Institute of Innovative Research, Tokyo Institute of Technology, Yokohama, Kanagawa, Japan.

Sony Computer Science Laboratories, Tokyo, Japan.

PLoS One. 2020 Sep 18;15(9):e0239494. doi: 10.1371/journal.pone.0239494. eCollection 2020.

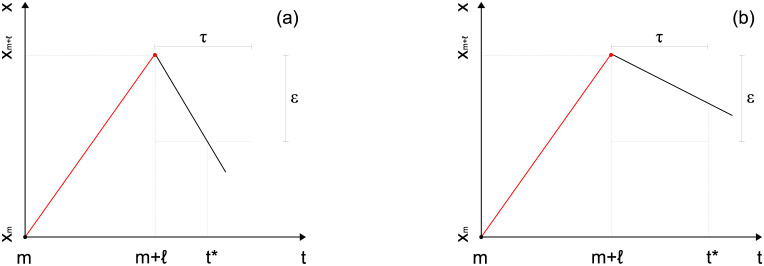

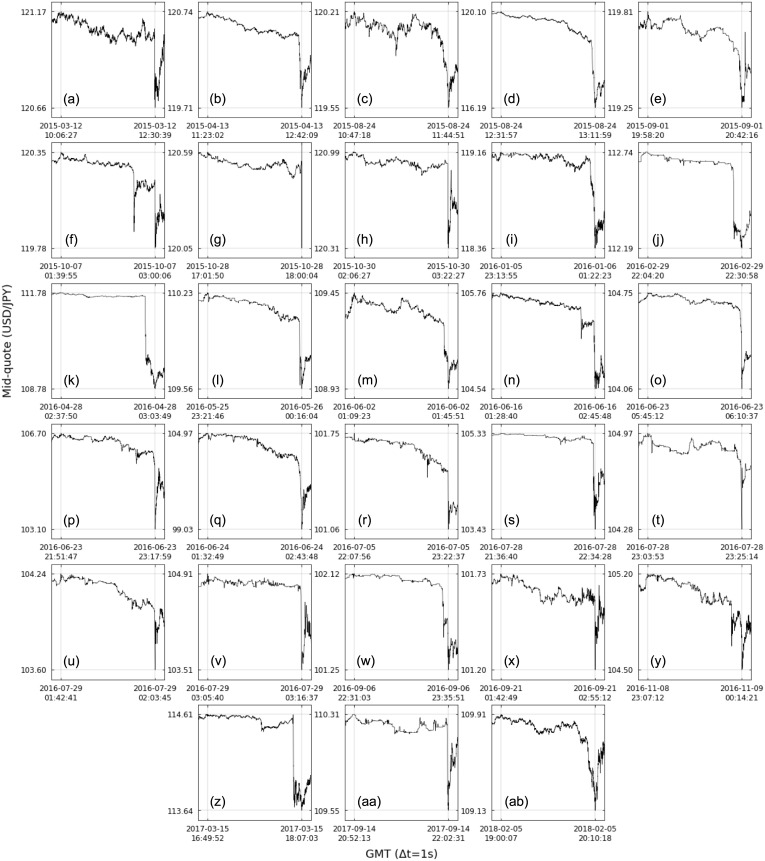

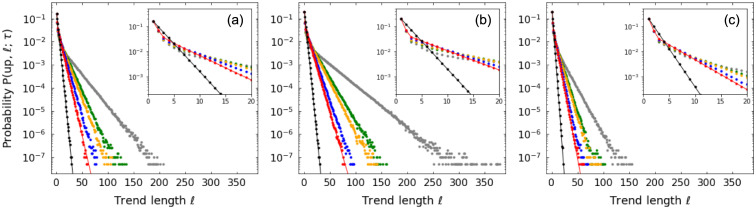

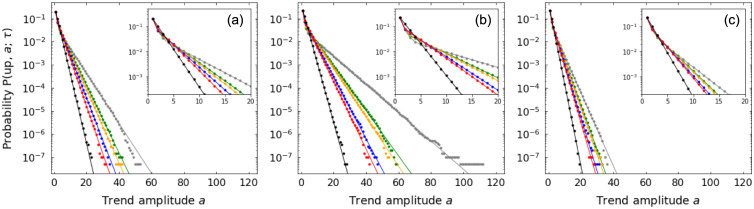

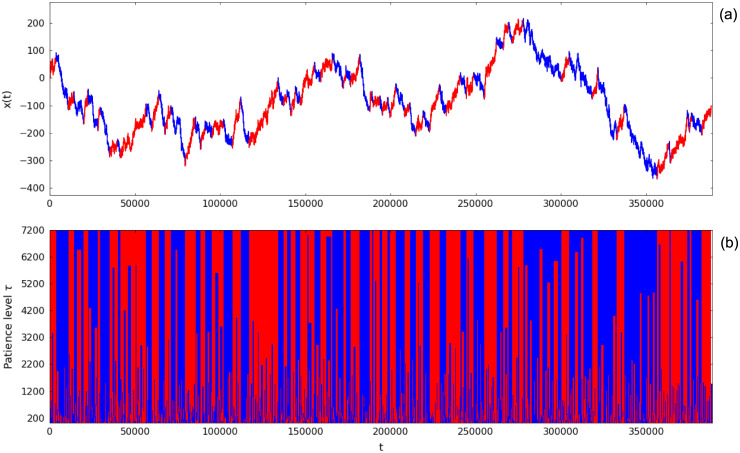

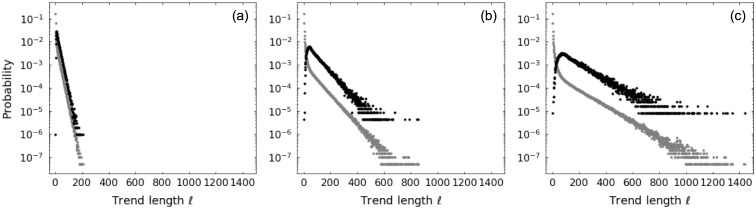

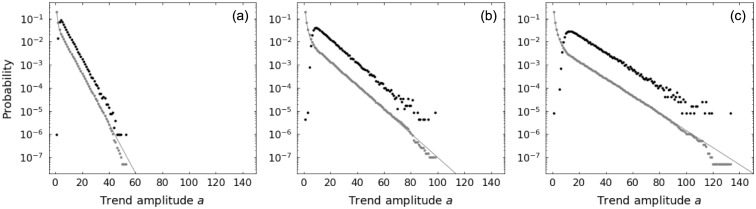

