The Water Institute, Gillings School of Global Public Health, University of North Carolina at Chapel Hill, Chapel Hill, NC 27599, USA.

School of Civil Engineering, University of Leeds, Leeds LS2 9JT, UK.

Int J Environ Res Public Health. 2020 Mar 20;17(6):2075. doi: 10.3390/ijerph17062075.

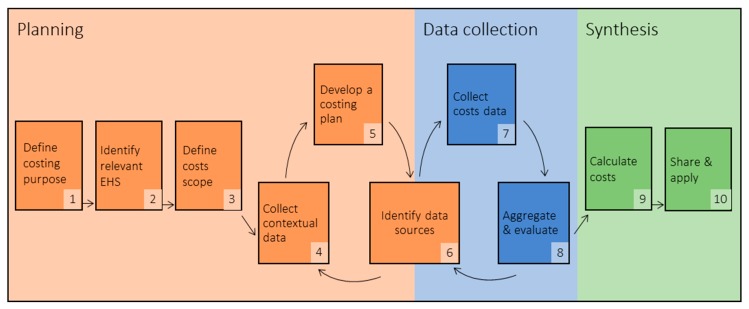

Environmental health services (EHS) in healthcare facilities (HCFs) are critical for safe care provision, yet their availability in low- and middle-income countries is low. A poor understanding of costs hinders progress towards adequate provision. Methods are inconsistent and poorly documented in costing literature, suggesting opportunities to improve evidence. The goal of this research was to develop a model to guide budgeting for EHS in HCFs. Based on 47 studies selected through a systematic review, we identified discrete budgeting steps, developed codes to define each step, and ordered steps into a model. We identified good practices based on a review of additional selected guidelines for costing EHS and HCFs. Our model comprises ten steps in three phases: planning, data collection, and synthesis. Costing-stakeholders define the costing purpose, relevant EHS, and cost scope; assess the EHS delivery context; develop a costing plan; and identify data sources (planning). Stakeholders then execute their costing plan and evaluate the data quality (data collection). Finally, stakeholders calculate costs and disseminate findings (synthesis). We present three hypothetical costing examples and discuss good practices, including using costing frameworks, selecting appropriate indicators to measure the quantity and quality of EHS, and iterating planning and data collection to select appropriate costing approaches and identify data gaps.

医疗机构中的环境卫生服务(EHS)对于安全的医疗服务提供至关重要,但在中低收入国家,其可用性很低。对成本的理解不足阻碍了充分供应的进展。成本核算文献中的方法不一致且记录不完整,这表明有机会改进证据。这项研究的目的是开发一个模型,为医疗机构中的环境卫生服务提供预算编制指导。我们通过系统评价选择了 47 项研究,根据这些研究确定了离散的预算编制步骤,制定了定义每个步骤的代码,并将步骤按模型进行了排序。我们根据对额外选定的环境卫生服务和医疗机构成本核算指南的审查,确定了良好做法。我们的模型由三个阶段的十个步骤组成:规划、数据收集和综合。成本核算利益相关者定义成本核算目的、相关的环境卫生服务和成本范围;评估环境卫生服务提供情况;制定成本核算计划;并确定数据来源(规划)。然后,利益相关者执行其成本核算计划并评估数据质量(数据收集)。最后,利益相关者计算成本并传播调查结果(综合)。我们提出了三个假设性的成本核算示例,并讨论了良好做法,包括使用成本核算框架、选择适当的指标来衡量环境卫生服务的数量和质量,以及迭代规划和数据收集,以选择适当的成本核算方法并确定数据差距。