Sheffield Alcohol Research Group, School of Health and Related Research, University of Sheffield, UK.

Addiction. 2019 Aug;114(8):1489-1494. doi: 10.1111/add.14631. Epub 2019 May 30.

The World Health Organization recommends increasing alcohol taxes as a 'best-buy' approach to reducing alcohol consumption and improving population health. Alcohol may be taxed based on sales value, product volume or alcohol content; however, duty structures and rates vary, both among countries and between beverage types. From a public health perspective, the best duty structure links taxation level to alcohol content, keeps pace with inflation and avoids substantial disparities between different beverage types. This data note compares current alcohol duty structures and levels throughout the 28 European Union (EU) Member States and how these vary by alcohol content, and also considers implications for public health.

Descriptive analysis using administrative data, European Union, July 2018.

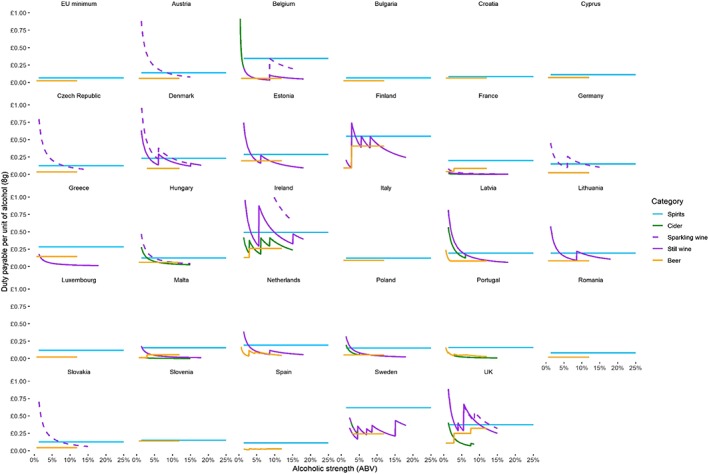

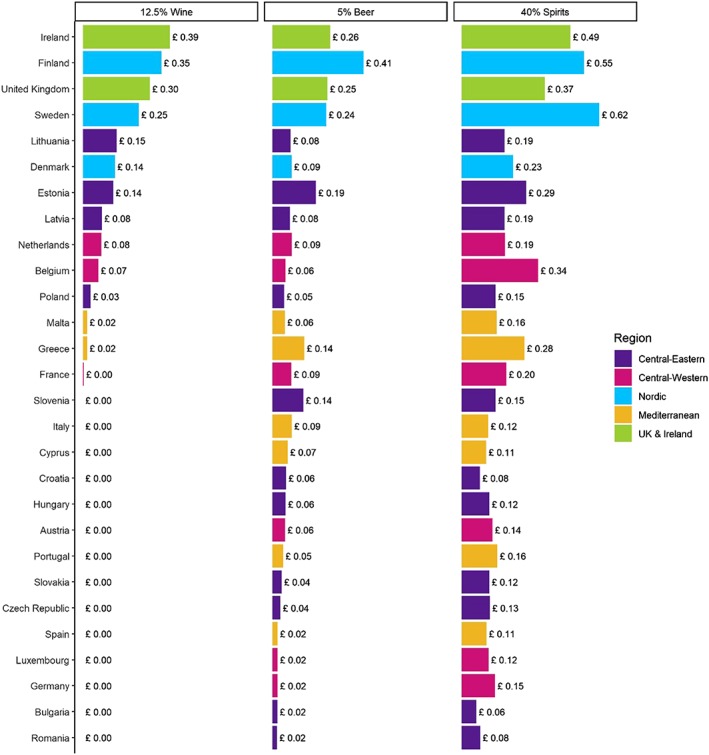

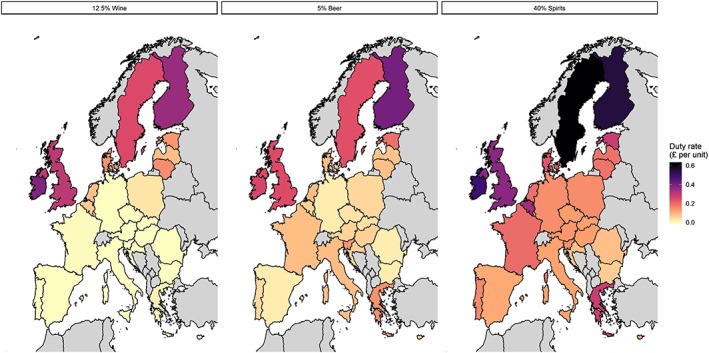

Beverage-specific alcohol duty rates per UK alcohol unit (8 g ethanol) in pounds sterling at a range of different alcoholic strengths.

Only 50% of Member States levy any duty on wine and several levy duty on spirits and beer at or close to the EU minimum level. There is at least a 10-fold difference in the effective duty rate per unit between the highest- and lowest-duty countries for each beverage type. Duty rates for beer and spirits stay constant with strength in the majority of countries, while rates for wine and cider generally fall as strength increases. Duty rates are generally higher for spirits than other beverage types and are generally lowest in eastern Europe and highest in Finland, Sweden, Ireland and the United Kingdom.

Different European Union countries enact very different alcohol taxation policies, despite a partially restrictive legal framework. There is only limited evidence that alcohol duties are designed to minimize public health harms by ensuring that drinks containing more alcohol are taxed at higher rates. Instead, tax rates appear to reflect national alcohol production and consumption patterns.

世界卫生组织建议提高酒精税,将其作为减少酒精消费和改善人口健康的“最佳选择”。酒精税可以根据销售价值、产品数量或酒精含量征收;然而,关税结构和税率在国家之间和饮料类型之间都有所不同。从公共卫生的角度来看,最佳的关税结构将税收水平与酒精含量联系起来,与通货膨胀保持同步,并避免不同饮料类型之间的巨大差异。本数据说明比较了整个欧盟 28 个成员国目前的酒精关税结构和水平,以及这些结构和水平如何根据酒精含量而变化,并考虑了对公共卫生的影响。

使用行政数据进行描述性分析,欧盟,2018 年 7 月。

按英国酒精单位(8 克乙醇)计算的各种饮料的具体酒精税率,以不同的酒精强度为单位,以英镑计算。

只有 50%的成员国对葡萄酒征收任何关税,而有几个成员国对烈酒和啤酒征收的关税接近或低于欧盟的最低水平。对于每种饮料类型,最高和最低关税国家之间的单位有效税率差异至少为 10 倍。在大多数国家,啤酒和烈酒的税率与强度保持不变,而葡萄酒和苹果酒的税率通常随着强度的增加而下降。烈酒的税率通常高于其他饮料类型,东欧的税率普遍较低,芬兰、瑞典、爱尔兰和英国的税率较高。

尽管法律框架部分受限,但不同的欧盟国家制定了非常不同的酒精税收政策。只有有限的证据表明,酒精税的目的是通过确保含酒精量较高的饮料征收更高的税率来尽量减少对公共健康的危害。相反,税率似乎反映了国家的酒精生产和消费模式。