Pfeffer Jeffrey, Olsen Esther, Singer Sara J

Graduate School of Business, Stanford University, Stanford, California.

School of Medicine, Stanford University, Stanford, California.

JAMA Health Forum. 2025 Jan 3;6(1):e245229. doi: 10.1001/jamahealthforum.2024.5229.

Few studies have examined the extent to which employers emphasize financial over nonfinancial criteria in measurement, reporting, and decision-making about health care benefits.

To measure and identify factors associated with financial over nonfinancial emphasis in employer decision-making about health benefits.

DESIGN, SETTING, AND PARTICIPANTS: A survey was administered to a nationally representative sample of US employers to assess the extent of employers' emphasis on benefits plans' costs over member experience, access to care, and equity, and on financial vs other considerations when choosing third-party benefits administrators. The sample included in-company human resources administrators from randomly selected nongovernmental organizations with at least 50 employees. The survey was administered in 2 waves: May 2022 to July 2022 and November 2022 to April 2023.

The survey included 41 multipart questions capturing information about the respondent, company, company interactions with benefits consulting firms and benefits administrators, and company approach to managing employee health benefits.

Main outcomes were proportion of financially oriented measures that internal benefits administrators and external benefits consultants use and importance of financial vs other factors in companies' choice of third-party administrators.

