Faculty of Management, Royal Roads University, Victoria, BC, Canada.

PLoS One. 2023 Jul 17;18(7):e0287327. doi: 10.1371/journal.pone.0287327. eCollection 2023.

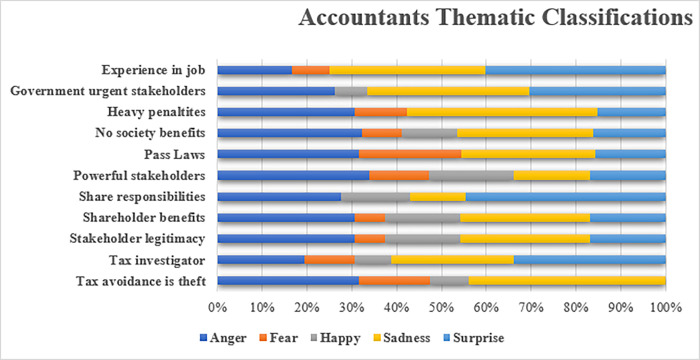

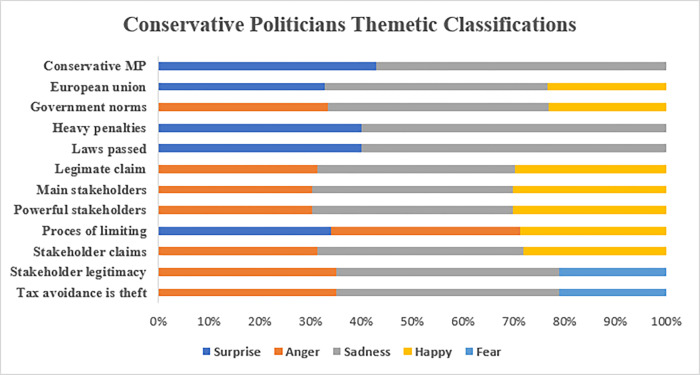

This paper examines the moral and legal underpinnings of corporate tax avoidance. Cast in terms of a totemic symbol that brand tax avoidance as within the purview of the law, the paper invokes the attributional frames of the new sociology of morality to examine the position of both the moral advocates and the amoral critics of aggressive tax avoidance. The paper uses the United Kingdom as a jurisdiction where complex tax planning by tax advisors serves as a measure of protection for corporations who may have already conceived that they are paying too much tax. Data for the paper came from semi-structured interviews conducted with tax accountants, consultants, parliamentarians, and government officials. To supplement the interviews, data from the Parliamentary Commission on Banking Standards were collected and analyzed to provide useful insights. The findings reveal that through effective tax planning, companies can reduce the present values of future tax payments. Given the singular justification of their actions within the contours of the tax rules, the moral culpability of organized tax avoidance is minimized, with very little liability attached. Tax avoidance is a morally charged area that is slowly drifting away from conventional social norms of what is right or wrong. It is hard not to see those in charge of tax regulation not using the findings of this paper to provide a more nuanced understanding of the intractable problems associated with corporate tax avoidance and use it as a reference point for regulatory reforms.

本文探讨了企业避税的道德和法律基础。本文以一个图腾符号为框架,将避税行为视为法律范围内的行为,援引新道德社会学的归因框架,考察了积极避税的道德辩护者和非道德批评者的立场。本文以英国为案例,在英国,税务顾问的复杂税务筹划被视为对那些可能已经认为自己缴纳过多税款的公司的一种保护措施。本文的数据来自对税务会计师、顾问、议员和政府官员进行的半结构化访谈。为了补充访谈,还收集和分析了议会银行标准委员会的数据,以提供有用的见解。研究结果表明,通过有效的税务筹划,公司可以降低未来税款的现值。鉴于其在税收规则范围内的行为只有单一的正当理由,组织性避税的道德罪责被最小化,几乎没有什么责任。避税是一个充满道德争议的领域,它正在慢慢偏离对错的传统社会规范。很难不让那些负责税收监管的人不利用本文的研究结果,对与企业避税相关的棘手问题有更细致的理解,并将其作为监管改革的参考点。