Department of Psychiatry and Psychotherapy, Center for Interdisciplinary Addiction Research (ZIS), University Medical Center Hamburg-Eppendorf (UKE), Hamburg, Germany.

Department of Psychiatry, Medical Faculty, University of Leipzig, Leipzig, Germany.

Appl Health Econ Health Policy. 2024 May;22(3):363-374. doi: 10.1007/s40258-024-00873-5. Epub 2024 Feb 22.

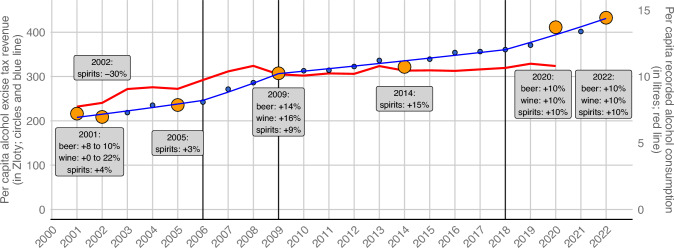

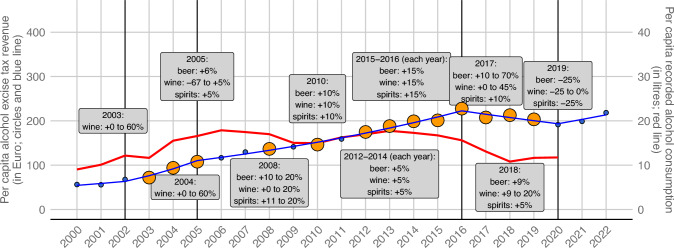

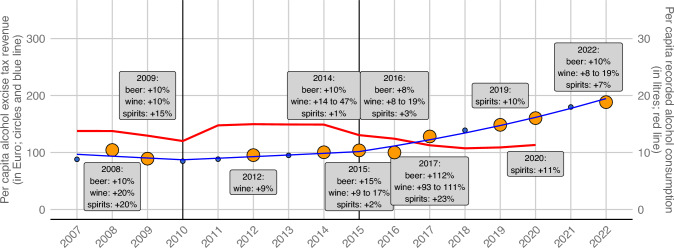

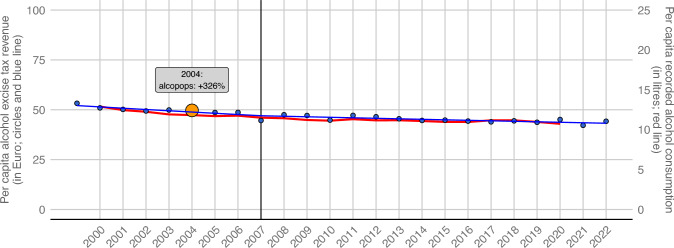

Reducing the affordability of alcoholic beverages by increasing alcohol excise taxation can lead to a reduction in alcohol consumption but the impact on government alcohol excise tax revenue is poorly understood. This study aimed to (a) describe cross-country tax revenue variations and (b) investigate how changes in taxation were related to changes in government tax revenue, using data from Estonia, Germany, Latvia, Lithuania and Poland.

For the population aged 15 years or older, we calculated the annual per capita alcohol excise tax revenue, total tax revenue, gross domestic product and alcohol consumption. In addition to descriptive analyses, joinpoint regressions were performed to identify whether changes in alcohol excise taxation were linked to changes in alcohol excise revenue since 1999.

In 2022, the per capita alcohol excise tax revenue was lowest in Germany (€44.2) and highest in Estonia (€218.4). In all countries, the alcohol excise tax revenue was mostly determined by spirit sales (57-72% of total alcohol tax revenue). During 2010-20, inflation-adjusted per capita alcohol excise tax revenues have declined in Germany (- 22.9%), Poland (- 19.1%) and Estonia (- 4.2%) and increased in Latvia (+ 56.8%) and Lithuania (+ 49.3%). In periods of policy non-action, alcohol consumption and tax revenue showed similar trends, but tax level increases were accompanied by increased revenue and stagnant or decreased consumption.

Increasing alcohol taxation was not linked to decreased but increased government revenue. Policymakers can increase revenue and reduce alcohol consumption and harm by increasing alcohol taxes.

通过提高酒精消费税来降低酒精饮料的可负担性,可导致酒精消费减少,但政府酒精消费税收入的影响尚不清楚。本研究旨在:(a) 描述各国之间的税收收入差异;(b) 利用爱沙尼亚、德国、拉脱维亚、立陶宛和波兰的数据,调查税收变化与政府税收收入变化之间的关系。

我们为年龄在 15 岁或以上的人群计算了每年人均酒精消费税收入、总税收收入、国内生产总值和酒精消费。除了描述性分析外,我们还进行了 joinpoint 回归,以确定自 1999 年以来,酒精消费税的变化是否与酒精消费税收入的变化有关。

2022 年,人均酒精消费税收入最低的是德国(44.2 欧元),最高的是爱沙尼亚(218.4 欧元)。在所有国家,酒精消费税收入主要由烈酒销售决定(占总酒精税收入的 57-72%)。在 2010-20 年期间,经通胀调整后的人均酒精消费税收入在德国(-22.9%)、波兰(-19.1%)和爱沙尼亚(-4.2%)下降,在拉脱维亚(+56.8%)和立陶宛(+49.3%)增加。在政策未发生变化的时期,酒精消费和税收呈现出相似的趋势,但税收水平的提高伴随着收入的增加和消费的停滞或减少。

提高酒精税并没有导致政府收入减少,反而增加了收入。提高酒精税可以增加收入、减少酒精消费和危害。