Botta Federico, Moat Helen Susannah, Stanley H Eugene, Preis Tobias

Centre for Complexity Science, University of Warwick, Coventry, CV4 7AL, United Kingdom; Data Science Lab, Behavioural Science, Warwick Business School, University of Warwick, Coventry, CV4 7AL, United Kingdom.

Data Science Lab, Behavioural Science, Warwick Business School, University of Warwick, Coventry, CV4 7AL, United Kingdom.

PLoS One. 2015 Sep 1;10(9):e0135600. doi: 10.1371/journal.pone.0135600. eCollection 2015.

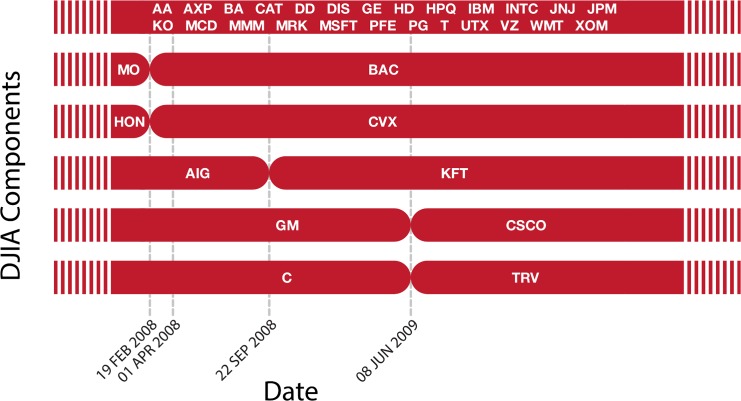

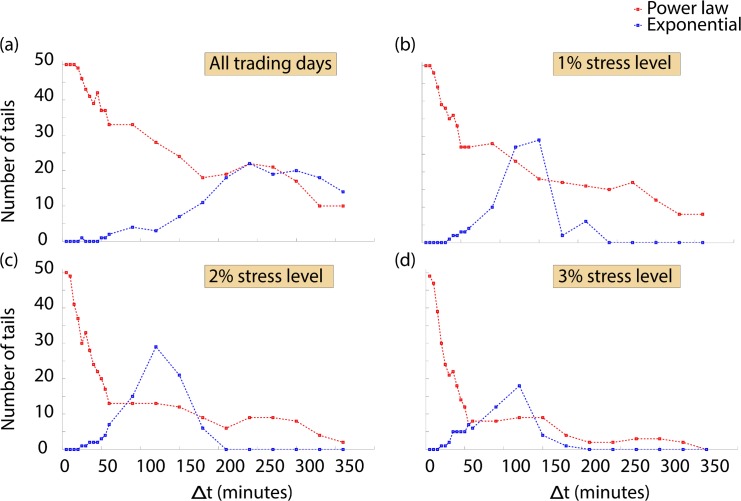

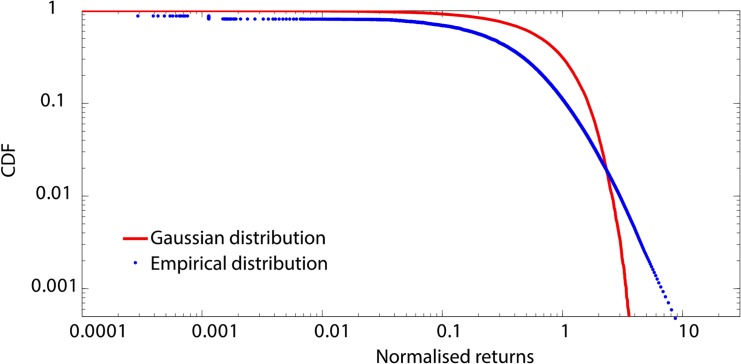

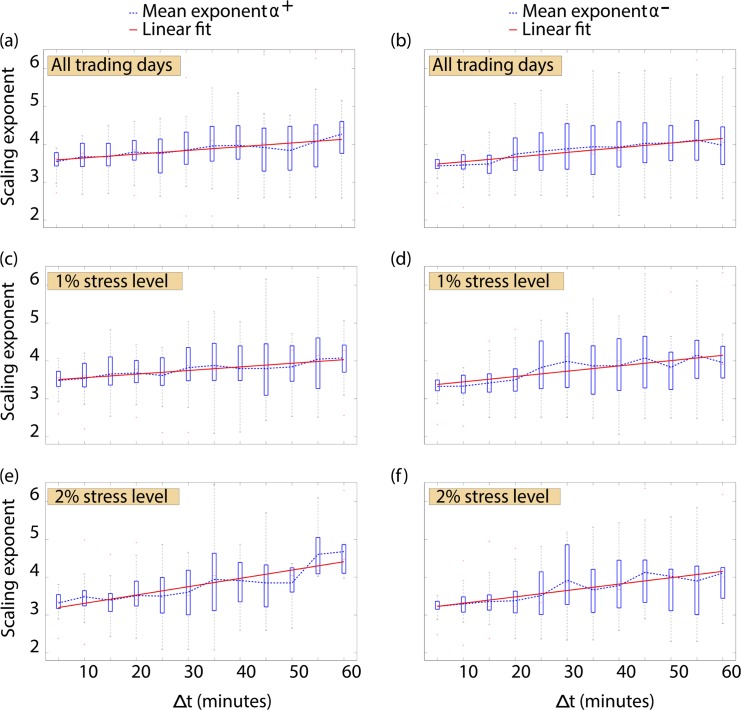

Being able to quantify the probability of large price changes in stock markets is of crucial importance in understanding financial crises that affect the lives of people worldwide. Large changes in stock market prices can arise abruptly, within a matter of minutes, or develop across much longer time scales. Here, we analyze a dataset comprising the stocks forming the Dow Jones Industrial Average at a second by second resolution in the period from January 2008 to July 2010 in order to quantify the distribution of changes in market prices at a range of time scales. We find that the tails of the distributions of logarithmic price changes, or returns, exhibit power law decays for time scales ranging from 300 seconds to 3600 seconds. For larger time scales, we find that the distributions tails exhibit exponential decay. Our findings may inform the development of models of market behavior across varying time scales.

能够量化股票市场大幅价格变动的概率对于理解影响全球人民生活的金融危机至关重要。股票市场价格的大幅变动可能在几分钟内突然出现,也可能在更长的时间尺度上发展。在这里,我们分析了一个数据集,该数据集包含2008年1月至2010年7月期间以秒为分辨率构成道琼斯工业平均指数的股票,以便量化一系列时间尺度上市场价格变化的分布。我们发现,对数价格变化(即回报)分布的尾部在300秒至3600秒的时间尺度上呈现幂律衰减。对于更大的时间尺度,我们发现分布的尾部呈现指数衰减。我们的发现可能为不同时间尺度上的市场行为模型的发展提供参考。