UK Centre for Tobacco and Alcohol Studies, Division of Epidemiology and Public Health, University of Nottingham, Clinical Sciences Building, City Hospital, Nottingham NG5 1PB, UK.

Int J Environ Res Public Health. 2019 Aug 9;16(16):2842. doi: 10.3390/ijerph16162842.

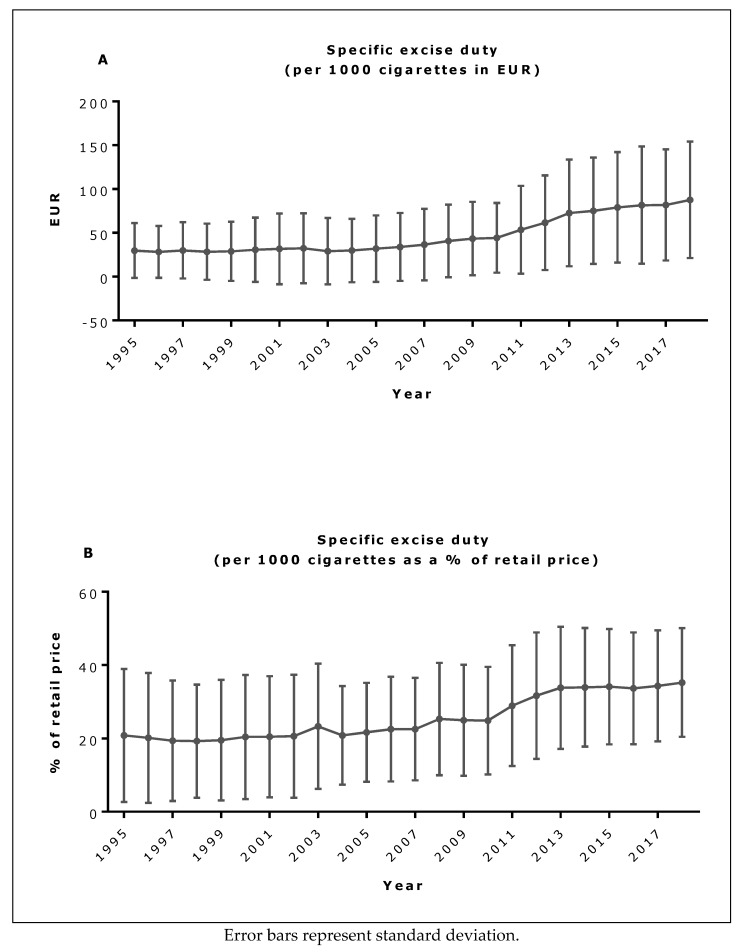

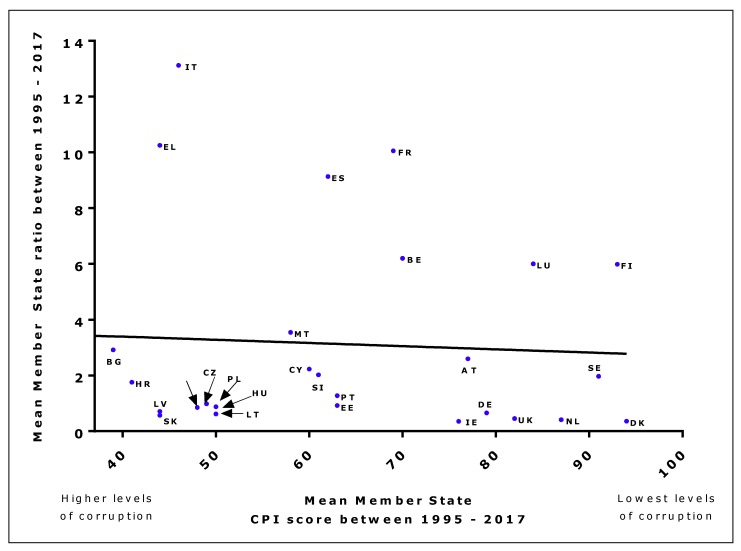

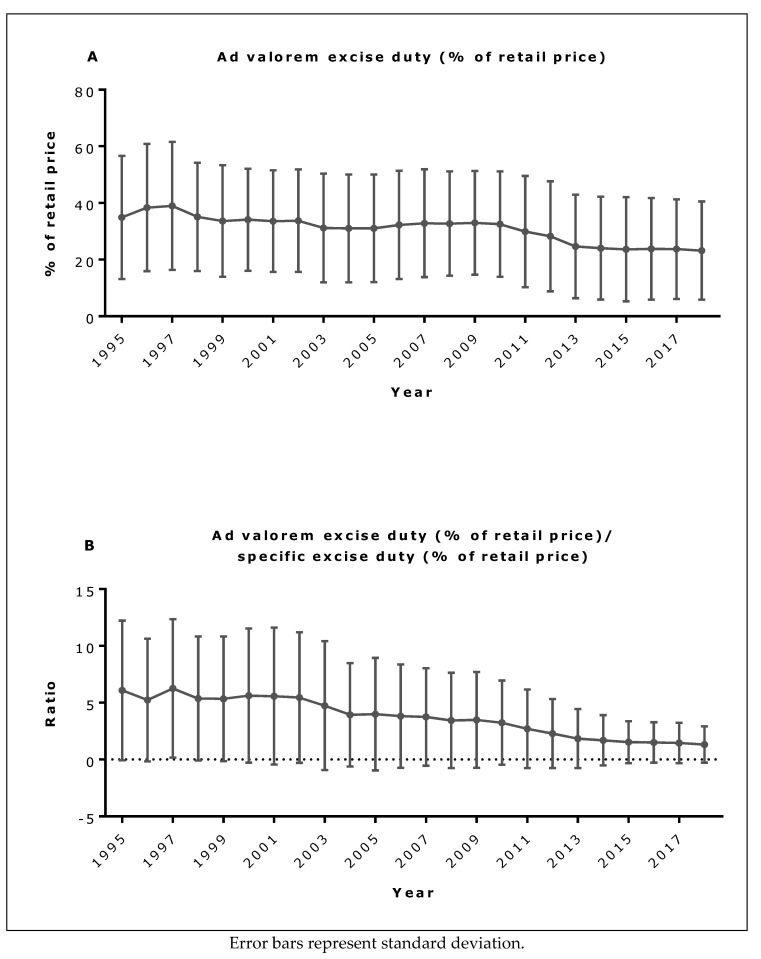

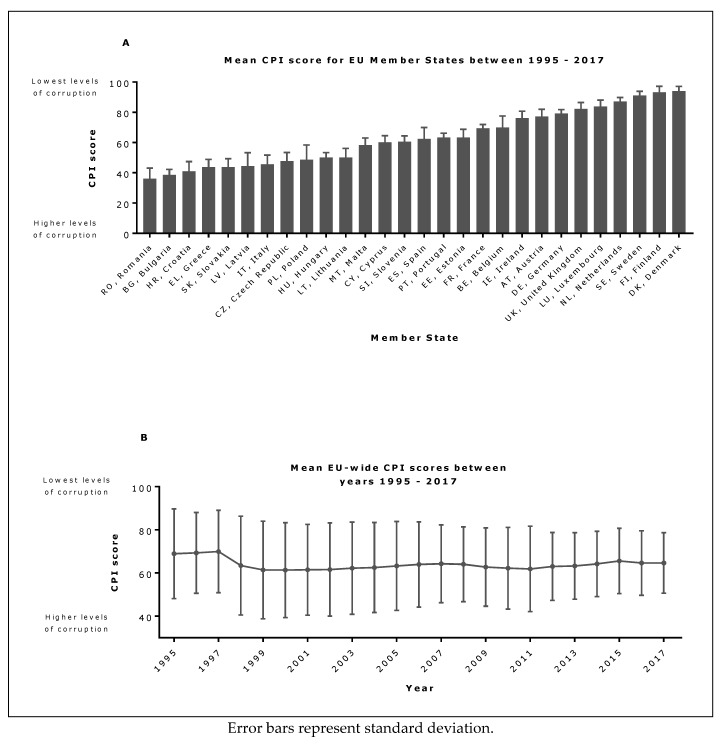

: Taxing tobacco products is one of the most effective tobacco control measures, and most countries apply a combination of specific taxes, which comprise a fixed amount per cigarette or gram of hand-rolling tobacco, and ad valorem taxes, which increase in proportion to the cost of the product. Since specific taxes reduce price differentials across tobacco product ranges while ad valorem taxes amplify them, we hypothesised that tobacco companies seeking to minimise the effect of tax increases on sales across a range of products will tend to favour, and hence lobby for, ad valorem rather than specific taxes; and that relatively corrupt governments would be more susceptible to such lobbying and hence, more likely to favour ad valorem taxes. : We searched for cigarette tax data and Transparency International Corruption Perceptions Index (CPI) scores for current 28 EU Member States for the years 1995 to 2017/8. Trends in cigarette tax levels and the ratio of ad valorem to specific taxes at a national and mean EU level were analysed by visual inspection, the