Kurnianingsih Yoanna A, Mullette-Gillman O'Dhaniel A

Department of Psychology, National University of Singapore Singapore, Singapore.

Department of Psychology, National University of SingaporeSingapore, Singapore; Neuroscience and Behavioral Disorders Program, Duke-NUS Graduate Medical SchoolSingapore, Singapore; Singapore Institute for Neurotechnology (SINAPSE), National University of SingaporeSingapore, Singapore.

Front Neurosci. 2015 Dec 16;9:457. doi: 10.3389/fnins.2015.00457. eCollection 2015.

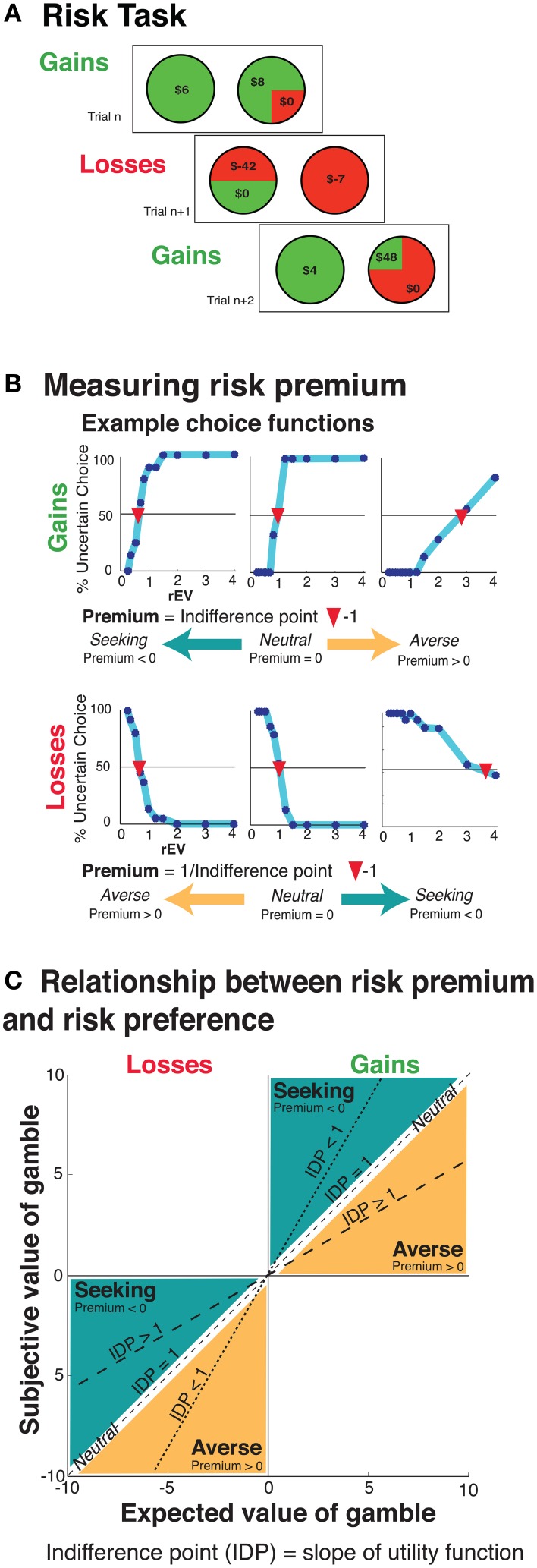

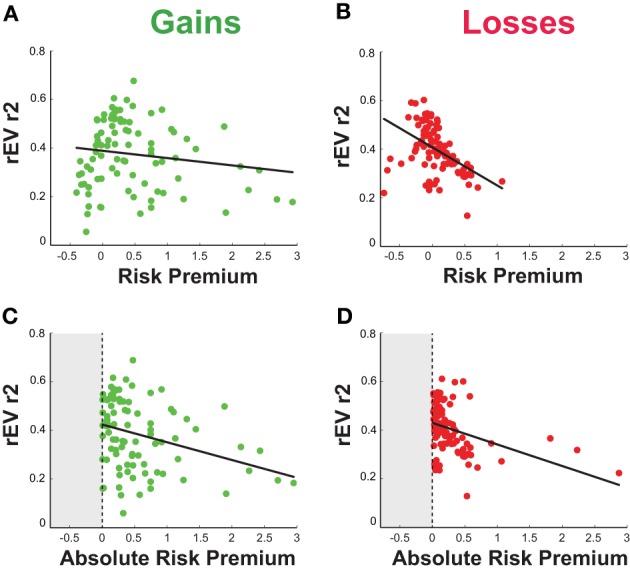

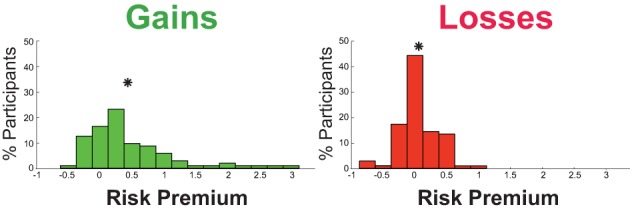

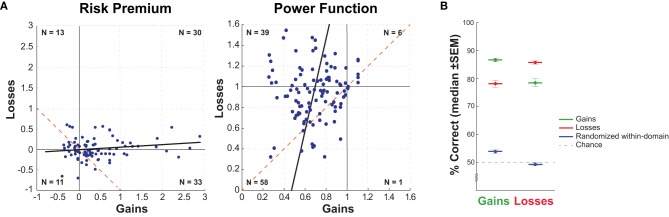

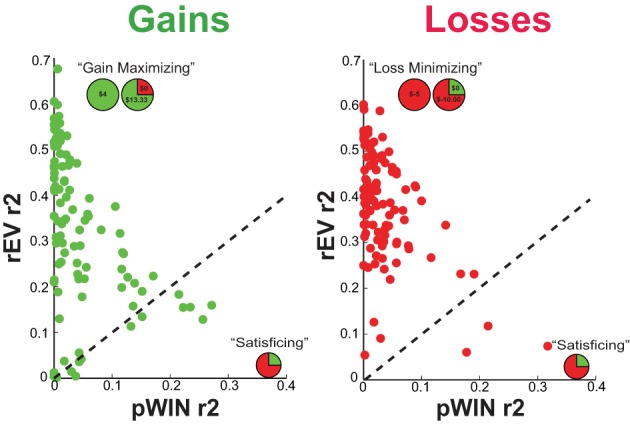

People choose differently when facing potential gains than when facing potential losses. Clear gross differences in decision making between gains and losses have been empirically demonstrated in numerous studies (e.g., framing effect, risk preference, loss aversion). However, theories maintain that there are strong underlying connections (e.g., reflection effect). We investigated the relationship between gains and losses decision making, examining risk preferences, and choice strategies (the reliance on option information) using a monetary gamble task with interleaved trials. For risk preferences, participants were on average risk averse in the gains domain and risk neutral/seeking in the losses domain. We specifically tested for a theoretically hypothesized correlation between