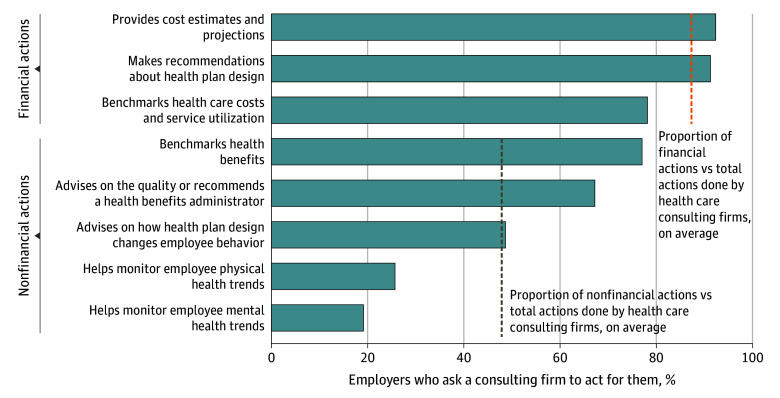

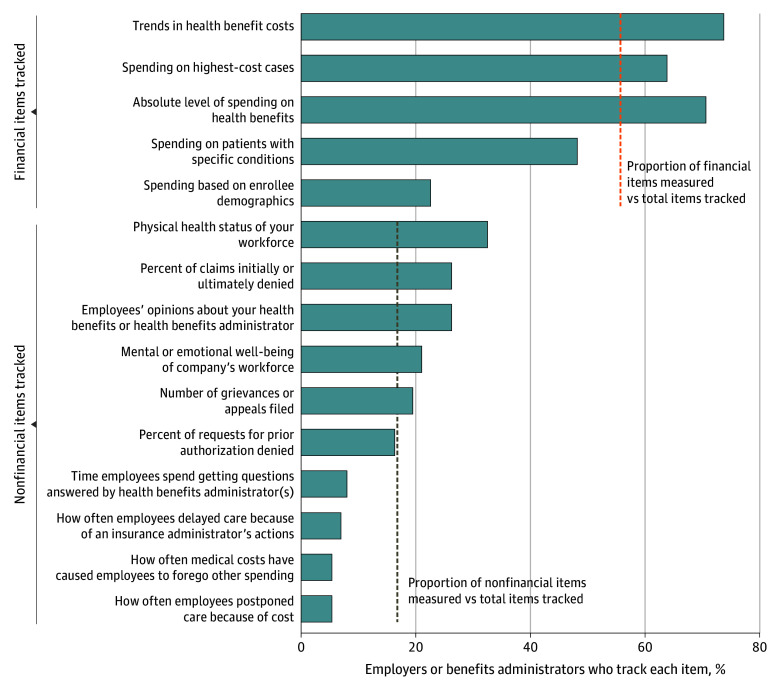

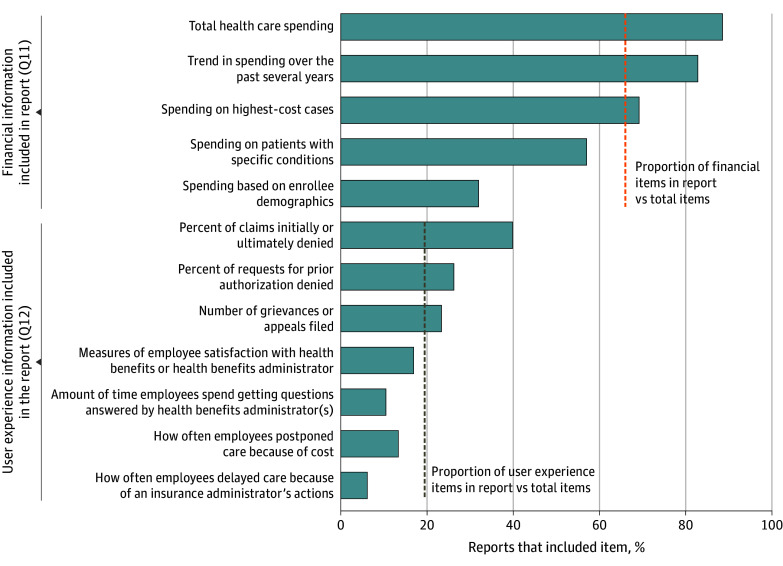

Of 1159 companies sampled, 251 (22%) responded; 30 with less than 50 employees were excluded. Of the 221 remaining companies, 147 (67%) used a benefits consulting firm. The companies and their benefits consultants focused on financial over nonfinancial performance dimensions in decision-making. While 125 companies (74%) tracked trends in health benefits costs and 109 (64%) tracked spending on the highest cost cases, only 14 (8%) tracked time employees spent having questions answered, and 12 (7%) tracked how often employees delayed receiving care because of an insurance company's actions. This financial focus was largely independent of organizational characteristics and other potential explanatory factors. Of 37 paired differences comparisons in the proportion of financial vs nonfinancial items, only 6 proportions (16%) differed significantly, with differences in proportions of 0.22 or less.

In this survey study, US employers emphasized financial over nonfinancial criteria in their measurement and decision-making about health benefits. To improve health plan performance, employer measurement and decision-making must emphasize both nonfinancial and financial criteria.

很少有研究考察雇主在医疗保健福利的衡量、报告和决策中,在多大程度上强调财务标准而非非财务标准。

衡量并确定与雇主在健康福利决策中强调财务而非非财务因素相关的因素。

设计、背景和参与者:对美国雇主的全国代表性样本进行了一项调查,以评估雇主在多大程度上强调福利计划的成本而非成员体验、就医机会和公平性,以及在选择第三方福利管理者时对财务因素与其他因素的考量。样本包括从随机选择的至少有50名员工的非政府组织中抽取的公司内部人力资源管理人员。调查分两波进行:2022年5月至2022年7月以及2022年11月至2023年4月。

该调查包括41个多部分问题,获取有关受访者、公司、公司与福利咨询公司及福利管理者的互动,以及公司管理员工健康福利方式的信息。

主要结局是内部福利管理者和外部福利顾问使用的以财务为导向的指标比例,以及财务因素与其他因素在公司选择第三方管理者时的重要性。

在抽样的1159家公司中,251家(22%)做出了回应;30家员工少于50人的公司被排除。在剩下的221家公司中,147家(67%)使用了福利咨询公司。这些公司及其福利顾问在决策中更关注财务而非非财务绩效维度。虽然125家公司(74%)跟踪健康福利成本趋势,109家(64%)跟踪最高成本案例的支出,但只有14家(8%)跟踪员工提问所花费的时间,12家(7%)跟踪员工因保险公司的行为而推迟接受治疗的频率。这种对财务的关注在很大程度上与组织特征和其他潜在解释因素无关。在财务项目与非财务项目比例的37对差异比较中,只有6个比例(16%)有显著差异,差异比例为0.22或更小。

在这项调查研究中,美国雇主在健康福利的衡量和决策中更强调财务标准而非非财务标准。为了提高健康计划的绩效,雇主的衡量和决策必须同时强调非财务和财务标准。