Choi Sun-Yong

Department of Financial Mathematics, Gachon University, Gyeoggi 13120, Republic of Korea.

Financ Res Lett. 2020 Nov;37:101783. doi: 10.1016/j.frl.2020.101783. Epub 2020 Sep 29.

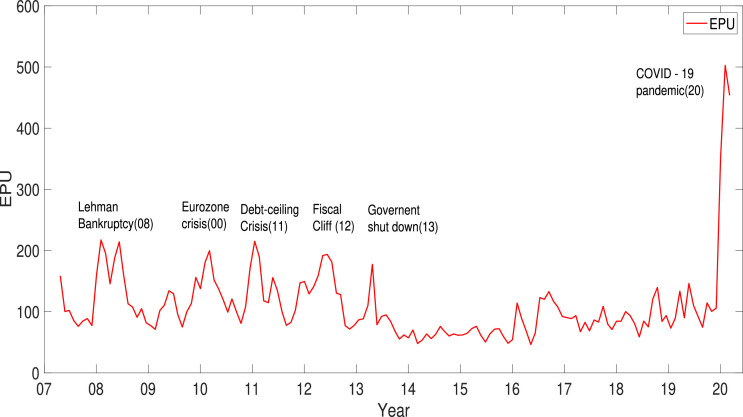

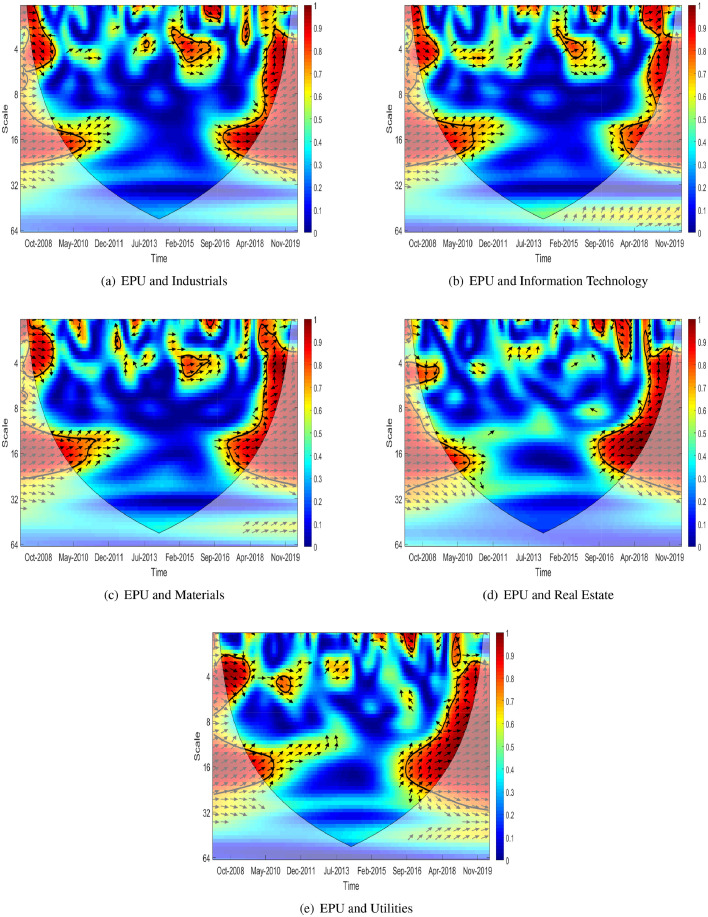

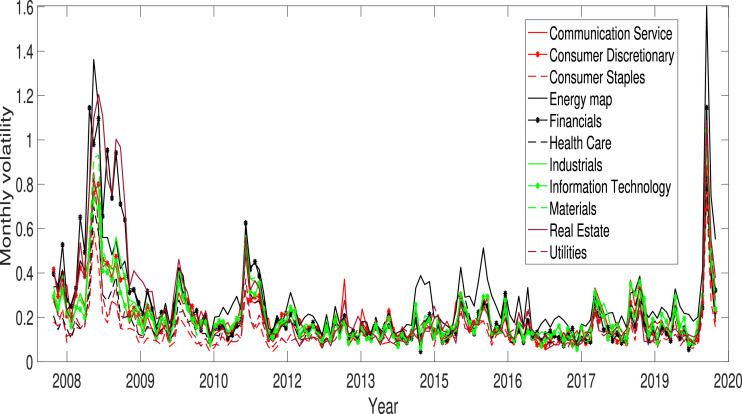

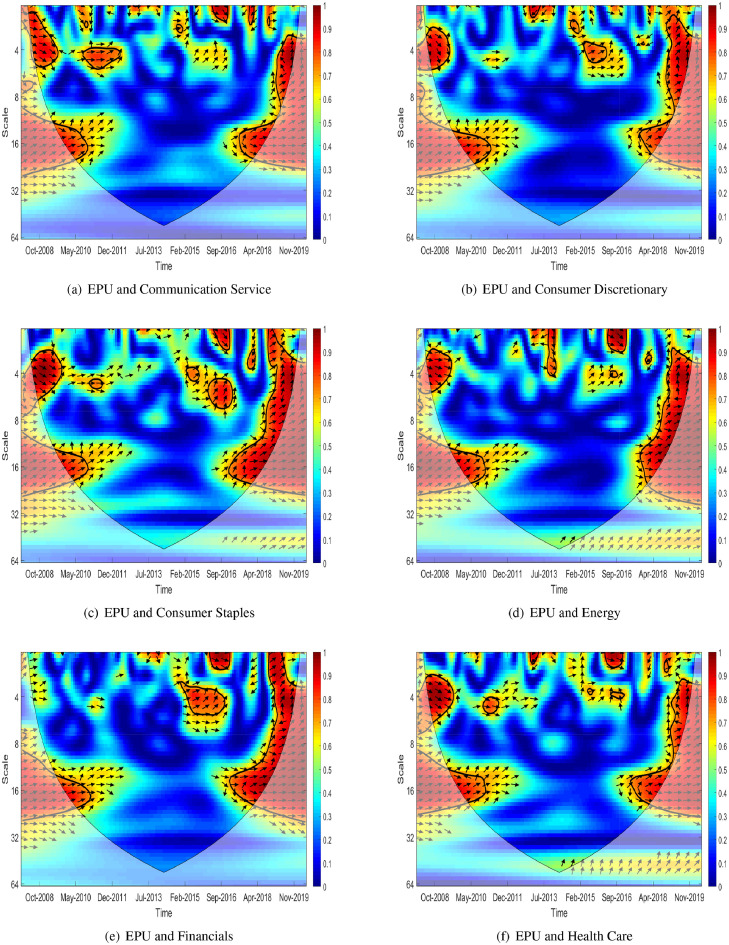

This study investigates the impact of economic uncertainty due to the coronavirus (COVID-19) pandemic on the industrial economy in the US in terms of the interdependence and causality relationship. We apply wavelet coherence analysis to economic policy uncertainty (EPU) data and monthly sector volatility of the S&P 500 index from January 2008 to May 2020. The results reveal that EPU in terms of COVID-19 has influenced the sector volatility more than the global financial crisis (GFC) for all sectors. Furthermore, EPU leads the volatility of all sectors during COVID-19 pandemic, while some sector's volatilities lead EPU during the GFC.

本研究从相互依存关系和因果关系的角度,调查了冠状病毒(COVID-19)大流行导致的经济不确定性对美国工业经济的影响。我们将小波相干分析应用于2008年1月至2020年5月的经济政策不确定性(EPU)数据和标准普尔500指数的月度行业波动率。结果表明,就所有行业而言,COVID-19相关的EPU对行业波动率的影响超过了全球金融危机(GFC)。此外,在COVID-19大流行期间,EPU引领所有行业的波动率,而在全球金融危机期间,一些行业的波动率引领EPU。