individual risk preferences across the gains and losses domains (the reflection effect), but found no significant relationship in the predicted direction. Interestingly, despite the lack of reflected risk preferences, cross-domain risk preferences were still informative of individual choice behavior. For choice strategies, in both domains participants relied more heavily on the maximizing strategy than the satisficing strategy, with increased reliance on the maximizing strategy in the losses domain. Additionally, while there is no mathematical reliance between the risk preference and strategy metrics, within both domains there were significant relationships between risk preferences and strategies-the more participants relied upon the maximizing strategy the more risk neutral they were (equating value and utility maximization). These results demonstrate the complexity of gains and losses decision making, indicating the apparent contradiction that their underlying cognitive/neural processes are both dissociable and overlapping.

人们在面对潜在收益时的选择与面对潜在损失时不同。在众多研究中(如框架效应、风险偏好、损失厌恶),收益和损失之间决策上明显的总体差异已得到实证证明。然而,理论认为存在强大的潜在联系(如反射效应)。我们使用交错试验的货币赌博任务,研究了收益和损失决策之间的关系,考察了风险偏好和选择策略(对选项信息的依赖)。对于风险偏好,参与者在收益领域平均表现为风险厌恶,而在损失领域表现为风险中性/寻求风险。我们专门测试了收益和损失领域个体风险偏好之间理论上假设的相关性(反射效应),但未发现预测方向上的显著关系。有趣的是,尽管缺乏反射性风险偏好,但跨领域风险偏好仍能为个体选择行为提供信息。对于选择策略,在两个领域中,参与者更多地依赖最大化策略而非满意策略,在损失领域对最大化策略的依赖增加。此外,虽然风险偏好和策略指标之间没有数学上的依赖关系,但在两个领域内,风险偏好和策略之间都存在显著关系——参与者越依赖最大化策略,他们就越风险中性(将价值和效用最大化等同)。这些结果证明了收益和损失决策的复杂性,表明其潜在的认知/神经过程既可分离又重叠这一明显矛盾。