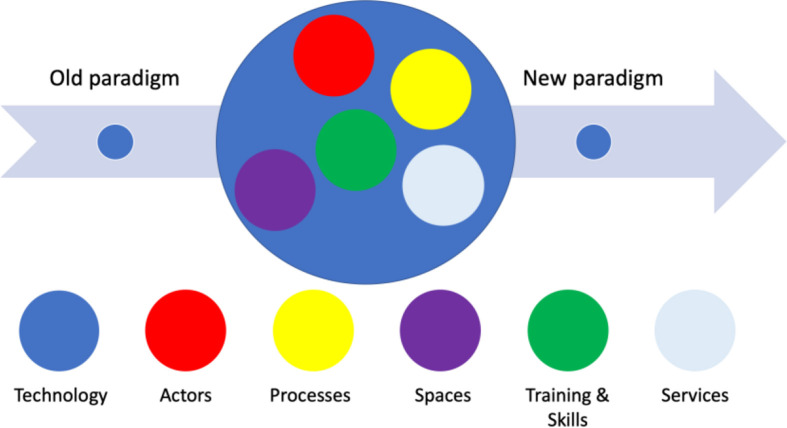

The COVID-19 pandemic has exposed the obsolescence and vulnerability of many existing auditing practices. While some progressive practices have been implemented (e.g., remote audits using rudimentary information and communication technologies), a new paradigm is needed not only to account for the risk of repeated lockdowns but also to align practices with the level of digitalization, automation, and use of artificial intelligence in the current business environment. In this article, we argue that the adoption of new technologies requires a fundamental rethinking of how auditing services are delivered. We argue that new technological possibilities have implications for five other auditing elements that enable a shift from the old to the new paradigm of auditing, namely actors, processes, spaces, training and skills development, and services. We explain how nonfinancial audits conducted under the new paradigm are key enablers of a firm's ability to participate and to thrive in a competitive international marketplace.

新冠疫情暴露了许多现有审计实践的过时与脆弱。虽然已经实施了一些先进的做法(例如使用基本信息和通信技术进行远程审计),但不仅需要一种新的模式来应对反复封锁的风险,还需要使实践与当前商业环境中的数字化、自动化和人工智能使用水平保持一致。在本文中,我们认为采用新技术需要从根本上重新思考审计服务的提供方式。我们认为,新的技术可能性对其他五个审计要素产生影响,这些要素能够推动从旧的审计模式向新的审计模式转变,即审计主体、流程、空间、培训与技能发展以及服务。我们解释了在新模式下进行的非财务审计如何成为企业在竞争激烈的国际市场中参与并蓬勃发展的关键推动因素。