within-country relation between the ad valorem to specific tax ratio and CPI scores over time by time-series regression analysis, and at EU level, for which complete data were available from 1995 to 2017, using a multi-level regression model. : Within most Member States, the ad valorem to specific cigarette tax ratio declined over the study period and was not significantly associated with corruption score. However, at an aggregate EU-level, our multi-level model indicated that reduced corruption was associated with a significant increase in the ad valorem to specific cigarette tax ratio, by 0.04 (95% confidence interval: 0.003-0.077, < 0.036) per unit increase in CPI score. : The ratio of ad valorem to specific taxes declined in most EU Member States over the study period, with no evidence that those with higher levels of perceived corruption tended to favour ad valorem taxes.

对烟草产品征税是最有效的控烟措施之一,大多数国家都采用了特定税收和从价税的组合,其中特定税收按每支香烟或每克手工卷制烟草的固定金额征收,从价税则按产品成本的比例增加。由于特定税收降低了不同烟草产品价格之间的差异,而从价税则放大了这种差异,我们假设,为了最大限度地减少一系列产品价格上涨对销售的影响,烟草公司将倾向于支持从价税而非特定税;相对腐败的政府更容易受到这种游说的影响,因此更倾向于支持从价税。我们为 1995 年至 2017/8 年期间的当前 28 个欧盟成员国搜索了香烟税收数据和透明国际腐败感知指数(CPI)得分。通过视觉检查分析了国家和欧盟平均水平的香烟税水平和从价税与特定税的比例趋势,通过时间序列回归分析分析了一个国家内的从价税与特定税的比例与 CPI 得分之间的关系随时间的变化,以及在欧盟层面上,对于 1995 年至 2017 年期间可用的完整数据,使用了多层次回归模型。在大多数成员国中,从价税与特定香烟税的比例在研究期间下降,与腐败得分没有显著关联。然而,在欧盟的总体水平上,我们的多层次模型表明,腐败程度的降低与从价税与特定香烟税的比例显著增加有关,CPI 得分每增加一个单位,这一比例就增加 0.04(95%置信区间:0.003-0.077,<0.036)。在研究期间,大多数欧盟成员国的从价税与特定税的比例下降,没有证据表明那些被认为腐败程度较高的国家倾向于支持从价税。