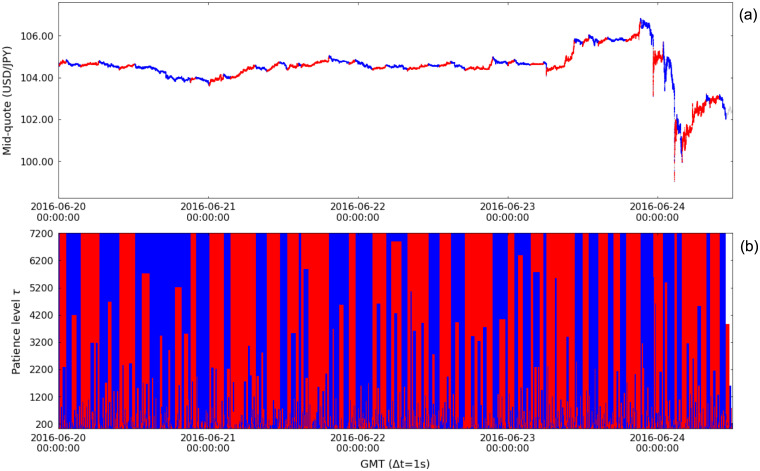

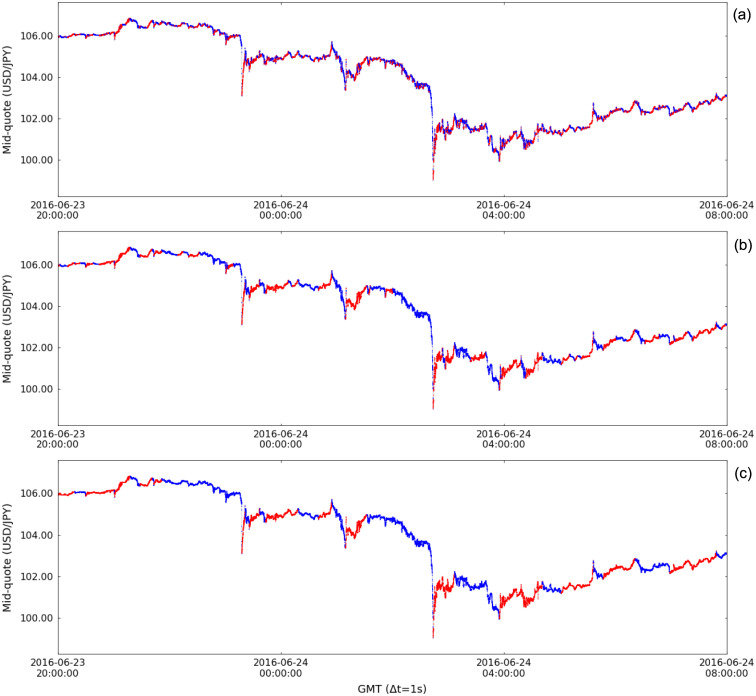

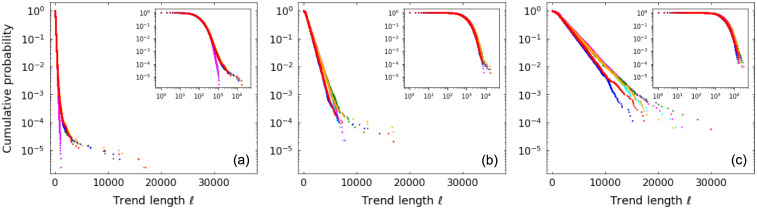

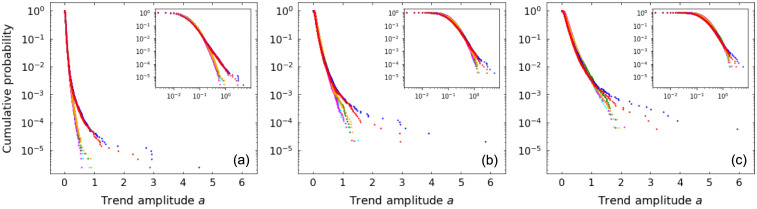

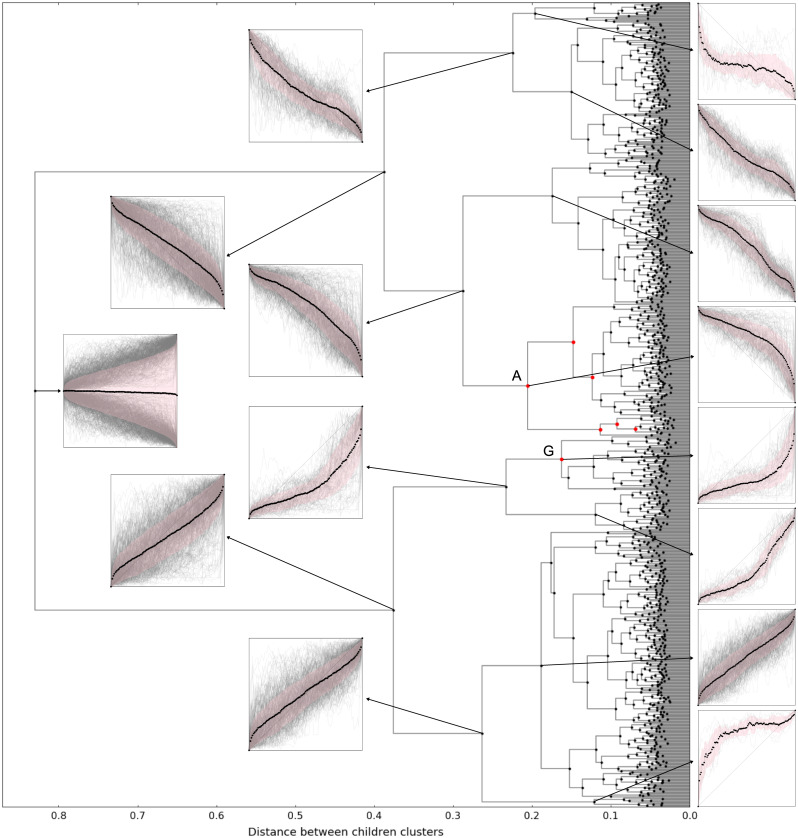

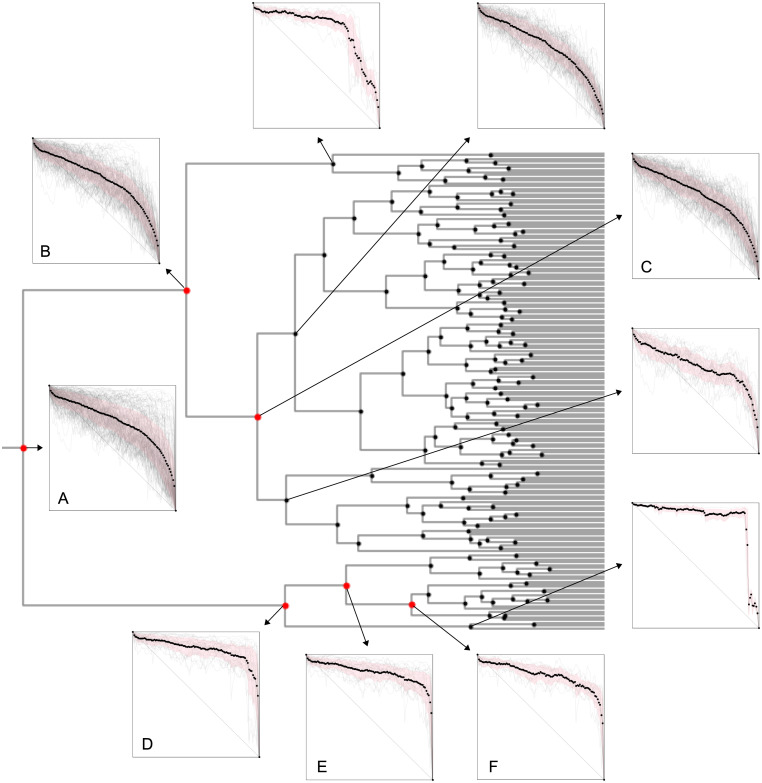

We propose the epsilon-tau procedure to determine up- and down-trends in a time series, working as a tool for its segmentation. The method denomination reflects the use of a tolerance level ε for the series values and a patience level τ in the time axis to delimit the trends. We first illustrate the procedure in discrete random walks, deriving the exact probability distributions of trend lengths and trend amplitudes, and then apply it to segment and analyze the trends of U.S. dollar (USD)/Japanese yen (JPY) market time series from 2015 to 2018. Besides studying the statistics of trend lengths and amplitudes, we investigate the internal structure of the trends by grouping trends with similar shapes and selecting clusters of shapes that rarely occur in the randomized data. Particularly, we identify a set of down-trends presenting similar sharp appreciation of the yen that are associated with exceptional events such as the Brexit Referendum in 2016.

我们提出了 ε-τ 方法来确定时间序列中的上升和下降趋势,作为其分割的工具。该方法的命名反映了对序列值使用容忍水平 ε 和时间轴上的耐心水平 τ 来限制趋势。我们首先在离散随机游走中说明该方法,推导出趋势长度和趋势幅度的精确概率分布,然后将其应用于分割和分析 2015 年至 2018 年期间美元(USD)/日元(JPY)市场时间序列的趋势。除了研究趋势长度和幅度的统计数据外,我们还通过对具有相似形状的趋势进行分组,并选择在随机数据中很少出现的形状聚类,来研究趋势的内部结构。特别地,我们确定了一组呈现出相似日元急剧升值的下降趋势,这些趋势与 2016 年英国脱欧公投等特殊事件有关。