Csermely Tamás, Rabas Alexander

University of Vienna, Doctoral School of Operations Management and Logistics, Oskar Morgenstern Platz 1, 1090 Vienna, Austria.

Vienna University of Economics and Business, Institute for Public Sector Economics, Vienna, Austria.

J Risk Uncertain. 2016;53(2):107-136. doi: 10.1007/s11166-016-9247-6. Epub 2017 Feb 1.

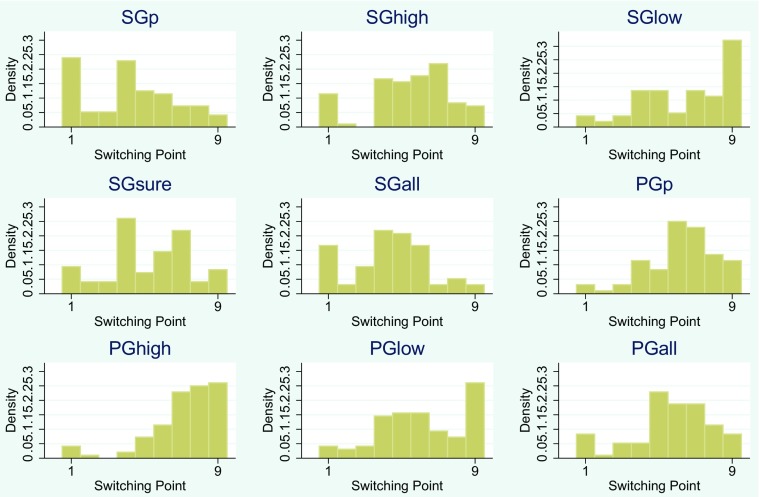

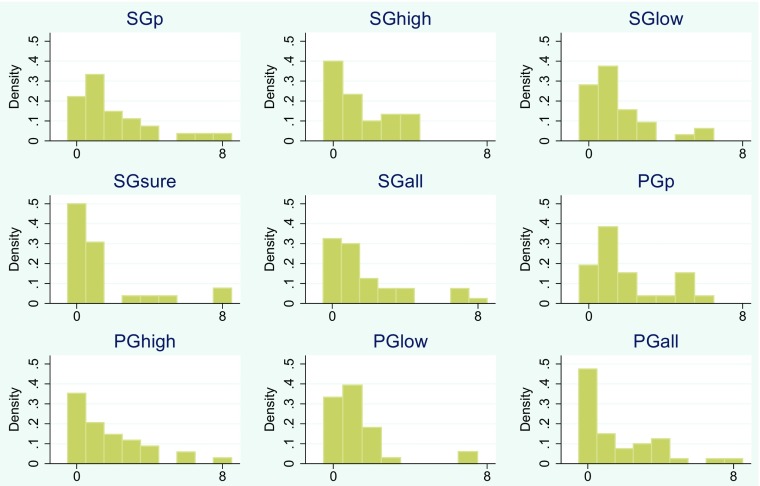

The question of how to measure and classify people's risk preferences is of substantial importance in the field of economics. Inspired by the multitude of ways used to elicit risk preferences, we conduct a holistic investigation of the most prevalent method, the multiple price list (MPL) and its derivations. In our experiment, we find that revealed preferences differ under various versions of MPLs as well as yield unstable results within a 30-minute time frame. We determine the most stable elicitation method with the highest forecast accuracy by using multiple measures of within-method consistency and by using behavior in two economically relevant games as benchmarks. A derivation of the well-known method by Holt and Laury (American Economic Review (5):1644-1655, 2002), where the highest payoff is varied instead of probabilities, emerges as the best MPL method in both dimensions. As we pinpoint each MPL characteristic's effect on the revealed preference and its consistency, our results have implications for preference elicitation procedures in general.

如何衡量和分类人们的风险偏好问题在经济学领域至关重要。受用于引出风险偏好的多种方式的启发,我们对最普遍的方法——多重价格列表(MPL)及其衍生方法进行了全面研究。在我们的实验中,我们发现,在MPL的不同版本下,显示偏好存在差异,并且在30分钟的时间范围内结果也不稳定。我们通过使用方法内一致性的多种度量,并以两个经济相关博弈中的行为作为基准,确定了预测准确性最高的最稳定引出方法。由霍尔特和劳里(《美国经济评论》(5):1644 - 1655,2002年)提出的著名方法的一种衍生方法,即改变最高收益而非概率,在这两个维度上均成为最佳的MPL方法。由于我们确定了每个MPL特征对显示偏好及其一致性的影响,我们的结果总体上对偏好引出程序具有启示意义。