Penalver Adrian, Hanaki Nobuyuki, Akiyama Eizo, Funaki Yukihiko, Ishikawa Ryuichiro

Banque de France, France.

Institute of Social and Economic Research, Osaka University, Japan.

J Econ Dyn Control. 2020 Oct;119:103978. doi: 10.1016/j.jedc.2020.103978. Epub 2020 Aug 29.

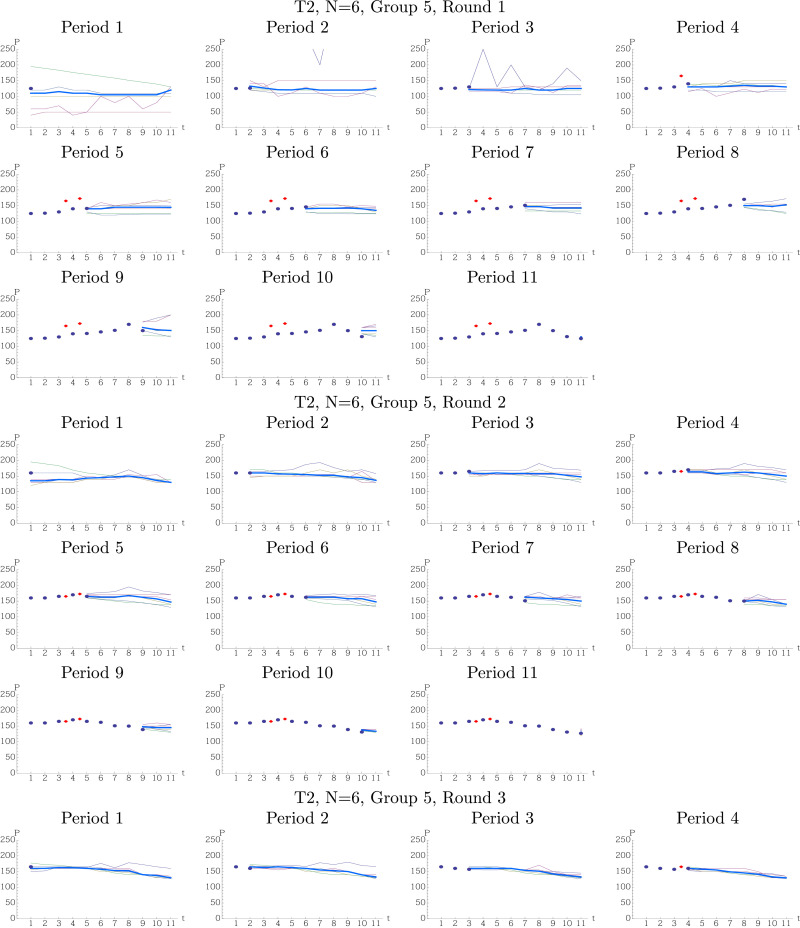

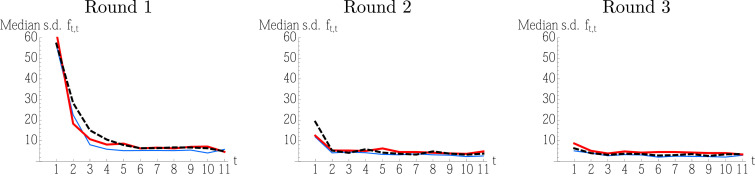

We experimentally investigate the effect of a central bank buying bonds for cash in a quantitative easing (QE) operation. In our experiment, the bonds are perfect substitutes for cash and have a constant fundamental value which is not affected by QE in the rational expectations equilibrium. We find that QE raises bond prices above those in the benchmark treatment without QE. Subjects in the benchmark treatment learned to trade the bonds at their fundamental value but those in treatments with QE became more convinced after repeated exposure to the same treatment that QE boosts bond prices. This suggests the possibility of a behavioural channel for the observed effects of actual QE operations on bond yields.

我们通过实验研究了中央银行在量化宽松(QE)操作中用现金购买债券的效果。在我们的实验中,债券是现金的完美替代品,并且具有恒定的基本价值,在理性预期均衡中不受量化宽松的影响。我们发现,量化宽松使债券价格高于无量化宽松的基准处理中的价格。基准处理中的受试者学会了按债券的基本价值进行交易,但经历了相同处理的量化宽松处理中的受试者在反复接触后更确信量化宽松会推高债券价格。这表明实际量化宽松操作对债券收益率的观测效果可能存在行为渠道。