Department of Mathematics, Assam University, Dargakona, Assam, India.

Department of Mathematics, Institute of Technology,Nirma University, Gujarat, India.

PLoS One. 2023 Mar 9;18(3):e0268996. doi: 10.1371/journal.pone.0268996. eCollection 2023.

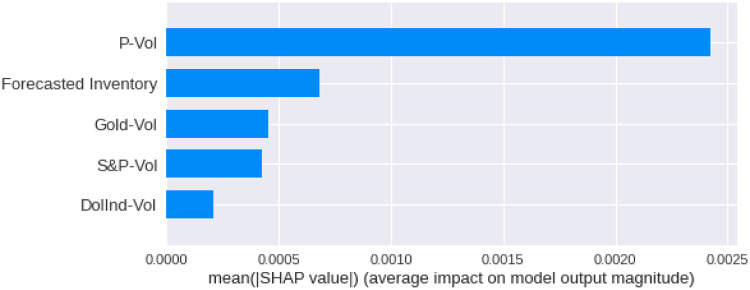

Crude Oil is one of the most important commodities in this world. We have studied the effects of Crude Oil inventories on crude oil prices over the last ten years (2011 to 2020). We tried to figure out how the Crude Oil price variance responds to inventory announcements. We then introduced several other financial instruments to study the relation of these instruments with Crude Oil variation. To undertake this task, we took the help of several mathematical tools including machine learning tools such as Long Short Term Memory(LSTM) methods, etc. The previous researches in this area primarily focussed on statistical methods such as GARCH (1,1) etc. (Bu (2014)). Various researches on the price of crude oil have been undertaken with the help of LSTM. But the variation of crude oil price has not yet been studied. In this research, we studied the variance of crude oil prices with the help of LSTM. This research will be beneficial for the options traders who would like to get benefit from the variance of the underlying instrument.

原油是世界上最重要的商品之一。我们研究了过去十年(2011 年至 2020 年)原油库存对原油价格的影响。我们试图找出原油价格变化如何对库存公告做出反应。然后,我们引入了其他几种金融工具来研究这些工具与原油变化的关系。为了完成这项任务,我们借助了包括机器学习工具(如长短时记忆(LSTM)方法等)在内的几种数学工具。该领域的先前研究主要集中在统计方法上,如 GARCH(1,1)等。(Bu(2014))。借助 LSTM 进行了各种关于原油价格的研究。但是,尚未研究原油价格的波动。在这项研究中,我们借助 LSTM 研究了原油价格的波动。这项研究将有利于希望从基础工具的波动中获利的期权交易员。